Venture capital pitch decks can be persuasive, but investors should evaluate net returns, fees, illiquidity, benchmarks, and whether the opportunity fits their long-term strategy.

Key Takeaways

- Venture capital pitch decks often begin with a powerful macro narrative that makes the opportunity feel inevitable before the investment itself is fully evaluated.

- Elite company logos and standout winners can create a compelling highlight reel, but they may not show the full distribution of portfolio outcomes.

- Performance should be judged by net returns, DPI, TVPI, timing, fees, and realized outcomes, not just impressive dollar figures or unrealized valuations.

- Venture capital can offer asymmetric upside, but it also comes with illiquidity, fee drag, uncertainty, and a wide dispersion of results.

- The right question is not simply whether venture capital is a good investment, but whether it fits the investor’s broader strategy, liquidity needs, risk tolerance, and opportunity cost.

Top-tier venture capital pitch decks are rarely seen outside institutional circles.

That exclusivity is part of the appeal.

Once you begin to understand how these decks are constructed, how they guide your thinking, shape your expectations, and subtly steer attention away from uncomfortable realities, the mystique starts to fade. What initially feels impressive becomes something far more interesting: analyzable.

And that is exactly the purpose of this article.

We are going to break down a real-world pitch deck from one of the venture capital industry's most respected firms. Not to criticize the firm, but to examine how elite venture funds present opportunities, frame risk, and position themselves to sophisticated investors.

Because in investing, what is omitted from the presentation can matter just as much as what appears on the slide.

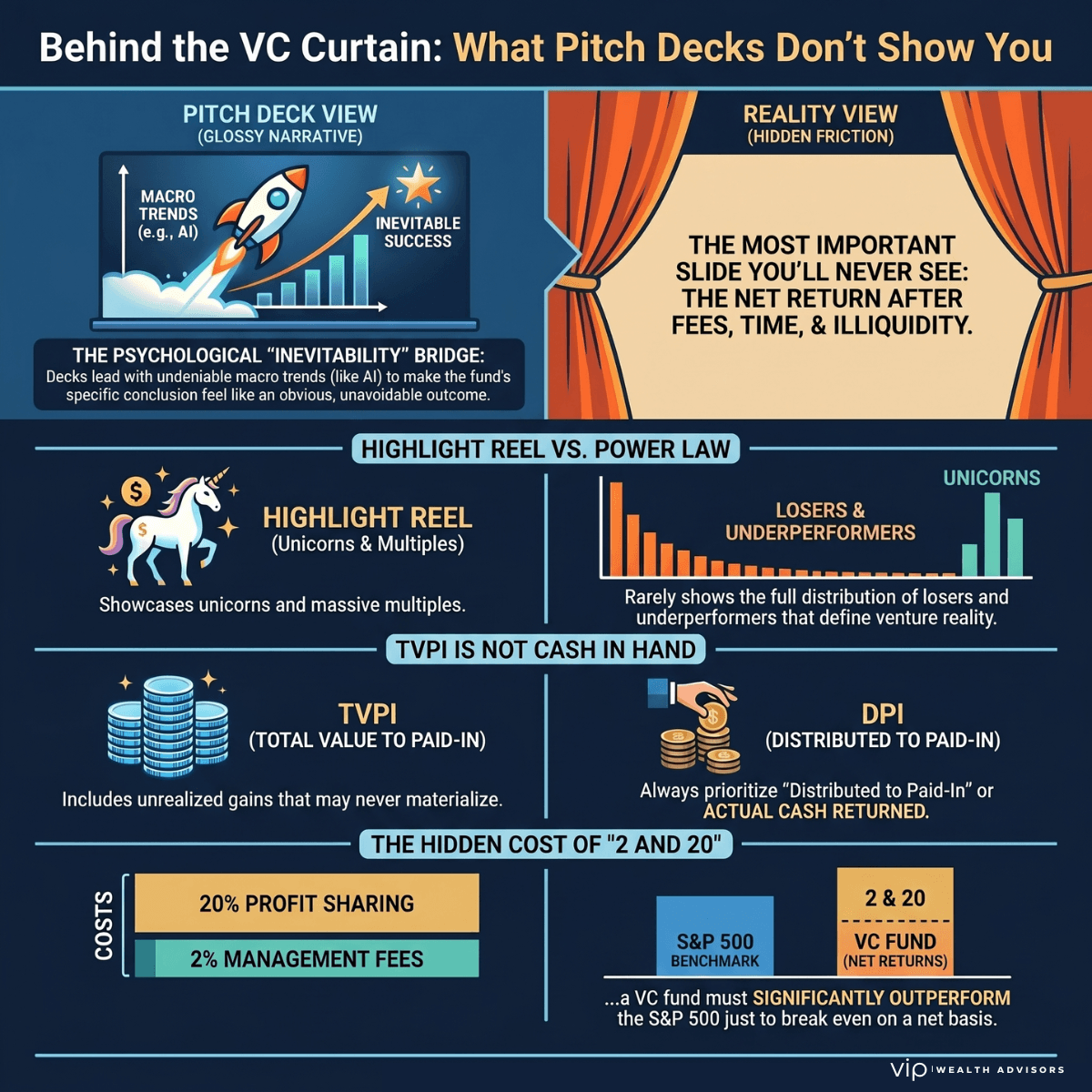

The First Move: Make the Opportunity Feel Inevitable

Every great venture pitch deck starts the same way, with a macro narrative you can’t argue with.

In this case, it’s artificial intelligence.

You’ll see slides talking about:

- AI is reshaping entire industries

- Massive global investment flows

- Structural shifts in healthcare, defense, and financial services

And here’s the thing, none of that is wrong.

AI is transformative. It will change industries. Capital is flowing aggressively into the space.

But that’s not the point.

The opening narrative is designed to move you from skepticism to acceptance before the investment is even introduced.

Because once you agree with the premise, the conclusion starts to feel obvious.

If AI is inevitable…

And this fund invests in AI…

Then this fund must be a great opportunity.

That’s the psychological bridge.

But investing isn’t about agreeing with a story. It’s about evaluating outcomes.

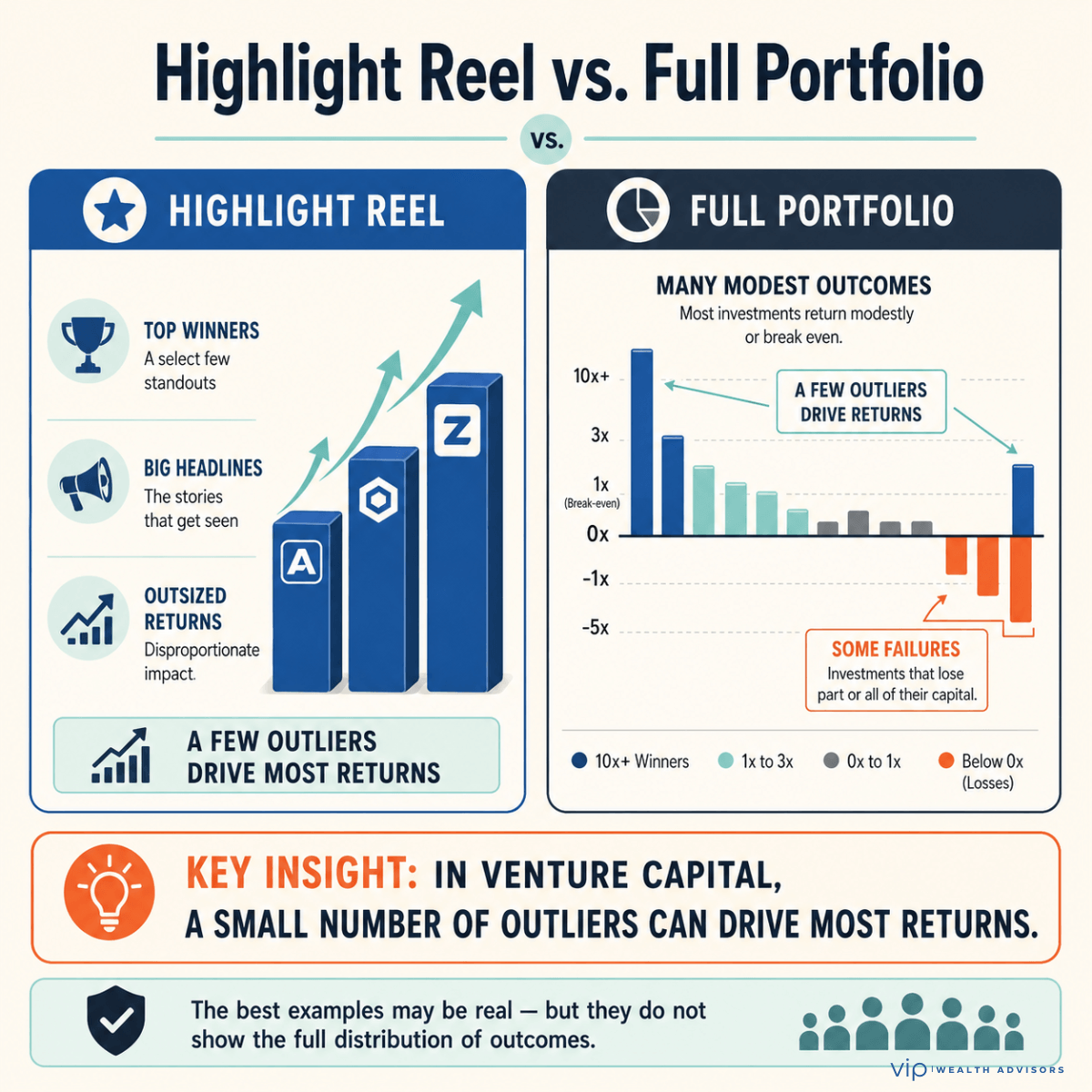

The Highlight Reel: Access to Elite Companies

Next comes the part that grabs attention.

Logos.

Stripe. Anthropic. Canva. Anduril.

Massive companies. Massive valuations. Massive implied returns.

You’ll see early entry points: $100 million valuations growing into $100 billion outcomes. Multiples that look almost absurd in hindsight.

This is where the pitch starts to feel powerful.

Is this the portfolio or the highlight reel?

Because venture capital operates on a power law:

- A small number of companies drive the majority of returns

- Most investments generate modest outcomes

- Many fail entirely

And yet, the deck doesn’t show:

- The full distribution of outcomes

- The percentage of companies that underperformed

- The capital allocated to winners vs. losers

Instead, it shows you the best examples.

Not because they’re misleading but because they’re persuasive.

The winners are real. The outcomes are real.

What’s less clear is how consistently those outcomes can be repeated.

The Difference Between the Highlight Reel and the Full Portfolio

Pitch decks often spotlight the winners, but thoughtful investors look for the full distribution of outcomes before drawing conclusions.

The Performance Framing Trick

At some point, the deck will show performance.

And it will look impressive.

You’ll see numbers like:

- Billions in realized gains

- Tens of billions in unrealized value

- Strong multiples on invested capital

It creates the impression of momentum. Scale. Success.

But here’s where experienced investors slow down.

Because venture capital performance is often presented in a way that feels big, but isn’t always comparable.

Let’s break down what’s typically missing:

1. Net IRR (after all fees)

This is the number that actually matters to you as an investor.

And it’s rarely front and center.

2. DPI vs. TVPI

- DPI (Distributed to Paid-In): actual cash returned

- TVPI (Total Value): includes unrealized gains

Many venture funds look exceptional on TVPI… while returning very little cash in the early years.

3. Time-weighted returns

A 3x return over 10 years is very different from a 3x return over 5 years.

Without a time context, multiples can be misleading.

Venture performance is often presented in dollars, not returns, because dollars feel more impressive.

And:

Unrealized gains are not the same as realized outcomes.

This doesn’t make the investment bad.

But it makes it incomplete.

The Strategy That Sounds More Predictable Than It Is

Modern venture funds present a highly structured strategy:

- Invest early (seed stage)

- Follow winners through Series A and B

- Concentrate capital into breakout companies

- Capture asymmetric upside

On paper, it sounds precise. Almost engineered.

But in reality, venture capital is still driven by:

- Founder quality

- Market timing

- Competitive dynamics

- Capital availability

- And yes, a meaningful degree of luck

The strategy is logical.

The outcomes are not predictable.

A well-defined process does not guarantee repeatable results.

And yet, pitch decks often blur that line, subtly suggesting that past success can be systematized.

In venture, that’s rarely true.

The Slide You’ll Never See: Fees, Time, and Friction

Let’s talk about what’s not emphasized.

Because this is where the real cost of the investment lives.

Most venture funds operate on a structure that looks like this:

- 2% annual management fee

- 20% carried interest (profit share)

- 10+ year investment horizon

And that’s just the beginning.

You also have:

- Capital calls over time (you don’t invest all at once)

- A “J-curve” effect (early negative returns due to fees and deployment timing)

- Limited liquidity (your capital is locked up for years)

None of this is hidden.

But it’s rarely highlighted.

The most important slide in a venture pitch deck is the one you’ll never see: the net return after fees, time, and illiquidity.

Because that’s the number that determines whether the investment actually outperforms.

What the Pitch Deck Emphasizes vs. What Investors Need to Evaluate

Pitch decks often highlight the story, the winners, and the upside. The real analysis happens when investors look at net returns, fees, liquidity constraints, and the full distribution of outcomes.

The Power Law Trap

Venture capital is built on a simple truth:

A small number of investments account for most of the returns.

That’s called a power law distribution.

Top firms understand this. They design portfolios around it.

But here’s what’s often underappreciated:

If you capture the right outliers, returns can be extraordinary. If you miss them or don’t size them correctly, returns can be average.

And the gap between those outcomes is massive.

Access to venture capital is not the same as access to top-decile outcomes.

You can invest in a well-known firm…

And still end up with returns that look surprisingly similar to public markets.

The Benchmark They Don’t Show You

Here’s what you will almost never see in a venture pitch deck:

A comparison to the S&P 500.

Why?

Because once you introduce a benchmark, the conversation changes.

Over the last 15 years:

- The S&P 500 has delivered roughly 12–13% annual returns

- With full liquidity

- Minimal fees

- Daily pricing transparency

Now compare that to venture:

- Target net returns: ~15–20% (if successful)

- Illiquid for 10+ years

- High fee structure

- Significant dispersion of outcomes

Are you being compensated enough for the additional risk and complexity?

Because if a venture fund delivers:

- 12–14% net…

You took:

- Illiquidity

- Fee drag

- Uncertainty

For a result you could have achieved in public markets.

So… Is This a Good Investment?

That’s the wrong question.

For whom does this make sense?

Venture capital can be appropriate if:

- You already have substantial public market exposure

- You’re seeking asymmetric, long-term upside

- You understand dispersion and power law dynamics

- You have access to truly top-tier managers

- You can afford to lock up capital without needing liquidity

It’s likely not appropriate if:

- You’re chasing returns rather than building a strategy

- You need flexibility or liquidity

- You’re sensitive to fees

- You believe the macro story guarantees the outcome

The Real Takeaway

Venture capital pitch decks are not designed to mislead.

They’re designed to persuade.

They show:

- The opportunity

- The upside

- The best-case scenarios

They spend less time on:

- Tradeoffs

- Opportunity cost

- Net outcomes

And that’s where thoughtful investors separate themselves. The best investors don’t get excited by pitch decks. They understand them.

Q&A: What Investors Should Know About Venture Capital Funds

What returns should I expect from a venture capital fund?

Top-tier venture capital funds typically target net returns of 15–20% annually. However, actual outcomes vary widely. Many funds underperform these targets, especially after fees and over long time horizons.

How do venture capital returns compare to the S&P 500?

Over the past 15 years, the S&P 500 has delivered approximately 12–13% annually with full liquidity and minimal fees. Venture capital may offer higher upside, but the margin of outperformance is often smaller than expected once fees and illiquidity are considered.

What is the biggest risk in venture capital investing?

The biggest risk is not volatility, it’s opportunity cost and illiquidity. Your capital is typically locked up for 10+ years, limiting your ability to rebalance, redeploy, or access funds when needed.

Why do venture capital funds show unrealized gains?

Venture funds often report Total Value (TVPI), which includes unrealized gains based on estimated valuations. These are not the same as cash returns and may change significantly over time.

What does “power law” mean in venture capital?

Power law means that a small number of investments generate the majority of returns. In practice, this means most companies in a portfolio contribute little or no return, while a few outliers drive overall performance.

Are venture capital fees higher than traditional investments?

Yes. Venture funds typically charge around 2% annually in management fees plus 20% carried interest on profits. These fees can significantly reduce net returns relative to low-cost public-market investments.

Is venture capital a good investment for high-income professionals?

It can be, but usually as a satellite allocation rather than a core strategy. It’s most appropriate for investors who already have a strong foundation in public markets and are seeking long-term, high-risk, high-reward opportunities.

How should I evaluate a venture capital fund?

Focus on:

- Net returns (after fees)

- Track record across multiple cycles

- Ability to access top-tier deals

- Portfolio concentration and follow-on strategy

- Alignment of incentives

And always compare expected outcomes to public market alternatives.

Before You Invest in a Private Opportunity, Understand the Tradeoffs

Venture capital can sound compelling on paper, especially when the story is built around innovation, elite access, and exceptional upside. But the real decision is whether the opportunity fits your broader financial strategy, liquidity needs, and long-term goals.

VIP Wealth Advisors can help you evaluate private investments with a clear view of fees, risk, opportunity cost, and how the allocation fits into your bigger picture.