S corporation owners need to understand both internal basis and external basis because these separate tax systems determine loss deductions, taxable distributions, shareholder loans, Form 7203 reporting, and the tax impact of a future business sale.

Key Takeaways

- S corporations effectively operate with two separate basis systems: internal basis at the corporate asset level and external basis at the shareholder level.

- Internal basis helps determine depreciation and gain or loss when corporate assets are sold.

- External basis determines whether shareholder losses may be deducted, whether distributions are tax-free, and how stock sales are taxed.

- An S corporation bank loan generally does not increase shareholder basis, while a direct shareholder loan may create debt basis.

- Form 7203 tracks shareholder stock and debt basis. It does not track the corporation's internal basis in its assets.

Business owners often assume that if their company has substantial assets, cash in the bank, and a healthy balance sheet, they should be able to deduct losses, receive distributions tax-free, and understand the tax consequences of selling their business. Unfortunately, S corporation taxation does not always work that way.

A business owner may own a company worth several million dollars and still have insufficient basis to deduct losses. Another owner may receive a distribution, unexpectedly triggering a taxable gain. Yet another may sell a business and discover that the taxable consequences are significantly different from those anticipated. The source of this confusion usually comes down to one concept: basis.

In S corporation taxation, the concept of basis is frequently misunderstood. The reason it causes so much confusion is that S corporations effectively operate with two separate basis systems simultaneously. One basis system exists inside the company and tracks the tax basis of the corporation's assets. The other basis system exists at the shareholder level and tracks the owner's investment in the company.

Understanding these two systems is critical because they determine whether losses are deductible, whether distributions are taxable, how shareholder loans are treated, and ultimately how much tax may be owed when the business is sold.

An S Corporation Effectively Operates with Two Balance Sheets

The easiest way to understand basis is to think of an S corporation as maintaining two separate tax balance sheets.

The first balance sheet belongs to the corporation itself. It tracks the tax basis of the corporation's assets and liabilities. This includes cash, equipment, real estate, inventory, intellectual property, and any other property owned by the business.

The second balance sheet belongs to the shareholder. This ledger tracks the owner's investment in the company. It records stock basis, debt basis, contributions made by the owner, income allocated to the owner, losses passed through to the owner, and distributions received from the business.

These two systems constantly interact with one another, but they are not interchangeable. In fact, many of the most confusing S corporation tax outcomes arise because business owners assume that the corporation's basis and the shareholder's basis are the same. They are not. Understanding this distinction is the key to understanding nearly every basis-related rule that applies to S corporations.

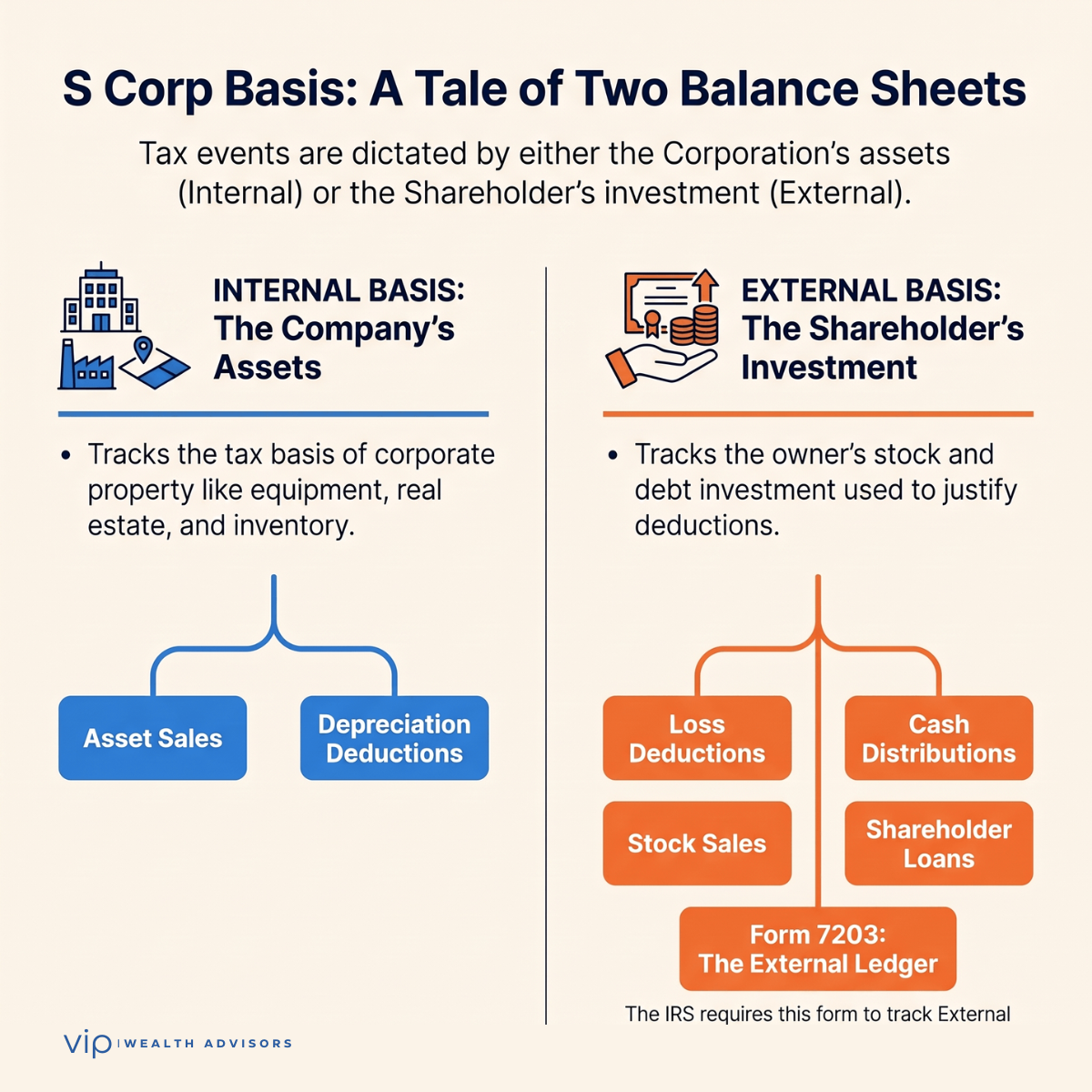

Visual Guide: The Two Balance Sheets Behind Every S Corporation

One balance sheet belongs to the company. The other belongs to the shareholder. Understanding the difference explains nearly every S corporation basis rule.

What Is Internal Basis?

Internal basis refers to the corporation's adjusted tax basis in its assets.

| Basis System | Who It Belongs To | What It Tracks | Why It Matters |

|---|---|---|---|

| Internal basis | The corporation | The adjusted tax basis of company assets | Depreciation and gain or loss on asset sales |

| External basis | The shareholder | Stock basis and debt basis | Loss deductions, taxable distributions, and stock sale gain or loss |

This table is a simplified overview. The article below explains how these systems interact.

Every asset owned by the company has a tax basis. If the corporation purchases equipment for $100,000, the equipment has an initial tax basis of $100,000. If the corporation purchases a building for $500,000, the building has an initial tax basis of $500,000. Over time, this basis changes.

Depreciation deductions reduce the tax basis of equipment and buildings. Additional capital expenditures may increase basis. The sale of assets removes basis from the corporation's books and determines the amount of gain or loss recognized on the sale.

Internal basis, therefore, serves as the tax accounting mechanism that determines how the corporation calculates depreciation deductions and computes gain or loss when assets are sold.

For example, suppose an S corporation purchases machinery for $250,000 and claims $100,000 of depreciation deductions over several years. The machinery's adjusted tax basis would then be $150,000. If the machinery is later sold for $200,000, the corporation would generally recognize a gain because the sales price exceeds the asset's adjusted basis.

Notice that this entire calculation occurs inside the corporation. At this stage, we have not considered the shareholder's basis at all. That is because the internal basis belongs to the corporation.

What Is External Basis?

External basis refers to the shareholder's adjusted basis in his or her investment in the S corporation. This basis generally consists of two components. The first component is stock basis. Stock basis generally begins with the amount of cash and property contributed to the corporation in exchange for stock. The second component is debt basis. Debt basis arises when a shareholder directly lends money to the corporation. Unlike internal basis, external basis is constantly changing.

External basis increases when the corporation allocates taxable income, tax-exempt income, or additional contributions to the shareholder. External basis decreases when the shareholder receives distributions, is allocated losses and deductions, or incurs certain nondeductible expenses.

The shareholder's external basis, therefore, acts as a running measure of the owner's economic investment in the company. This concept is extraordinarily important because basis limitations prevent shareholders from deducting losses that exceed their economic investment in the business.

Why External Basis Matters So Much

External basis determines several of the most important tax consequences facing S corporation shareholders.

It determines whether losses passed through from the corporation are currently deductible. It determines whether cash distributions are received tax-free or generate taxable gain. It determines the amount of gain or loss recognized when stock is sold. It also determines how shareholder loans are treated and whether suspended losses can eventually be deducted.

Because S corporations are pass-through entities, income and losses generally flow directly to the shareholders. Congress did not intend for shareholders to deduct losses that exceed their actual investment in the business. External basis rules were designed to prevent this result.

Consequently, maintaining accurate basis records is not merely a technical exercise. It directly affects the shareholder's current and future tax liabilities.

Maintaining accurate basis records is not merely a technical exercise.

Internal Basis and External Basis Often Move Independently

One of the most difficult aspects of S corporation taxation is understanding that internal basis and external basis frequently move in different directions.

Suppose an S corporation purchases equipment with cash. The corporation's internal basis in the equipment increases because it now owns an additional asset. However, the shareholder's stock basis generally does not increase merely because the company purchased equipment.

Now, assume the corporation generates substantial profits during the year. The shareholder's external basis generally increases because income passes through to the owner. Yet the corporation's basis in its assets may remain unchanged. Likewise, the corporation may own highly appreciated assets that have increased substantially in value while the shareholder has relatively little basis available to deduct losses. The corporation's economic value and the shareholder's basis are not the same thing. This distinction frequently surprises business owners.

How a Company Can Have Significant Assets but a Shareholder Has No Basis

Consider an S corporation that owns several valuable properties and maintains significant cash reserves. The company may be worth several million dollars. However, if the shareholder previously received substantial distributions or deducted losses that reduced basis over time, the shareholder may have little or no external basis remaining.

Suppose the corporation then experiences a difficult year and allocates a substantial loss to the shareholders. Even though the corporation still possesses significant assets and value, the shareholder may be unable to deduct the loss because there is insufficient basis available.

This outcome often seems counterintuitive because business owners naturally associate company value with basis. Tax law does not make that assumption. The corporation's value and the shareholder's basis are separate calculations.

Debt Basis and One of the Biggest S Corporation Traps

Debt basis creates another area of confusion. Many business owners assume that if their corporation borrows money from a bank, their basis automatically increases. In most cases, it does not. Unlike partnership taxation, borrowing by an S corporation generally does not create shareholder basis. Instead, debt basis typically arises only when the shareholder directly lends money to the corporation. This distinction can create unexpected consequences.

Suppose a corporation obtains a $1 million bank loan and subsequently generates losses. Even though the company now has additional liquidity and assets, the shareholders' basis may not increase simply because the corporation borrowed money from a third-party lender.

On the other hand, if the shareholder personally lends $1 million to the corporation, debt basis generally exists, potentially allowing losses to be deducted. This rule surprises many business owners and frequently leads to basis problems that are discovered years later.

Where Form 7203 Fits into the Picture

If basis is so important, many business owners assume that the IRS keeps track of these calculations for them. It does not. Basis tracking is ultimately the shareholder's responsibility. Form 7203, S Corporation Shareholder Stock and Debt Basis Limitations, exists because the IRS requires shareholders to demonstrate how much basis they have available. Form 7203 tracks external or outside basis. Specifically, it tracks stock basis and debt basis. It does not track the corporation's internal basis in its buildings, equipment, inventory, or other assets.

Think of Form 7203 as the shareholder's personal basis ledger. The form begins with the shareholder's beginning stock basis and then adjusts that amount for contributions, income items, losses, deductions, and distributions. It also separately tracks debt basis arising from direct shareholder loans to the corporation.

The purpose of Form 7203 is straightforward. The IRS wants to know whether the shareholder actually has sufficient basis to deduct losses and receive distributions without triggering additional tax consequences. In many respects, Form 7203 is simply the IRS's way of asking shareholders to show their work.

Why Basis Tracking Matters Throughout the Life of the Business

Basis is not simply an annual tax return exercise. Basis affects the shareholder throughout the business's entire life cycle. It affects annual loss deductions. It influences whether distributions are taxable. It affects debt planning and shareholder lending arrangements. It determines how suspended losses are treated. It also plays an important role when ownership interests are sold. When a shareholder sells S corporation stock, external basis is generally used to determine gain or loss on the sale.

Meanwhile, if the corporation sells its assets, internal basis becomes critically important because gain or loss is generally determined on an asset-by-asset basis. These two systems continue operating independently even during the disposition of the business. Understanding which basis system applies to a particular transaction is essential to accurately determining the tax consequences.

Which Basis System Applies?

Most S corporation tax questions can be answered by first identifying whether the transaction affects the corporation's basis or the shareholder's basis.

Seeing the Complete Picture

The easiest way to understand S corporation basis is to recognize that two separate tax balance sheets are operating at the same time.

Internal basis is the corporation's and tracks the adjusted tax basis of the company's assets. External basis belongs to the shareholder and tracks the owner's economic investment through stock basis and debt basis.

These two systems constantly influence one another, but they are not the same calculation and should never be treated as interchangeable.

Company value and shareholder basis are not the same calculation.

A corporation may own significant assets while the shareholder has little basis available to deduct losses. A shareholder may have substantial basis even though the corporation's assets have been heavily depreciated. A corporation's bank borrowing may have no impact on shareholder basis, while a direct shareholder loan can create debt basis that supports future deductions.

Form 7203 sits squarely within this framework. It does not track what the company owns. Instead, it tracks what the shareholder has invested and whether sufficient basis exists to support losses and distributions.

For S corporation owners, basis is one of the hidden engines of taxation and tax planning. Understanding how internal basis, external basis, and Form 7203 work together can help business owners make more informed decisions and avoid some of the most common and costly surprises in S corporation taxation.

Frequently Asked Questions About S Corporation Basis

What is basis in an S corporation?

Basis is a tax concept that measures a shareholder's investment in an S corporation and the corporation's investment in its assets. S corporations effectively operate with two separate basis systems. Internal basis refers to the corporation's adjusted tax basis in its assets, while external basis refers to the shareholder's adjusted basis in stock and direct loans made to the corporation. Basis is important because it determines whether losses are deductible, whether distributions are taxable, and how gains or losses are calculated when assets or stock are sold.

What is internal basis in an S corporation?

Internal basis is the corporation's adjusted tax basis in its assets. This includes cash, real estate, equipment, vehicles, inventory, intellectual property, and other business property. Internal basis changes over time as the corporation purchases and sells assets, claims depreciation deductions, and makes capital improvements. Internal basis primarily affects depreciation calculations and determines gain or loss when corporate assets are sold.

What is external basis in an S corporation?

External basis is the shareholder's adjusted tax basis in his or her investment in the S corporation. External basis consists of stock basis and, in certain circumstances, debt basis arising from direct loans made by the shareholder to the corporation. External basis determines whether losses may be deducted, whether distributions are taxable, and how gain or loss is calculated when S corporation stock is sold.

What is the difference between internal basis and external basis?

Internal basis belongs to the corporation and tracks the adjusted tax basis of corporate assets. External basis is attributable to the shareholder and reflects the owner's economic investment in the company. Internal basis determines the tax consequences associated with corporate assets, while external basis determines the tax consequences that affect the shareholder personally.

Why does an S corporation have two basis systems?

Congress created two basis systems because S corporations are pass-through entities. The corporation owns assets and therefore needs tax basis calculations for depreciation and asset sales. At the same time, shareholders report income, losses, and distributions on their personal tax returns and therefore need their own basis calculations. The two systems serve different purposes and frequently produce different outcomes.

Why can't I deduct my S corporation losses?

A shareholder generally cannot deduct S corporation losses that exceed his or her stock basis and debt basis. Basis limitations prevent shareholders from deducting losses that exceed their actual economic investment in the business. If losses exceed basis, the excess losses are generally suspended and carried forward until additional basis becomes available.

What happens to suspended S corporation losses?

Suspended losses are not permanently lost. Instead, they are carried forward indefinitely and may become deductible in future years when the shareholder restores basis through additional capital contributions, direct loans to the corporation, or pass-through income allocations.

How is stock basis calculated in an S corporation?

Stock basis generally begins with the amount of cash and the adjusted basis of property contributed to the corporation. Stock basis increases by income items and additional contributions and decreases by distributions, nondeductible expenses, and losses allocated to the shareholder. The calculation is cumulative and must be tracked from year to year.

What is debt basis in an S corporation?

Debt basis generally arises when a shareholder directly lends money to the corporation. Debt basis can allow shareholders to deduct losses that exceed their stock basis. However, debt basis is separate from stock basis and has its own ordering rules and restoration requirements.

Does an S corporation bank loan increase shareholder basis?

Generally, no. Unlike partnership taxation, debt borrowed directly by an S corporation from a bank usually does not increase shareholder basis. In most situations, debt basis arises only when the shareholder personally lends money to the corporation.

Does guaranteeing an S corporation loan create basis?

Generally, no. Merely guaranteeing a corporate loan typically does not create shareholder basis. Courts have consistently held that an economic outlay generally must occur before debt basis is created. If a shareholder ultimately pays under the guarantee and becomes the corporation's creditor, basis may arise at that time.

Do capital contributions increase stock basis?

Yes. Cash contributions and contributions of property generally increase a shareholder's stock basis. Increasing stock basis can provide additional capacity to deduct future losses and can reduce the likelihood that future distributions become taxable.

Do distributions reduce stock basis?

Yes. Generally, non-dividend distributions from an S corporation reduce stock basis. If distributions exceed available stock basis, the excess amount is generally treated as capital gain.

Are S corporation distributions always tax-free?

No. Distributions are often tax-free to the extent of the shareholder's stock basis. However, distributions that exceed available stock basis generally trigger taxable gain. This is why maintaining accurate basis records is extremely important.

Can an S corporation have substantial assets while the shareholder has zero basis?

Yes. This is one of the most misunderstood aspects of S corporation taxation. A corporation may own valuable real estate, equipment, and cash reserves while the shareholder has little or no basis available due to prior distributions and losses. Company value and shareholder basis are not the same calculation.

How does depreciation affect basis?

Depreciation generally reduces the corporation's internal basis in depreciable assets. Depreciation deductions may also indirectly reduce a shareholder's external basis if, for example, they contribute to losses that pass through to the shareholder. The impact on internal basis and external basis may occur simultaneously but represent two separate calculations.

How does basis affect the sale of an S corporation?

If a shareholder sells stock, external basis determines the amount of taxable gain or loss. If the corporation sells assets, internal basis determines the gain or loss on each asset sold. The structure of the transaction can therefore produce very different tax outcomes.

What is IRS Form 7203?

Form 7203, S Corporation Shareholder Stock and Debt Basis Limitations, is an IRS form used to track a shareholder's external basis. The form reports stock basis, debt basis, and basis adjustments resulting from contributions, income, losses, and distributions.

Does Form 7203 track internal basis?

No. Form 7203 does not track the corporation's basis in its assets. The form exclusively tracks external basis at the shareholder level. It is designed to determine whether shareholders have sufficient basis to deduct losses and receive distributions without generating additional tax consequences.

Who must file Form 7203?

Generally, shareholders are required to file Form 7203 when claiming a deduction for S corporation losses, receiving distributions, disposing of stock, receiving repayment of shareholder loans, or when other transactions require basis reporting. The form helps substantiate basis calculations and demonstrates compliance with the shareholder basis limitation rules.

Why is keeping basis records so important?

Basis records affect annual taxes, loss deductions, distributions, shareholder loans, business succession planning, and the taxation of a future sale. Reconstructing basis years later can be difficult and expensive. Maintaining accurate records each year helps business owners avoid unpleasant surprises and allows for more informed tax planning decisions throughout the life of the business.

Need help understanding your S corporation basis?

S corporation basis can affect loss deductions, distributions, shareholder loans, and the tax impact of selling a business. If you own an S corporation and want to understand how these rules may apply to your planning picture, schedule a conversation with our team.