Avoiding double taxation is not automatic—it depends on correctly coordinating multiple tax systems, IRS forms, and planning decisions before mistakes compound.

Key Takeaways

- Cross-border professionals are often dealing with two or more tax systems at the same time.

- The IRS still expects worldwide income reporting based on status, not just where you live.

- Forms like 1040, 1116, 2555, FBAR, and 8938 do not just document your tax life—they shape the outcome.

- The Foreign Tax Credit often creates better long-term results than the Foreign Earned Income Exclusion for high earners.

- Most expensive mistakes are not dramatic. They are small coordination failures that compound over time.

The Illusion of Simplicity

“I already pay taxes where I live… so I’m covered, right?”

That assumption is where the trouble begins.

If you’re a U.S. citizen working abroad, a green card holder on assignment overseas, or a foreign national working in the United States, your tax life doesn’t simplify when you cross borders… it multiplies.

The U.S. operates on a system that is both uniquely expansive and quietly unforgiving:

If you are a U.S. taxpayer, the IRS expects you to report your worldwide income—regardless of where you live or where the income is earned.

That means your financial life now lives in two (or more) tax systems simultaneously. And the IRS doesn’t coordinate that for you.

You do.

Or more realistically… someone like us does it with you.

The Foundation: Why the IRS Still Has a Claim on Your Income

Before we get into forms, you need to understand the rules of the game.

Who is subject to U.S. worldwide taxation?

- U.S. citizens (no matter where they live)

- Green card holders (even if they leave the U.S.)

- Foreign nationals who meet the Substantial Presence Test

For foreign workers, this is where things get real.

Spend enough time in the U.S., and you may be treated as a U.S. tax resident, even if your passport says otherwise.

For U.S. citizens abroad, there is no “I moved, so I’m done” moment.

You are always in the system.

Don’t Get Taxed Twice: The Cross-Border Reality

Before diving into specific IRS forms, here’s a high-level view of how cross-border tax risk actually builds—and where most people get it wrong.

Most cross-border tax issues don’t come from one major mistake. They come from small gaps—missed forms, poor coordination, or the wrong strategic choices—that compound over time.

Now let’s break down the specific forms that drive these outcomes—and where mistakes tend to happen.

The IRS Forms: The Cast of Characters You Can’t Ignore

Think of your tax return as a story you’re telling the IRS.

These forms are the chapters. Miss one… and the story stops making sense.

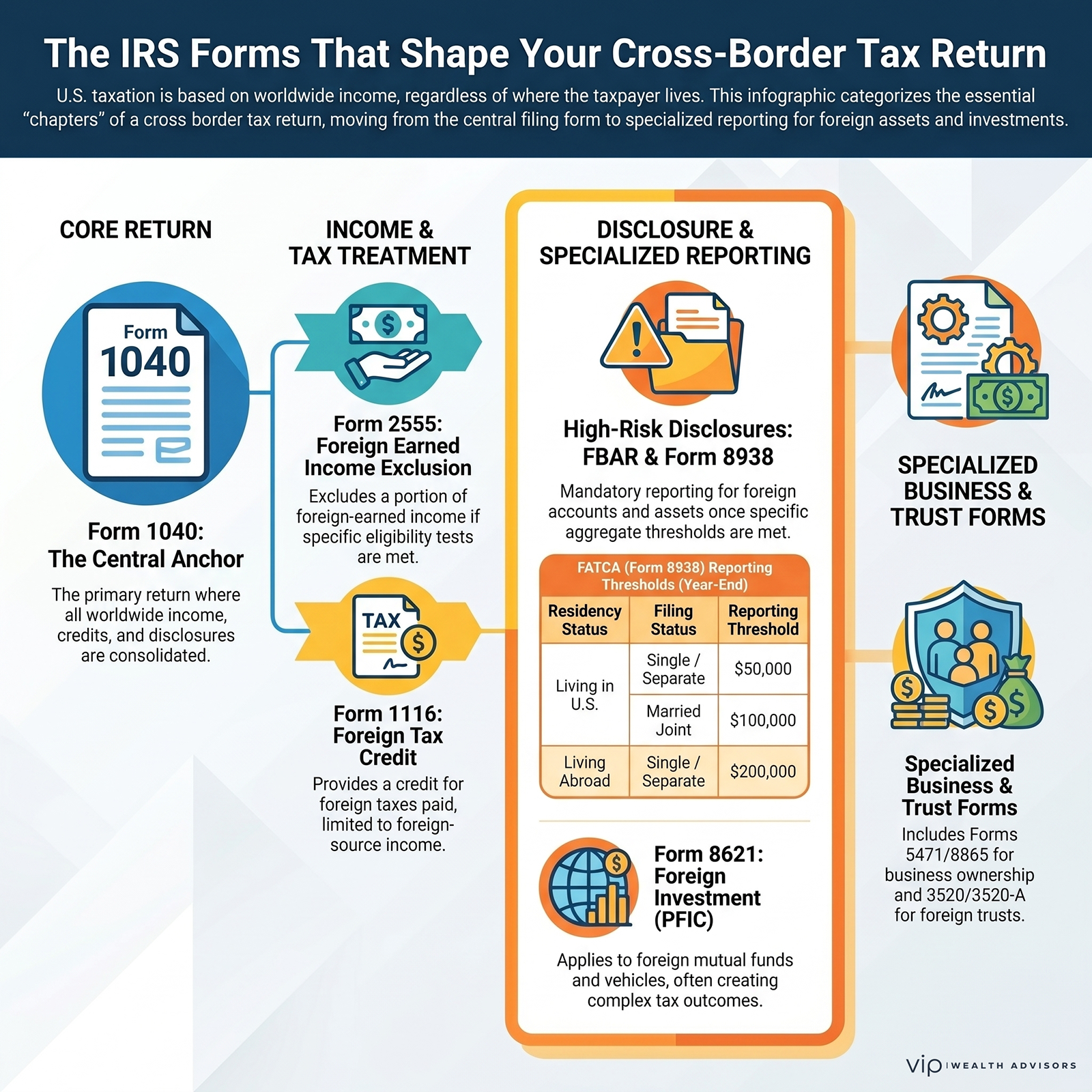

Form 1040 — The Anchor

This is your main return.

Everything flows through here:

- U.S. income

- Foreign income

- Credits

- Disclosures

If you’re cross-border, this is not just a tax form… It’s a consolidation engine.

Schedule B — Where Foreign Accounts Start to Matter

If you have foreign bank or investment accounts, this is where the IRS starts asking questions.

It also triggers additional reporting requirements.

And once you check “yes” to those foreign account questions… the IRS expects follow-through.

Form 2555 — The Foreign Earned Income Exclusion (FEIE)

This form allows you to exclude a portion of foreign-earned income from U.S. taxation.

Sounds great. And sometimes it is.

But here’s the catch:

- It only applies to earned income

- It requires passing either a Physical Presence Test or a Bona Fide Residence Test

And most importantly…

It’s not always the best option.

Many high-income professionals are better off not excluding income… and instead using credits.

We’ll get there.

Form 1116 — The Foreign Tax Credit (The Real Power Tool)

This is where strategy lives.

If you pay taxes to another country, this form allows you to claim a credit against your U.S. tax.

Not a deduction.

A credit.

That’s a completely different animal.

We’ll go deeper in a moment.

FBAR (FinCEN Form 114) — The Quiet Enforcer

This isn’t filed with your tax return, but ignoring it is a mistake people don’t easily recover from.

If your foreign accounts exceed $10,000 (aggregate), you must file.

Penalties for missing it can be… aggressive.

Form 8938 — FATCA Reporting

This is where the IRS moves from curiosity to full visibility.

Form 8938 requires you to disclose Specified Foreign Financial Assets (SFFAs) once you cross certain reporting thresholds. And unlike other parts of the tax return, these thresholds don’t just depend on how much you earn… they depend on where you live and how you file.

If You Live in the United States

- Single or Married Filing Separately

- $50,000 on the last day of the year, or

- $75,000 at any point during the year

- Married Filing Jointly

- $100,000 on the last day of the year, or

- $150,000 at any point during the year

If You Live Abroad

(and meet the IRS definition of having a foreign tax home plus physical presence or bona fide residence)

- Single or Married Filing Separately

- $200,000 on the last day of the year, or

- $300,000 at any point during the year

- Married Filing Jointly

- $400,000 on the last day of the year, or

- $600,000 at any point during the year

Miss this… and the penalties stack quickly.

Form 8621 — The PFIC Problem

If you own foreign mutual funds or certain foreign investment vehicles, this form enters your life.

And when it does… things get complicated fast.

PFIC rules can turn otherwise normal investments into tax inefficiencies.

This is one of the most common traps for expats.

Forms 5471 and 8865 — Foreign Business Ownership

Own part of a foreign company or partnership?

Now you’re in deep reporting territory.

These forms are detailed, technical, and carry significant penalties if missed or filed incorrectly.

Forms 3520 / 3520-A — Foreign Trusts and Gifts

Receiving large foreign gifts? Involved with foreign trusts?

These forms exist to make sure the IRS sees everything.

And they are not forgiving.

The Foreign Tax Credit: Where Planning Actually Happens

Let’s slow this down, because this is where most of the value is created… or lost.

Why this section matters

- What the Foreign Tax Credit Really Is

- Credit vs Deduction (Why This Matters)

- The Limitation Rule (The Hidden Governor)

- The Basket System (Why Not All Income Is Equal)

- Carryovers: The Long Game

- FTC vs FEIE: The Strategic Fork in the Road

What the Foreign Tax Credit Really Is

The Foreign Tax Credit (FTC) is designed to prevent double taxation.

But it doesn’t do this automatically.

It allows you to offset U.S. taxes with taxes you’ve already paid to a foreign country.

That sounds simple. It’s not.

Credit vs Deduction (Why This Matters)

- A deduction reduces taxable income

- A credit reduces your tax bill dollar-for-dollar

If you paid $20,000 in foreign taxes, the FTC can potentially reduce your U.S. tax by $20,000.

That’s real money.

The Limitation Rule (The Hidden Governor)

Here’s the constraint:

You can only use the credit against U.S. tax on foreign-source income.

In other words:

- Foreign taxes → offset foreign income tax

- Not U.S. income

This is where many returns go sideways.

The Basket System (Why Not All Income Is Equal)

The IRS divides income into categories:

- General income (wages, business income)

- Passive income (interest, dividends, investments)

Credits from one category generally can’t offset taxes in another.

So now you’re not just managing taxes…

You’re managing types of income.

Carryovers: The Long Game

Unused credits don’t just disappear.

- 1-year carryback

- 10-year carryforward

This creates planning opportunities, especially for clients with fluctuating income.

FTC vs FEIE: The Strategic Fork in the Road

This is where decisions matter.

FEIE (Form 2555):

- Excludes income

- Simple concept

- Can limit future credits

FTC (Form 1116):

- Keeps income visible

- Uses foreign taxes as credits

- Often better for high earners

Many high-income professionals instinctively use the exclusion… when the credit would produce a better long-term outcome.

This is not a software decision.

This is a strategy decision.

Where Things Break (And Why It’s Expensive)

This is the part no one advertises.

But it’s where we see real damage.

Common Mistakes:

- Using FEIE when FTC would be more beneficial

- Failing to file FBAR or FATCA forms

- Holding foreign mutual funds without understanding PFIC rules

- Currency conversion errors (timing matters)

- Missing foreign reporting thresholds

- Double taxation due to timing mismatches between countries

Each one seems small in isolation.

Together… they compound.

Foreign Workers in the U.S.: The Other Side of the Equation

If you’re coming into the U.S., the complexity doesn’t disappear; it just changes shape.

Residency Status Drives Everything

- Form 1040 → U.S. tax resident

- Form 1040-NR → Nonresident

And then there are dual-status years, where you are both.

Treaty Benefits

The U.S. has tax treaties with many countries.

These can:

- Reduce tax

- Eliminate double taxation

- Change how income is classified

But they must be properly claimed.

The Substantial Presence Test

This determines whether you’re treated as a U.S. resident.

And once you cross that threshold…

You’re in the worldwide income system.

The Strategic Layer: This Is Where Planning Beats Filing

Filing is backward-looking.

Planning is forward-looking.

And cross-border tax is where that distinction matters most.

What Real Planning Looks Like:

- Coordinating U.S. and foreign tax advisors

- Timing income recognition across jurisdictions

- Structuring equity compensation decisions globally

- Avoiding PFIC exposure before it happens

- Managing foreign tax credit carryforwards intentionally

This is not about filling out forms correctly.

It’s about making sure those forms tell the right story.

The Cost of Getting This Almost Right

Here’s the uncomfortable truth:

Most cross-border taxpayers aren’t wildly wrong.

They’re just… slightly off.

And in this space, “slightly off” can mean:

- Paying more tax than necessary

- Missing credits that could have been used

- Creating future problems that don’t show up for years

The goal isn’t just compliance.

The goal is coordination.

Because once your financial life crosses borders…

Precision becomes wealth.

Frequently Asked Questions

Do U.S. citizens have to pay taxes on foreign income?

Yes. U.S. citizens are taxed on their worldwide income, regardless of where they live.

What is Form 1116 used for?

Form 1116 is used to claim the Foreign Tax Credit, allowing taxpayers to offset U.S. taxes with foreign taxes paid.

Can I use both the Foreign Earned Income Exclusion and the Foreign Tax Credit?

Yes, but not on the same income. Strategic coordination is required.

What happens if I don’t file an FBAR?

Penalties can be significant, including fines that may exceed the account's value in extreme cases.

What is a PFIC?

A Passive Foreign Investment Company is a foreign investment vehicle that receives unfavorable U.S. tax treatment. Watch out for this one!

Do visa holders pay U.S. taxes on worldwide income?

If they meet the Substantial Presence Test, yes—they are treated as U.S. tax residents.

What is Form 8938 used for?

Form 8938 reports foreign financial assets under FATCA requirements.

What is the difference between Form 1040 and 1040-NR?

Form 1040 is for U.S. residents; Form 1040-NR is for nonresident aliens.

Can foreign taxes be carried forward?

Yes. Unused foreign tax credits can generally be carried forward for up to 10 years.

Is the Foreign Earned Income Exclusion always the best option?

No. High-income individuals often benefit more from the Foreign Tax Credit.

Cross-border tax mistakes rarely come from one big decision. They come from small forms, small thresholds, and small timing issues that add up.

If your income, accounts, or residency touch more than one country, the smartest next move is coordinated planning before filing season turns into damage control.