Box spread loans are sophisticated portfolio-backed financing strategies that may allow eligible high-net-worth investors to borrow against liquid, marginable assets at fixed rates near Treasury yields, but they require careful collateral, tax, and risk management.

Watch: Sell Investments? Or Borrow Against Them?

Key Takeaways

- Box spread loans use options to create a synthetic borrowing arrangement where an investor receives cash today and repays a predetermined amount at expiration.

- For some wealthy investors, the appeal is potential access to fixed-rate financing that may be lower than an SBLOC or traditional lending option.

- The strategy generally depends on liquid, publicly traded, marginable collateral rather than W-2 income or business cash flow.

- The biggest risks are usually collateral risk, concentrated stock exposure, refinancing risk, tax complexity, and the behavioral risk of taking on too much leverage.

- A box spread loan may make sense for certain high-net-worth investors, but only when the potential savings justify the additional complexity.

A 2026 Analysis by VIP Wealth Advisors: Examining a Leading Strategy for High-Net-Worth Liquidity

- What Is a Box Spread?

- How a Box Spread Loan Works

- Why Are Box Spread Loans Suddenly Becoming Popular?

- Box Spread Loan vs. SBLOC

- Who Qualifies for a Box Spread Loan?

- Can Private Company Stock Be Used as Collateral?

- The Risks Investors Must Understand

- When a Box Spread Loan May Make Sense

- When an SBLOC May Be Better

- The VIP Wealth Advisors Perspective

- Frequently Asked Questions

Imagine you’re a SpaceX employee sitting on a $10 million portfolio. Or perhaps you’re a founder who recently experienced a liquidity event and now holds a substantial taxable investment account. You need $2 million for a home purchase, a real estate investment, a business opportunity, or a tax obligation.

Selling appreciated investments could trigger hundreds of thousands of dollars in capital gains taxes. A traditional mortgage might cost 6% to 7%. A Securities-Based Line of Credit (SBLOC) could carry a variable interest rate and expose you to rising borrowing costs. Then someone mentions a strategy you’ve never heard of before: “Why not borrow through the options market using a box spread loan?” At first glance, it sounds like something pulled from a hedge fund playbook.

In reality, it is. For decades, institutional investors, market makers, and sophisticated trading firms have used box spreads as a financing tool. Until recently, however, the strategy was largely inaccessible to individual investors. That is beginning to change. New Fin-tech companies are building technology platforms designed to make box spread financing available to wealthy investors and their advisors. The result is a growing conversation among high-net-worth investors, founders, executives, and financial advisors: Can wealthy investors really borrow against their portfolios at rates approaching Treasury yields? And more importantly: Should they? Let’s separate the marketing from the reality.

This article is educational in nature and is not an endorsement of any specific platform, lender, broker, or financing provider.

Cheap debt is still debt. The best financing strategy is the one that remains sustainable during difficult markets.

What Is a Box Spread?

A box spread is an options strategy that combines:

- A bull call spread

- A bear put spread

Using the same strike prices and expiration date. The result is a position with a guaranteed payoff at expiration regardless of where the underlying index finishes. That certainty is what makes box spreads unique. Unlike most options strategies, which are designed to speculate on market direction, a properly constructed box spread behaves more like a bond than an investment. The future value is known in advance. For example, imagine a box spread constructed using S&P 500 index (SPX) options with strike prices of 5,000 and 6,000. Because the difference between the strikes is 1,000 points and SPX options use a 100 multiplier, the box spread will be worth exactly $100,000 at expiration. Not approximately. Exactly. This guaranteed future value is what creates the financing opportunity.

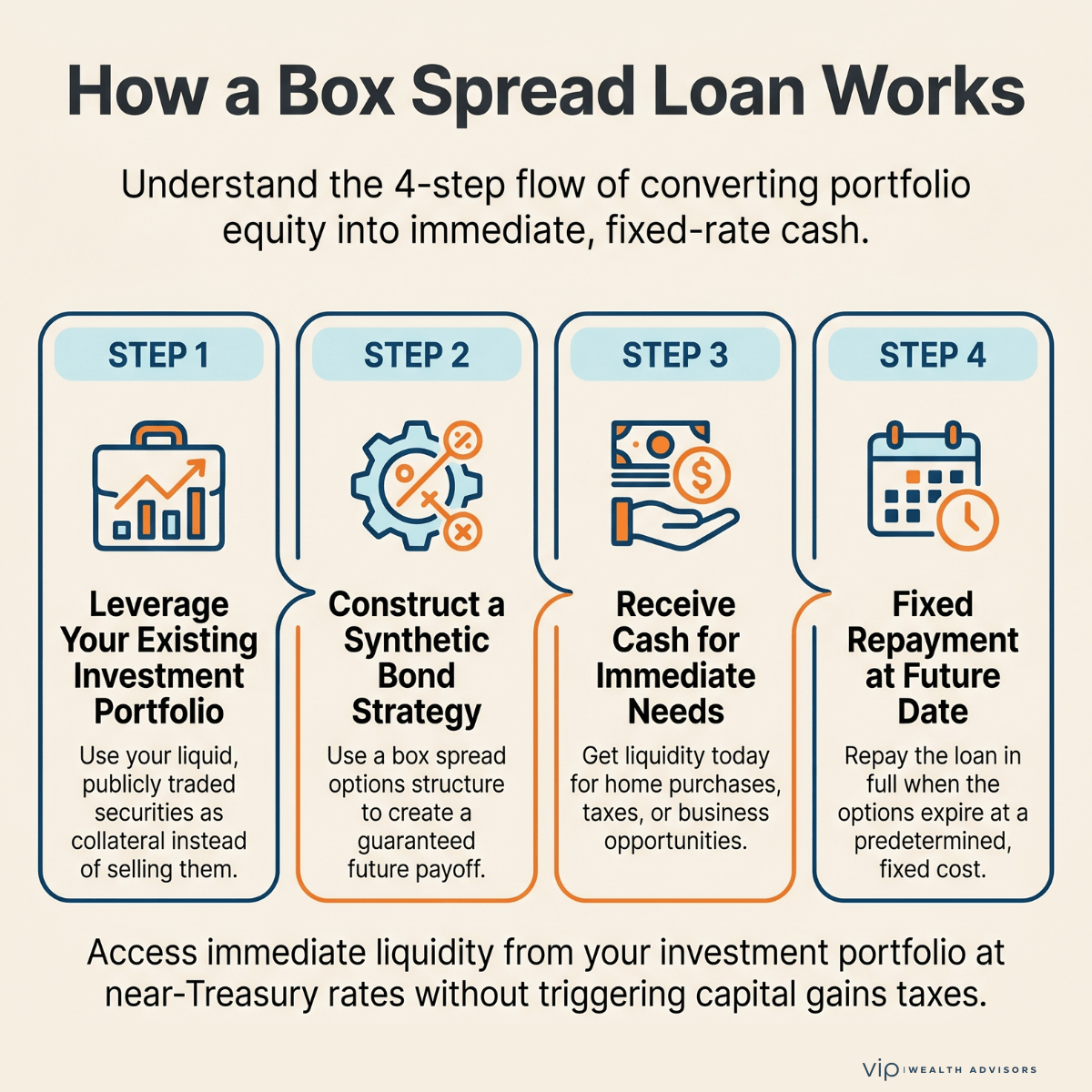

How a Box Spread Loan Works

The easiest way to understand a box spread loan is to think of it as creating a synthetic bond. Suppose a box spread will be worth $100,000 in three years. Today, the options market prices that box at $88,000. Why? Because money has a time value. Receiving $100,000 three years from now is not the same as receiving $100,000 today. If you buy the box, you are effectively lending money. If you sell the box, you are effectively borrowing money.

Buying the box can resemble lending money. Selling the box can resemble borrowing money. The financing cost is embedded in the difference between the cash received today and the fixed amount due at expiration.

In the borrowing scenario:

- You receive cash today

- You repay a larger amount at expiration

- The difference represents your borrowing cost

Economically, this works much like issuing your own bond backed by your investment portfolio.

How a Box Spread Loan Creates Liquidity

A simplified view of how investors use options positions to receive cash today and repay a predetermined amount in the future.

Why Are Box Spread Loans Suddenly Becoming Popular?

For years, box spreads were mostly discussed in quantitative finance circles. Today, several factors are driving interest among wealthy investors.

Higher Interest Rates

Borrowing costs matter again. When an investor needs $2 million to buy a home, the difference between borrowing at 6.5% and borrowing at 4.5% can be substantial.

Large Taxable Portfolios

Many technology professionals and founders now hold multi-million-dollar investment accounts. They have assets but may prefer not to sell those assets and incur capital gains taxes.

Concentrated Stock Positions

Employees at companies such as Nvidia, Databricks, Stripe, OpenAI, SpaceX, and countless startups often hold substantial equity positions. Liquidity planning has become increasingly important.

New Platforms

Companies such as SyntheticFi have built infrastructure that simplifies what was previously a highly technical institutional strategy. Rather than navigating complex options chains, clients interact with what feels much more like a traditional lending product.

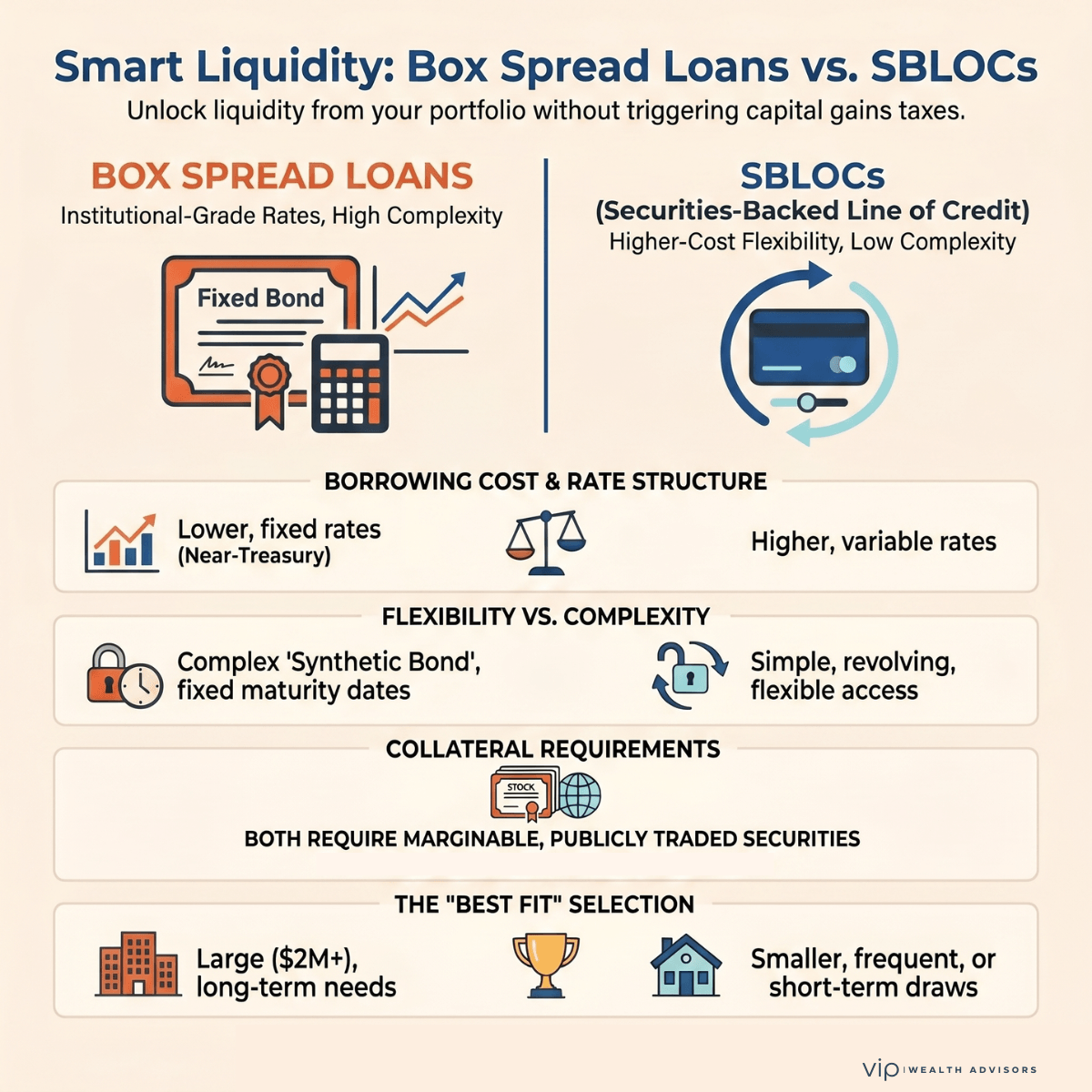

Box Spread Loan vs. SBLOC

The most important comparison is not between box spreads and traditional mortgages. It’s between box spreads and Securities-Based Lines of Credit.

| Feature | Box Spread Loan | SBLOC |

|---|---|---|

| Potential Interest Rate | Often Lower | Usually Higher |

| Rate Structure | Typically Fixed | Usually Variable |

| Complexity | Higher | Lower |

| Flexibility | Lower | Higher |

| Maturity Date | Fixed | Revolving |

| Collateral Requirement | Yes | Yes |

| Margin Risk | Yes | Yes |

An SBLOC remains the simpler solution. A box spread loan becomes interesting when the potential interest savings are significant enough to justify the additional complexity. For a client borrowing $100,000, the difference may not matter. For a client borrowing $2 million to $5 million, absolutely.

Who Qualifies for a Box Spread Loan?

A misconception is that approval depends on income. Traditional bank lending focuses on:

- W-2 income

- Business cash flow

- Debt-to-income ratios

- Tax returns

Box spread financing focuses on something else entirely:

Collateral. The central question becomes:

“How much liquid, marginable collateral does the client have?”

A client with:

- $10 million invested assets

- $300,000 salary

may be a stronger candidate than someone with:

- $2 million salary

- $200,000 brokerage account

This is asset-based financing, not income-based financing.

Can Private Company Stock Be Used as Collateral?

This is a question we receive from startup employees and founders. The answer is generally:

Not directly. Private shares in companies such as:

- Databricks

- Stripe

- OpenAI

- Anthropic

are typically not marginable. They are not publicly traded and cannot be easily valued or liquidated on a daily basis. Most box spread financing structures require publicly traded securities held in a brokerage account. That doesn’t mean private-company shareholders have no options. Specialized firms such as Secfi and others offer financing solutions specifically designed for pre-IPO equity holders. However, those products are fundamentally different from box spread loans.

Box Spread Loan vs. SBLOC at a Glance

Both strategies provide liquidity from invested assets, but they differ in flexibility, complexity, and borrowing structure.

The Risks Investors Must Understand

Every financing strategy has risks. Box spread loans are no exception.

The primary question is not whether the borrowing rate looks attractive. It is whether the investor can sustain the strategy through market declines, collateral calls, refinancing pressure, and changing personal liquidity needs.

Collateral Risk

The largest risk is not the box spread itself. It is the collateral supporting it. If portfolio values decline significantly, additional collateral may be required.

Concentrated Stock Risk

Many wealthy investors have concentrated positions. Borrowing aggressively against a highly concentrated portfolio can dramatically amplify risk.

Refinancing Risk

Box spreads have maturity dates. If the loan expires and rates have risen substantially, refinancing may be more expensive.

Liquidity Risk

Unlike an SBLOC, traditional box spreads are not naturally revolving credit facilities. Accessing additional capital may require establishing new financing structures.

Tax Complexity

Certain option transactions can trigger specialized tax rules. Professional tax guidance is essential before implementing large strategies.

Behavioral Risk

The ability to borrow cheaply can encourage investors to take on too much debt. Cheap debt is still debt. The best financing strategy is the one that remains sustainable during difficult markets.

When a Box Spread Loan May Make Sense

Potential candidates include:

Technology Executives

An executive with a large taxable portfolio who wants liquidity without triggering capital gains.

Founders

A founder who has already experienced a liquidity event and wishes to access capital while remaining invested.

Concentrated Stock Holders

Investors seeking temporary liquidity before a planned diversification strategy.

Real Estate Investors

Individuals who need bridge financing for a transaction while maintaining investment exposure.

When an SBLOC May Be Better

Sometimes the simplest answer is the best answer. An SBLOC may be preferable when:

- Borrowing needs are relatively small

- Flexibility is the highest priority

- Funds will be drawn and repaid frequently

- Simplicity outweighs potential interest-rate savings

Not every sophisticated strategy is automatically superior.

The VIP Wealth Advisors Perspective

Box spread loans represent a fascinating evolution in portfolio-backed lending. They are no longer merely a theoretical strategy discussed among traders and hedge funds. For certain wealthy investors, they may offer a legitimate alternative to traditional securities-based lending. However, we believe investors should focus on the right question. The question is not: “Can I borrow at a lower rate?” The question is: “Does the potential benefit justify the additional complexity, collateral requirements, refinancing risk, and leverage?”

The question is not: “Can I borrow at a lower rate?” The question is: “Does the potential benefit justify the additional complexity, collateral requirements, refinancing risk, and leverage?”

For the right client, the answer may be yes. For many others, traditional lending solutions remain entirely appropriate. As with any sophisticated planning strategy, success depends less on the product itself and more on thoughtful implementation, prudent risk management, and alignment with long-term financial goals.

Frequently Asked Questions About Box Spread Loans

What is a box spread loan?

A box spread loan is a financing strategy that uses options positions to create a synthetic borrowing arrangement. Investors receive cash today and repay a predetermined amount at a future date.

How do box spread loans work?

They work by selling a box spread constructed from options. The investor receives cash upfront and repays a fixed amount when the options expire.

Are box spread loans legal?

Yes. Box spreads are legitimate options strategies widely used by institutional investors and market participants.

Are box spread loans risky?

The primary risks involve collateral management, market declines, refinancing risk, and leverage rather than the box spread mechanics themselves.

What is the difference between a box spread loan and an SBLOC?

A box spread loan typically offers fixed-rate financing through the options market, while an SBLOC is a revolving line of credit secured by investments.

Can I borrow against my stock portfolio using a box spread?

Potentially, yes. Eligibility depends largely on the size and composition of your brokerage account.

Can private company stock be used as collateral?

Generally, no. Most box spread financing structures require publicly traded, marginable securities.

What is SyntheticFi?

SyntheticFi is a platform that helps advisors and investors access financing solutions built around box spreads and portfolio-backed lending strategies.

What is portfolio margin?

Portfolio margin is an alternative margin methodology that evaluates overall portfolio risk rather than applying traditional Reg T rules.

How much collateral is required?

Requirements vary depending on portfolio composition, concentration levels, broker policies, and margin treatment.

What happens if the market crashes?

A significant market decline could trigger margin calls, collateral requirements, or forced liquidation if leverage is too high.

Do box spread loans have monthly payments?

Many box spread loans do not require traditional monthly payments. Repayment is typically due at maturity.

Can a box spread loan be used to buy a home?

Yes. Some investors use portfolio-backed financing as an alternative to traditional mortgages.

What happens when the loan expires?

The financing must generally be repaid or refinanced using a new financing structure.

Are box spread loans tax-deductible?

Tax treatment depends on individual circumstances and should be reviewed with a qualified tax professional.

Are box spread loans better than margin loans?

Not necessarily. The answer depends on borrowing needs, flexibility requirements, risk tolerance, and overall financial objectives.

Who should consider a box spread loan?

Typically, high-net-worth investors have substantial taxable portfolios and sophisticated liquidity planning needs.

Can retirees use box spread loans?

Potentially, although careful evaluation of risk and sustainability is critical.

Are box spread loans available through financial advisors?

Yes. Some advisors and specialized platforms now facilitate these strategies for eligible clients.

Need Liquidity Without Selling Appreciated Investments?

Box spread financing may be worth exploring when the borrowing need is meaningful, the collateral base is strong, and the planning benefit outweighs the added complexity.

VIP Wealth Advisors can help evaluate how portfolio-backed lending, concentrated stock risk, tax impact, and long-term liquidity goals fit together before you make a major borrowing decision.