A grandparent-owned 529 plan may offer estate planning and financial aid advantages, but for many families, a parent-owned 529 remains the simpler and more practical college savings strategy.

Key Takeaways

- Under current FAFSA rules, grandparent-owned 529 plans are not counted as assets and withdrawals no longer count as student income.

- Parent-owned 529 plans have only a modest impact on financial aid calculations and often provide the simplest structure.

- Grandparent ownership can support estate planning goals and family gifting strategies.

- Additional complexity, coordination, and potential state tax considerations can outweigh the benefits for some families.

- The best structure depends on who is funding education, who should control the assets, and whether financial aid planning is truly relevant.

A Question More Families Are Asking (For Good Reason)

If you’ve been researching college savings strategies lately, you may have come across a recurring idea: “Instead of putting the 529 plan in the parents’ name, it might be better to put it in the grandparents’ name.”

At first glance, it sounds like a clever optimization. A small structural tweak that could potentially unlock better financial aid outcomes. And for years… that was partially true. But today, the rules have changed, and most of what you’ll find online hasn’t fully caught up.

Ultimately, the core issue isn't simply determining "Which option is superior?" Rather, it is: "Which approach is the most practical fit for your family's unique situation?"

- What Changed Under FAFSA Rules

- Should Grandparents Own the 529?

- Parent-Owned 529 Plans

- Grandparent-Owned 529 Plans

- Potential Benefits

- Important Tradeoffs

- A Better Way to Think About It

- What We Typically See Works Best

- When Grandparent Ownership Makes Sense

- When Simplicity Wins

- The Bottom Line

- Frequently Asked Questions

What Changed (And Why You’re Seeing This Advice Everywhere)

The surge in this strategy comes from a relatively recent shift in financial aid rules under the FAFSA Simplification Act.

Here’s the simple version.

How It Used to Work

- A 529 owned by grandparents did not count as an asset on financial aid forms

- But when money was withdrawn, it was treated as student income

And student income carries the heaviest penalty in the aid formula. In practical terms, using that money could significantly reduce financial aid eligibility.

How It Works Now

Today:

- Grandparent-owned 529 plans are still not counted as assets

- And now, withdrawals are no longer counted as student income

That old penalty? Gone. This is the entire reason the strategy is getting attention again.

The FAFSA rule change removed the biggest historical drawback of grandparent-owned 529 plans, which is why this strategy has resurfaced across financial planning discussions.

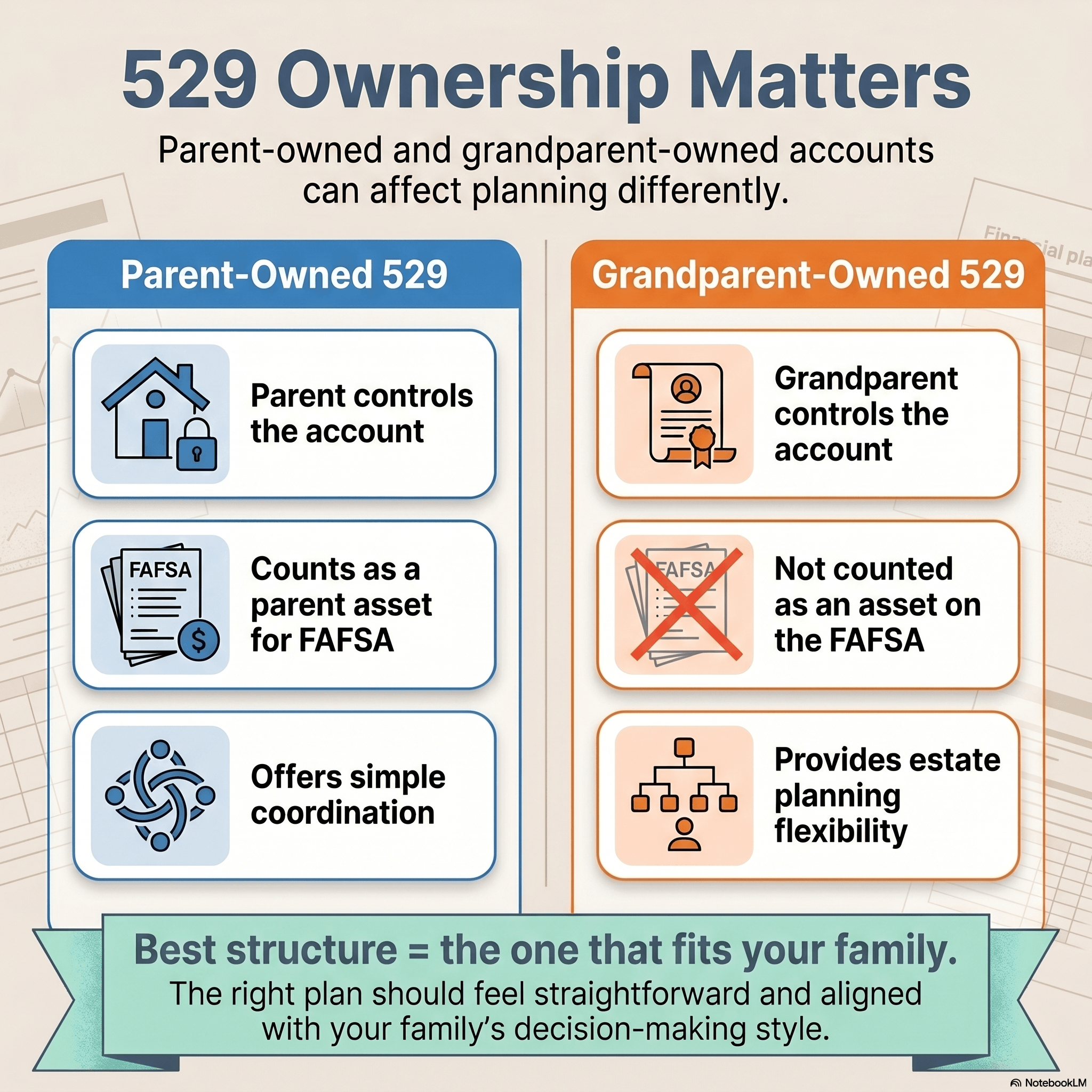

Parent-Owned vs. Grandparent-Owned 529 Plans at a Glance

While FAFSA rule changes have made grandparent-owned 529 plans more attractive, the right structure depends on factors beyond financial aid alone. Here's a side-by-side look at the key differences families should consider.

So… Should You Put the 529 in a Grandparent’s Name?

This is where it’s easy to get pulled into a simple answer. But the reality is more nuanced.

For some families, it can make sense. For many others, it doesn’t change much or can even complicate things.

Let’s walk through both sides in plain English.

| 529 Ownership Structure | How It Works | Potential Benefit | Potential Tradeoff | Best Fit |

|---|---|---|---|---|

| Parent-Owned 529 | The parent owns and controls the account. It is treated as a parent asset for financial aid purposes. | Simple, centralized, and easy to coordinate. Only a small portion is typically counted in aid calculations. | It is still visible on the FAFSA as a parent asset. | Families that value control, clarity, and a streamlined college funding plan. |

| Grandparent-Owned 529 | The grandparent owns and controls the account. It is not counted as an asset on the FAFSA under current rules. | May support financial aid positioning and estate planning goals. | Adds another decision-maker and may create coordination, timing, or state tax benefit issues. | Families where grandparents are leading the funding effort or estate planning is a key objective. |

Note: Some private colleges using the CSS Profile may evaluate grandparent-owned 529 plans differently.

The question isn’t whether grandparent ownership is better. The question is whether it fits how your family actually operates.

What a Parent-Owned 529 Looks Like

This is the most common setup.

- The parent owns the account

- It’s considered a parent asset for financial aid purposes

- Only a small portion (up to about 5.64%) is factored into aid calculations

In other words, it has a relatively modest impact.

More importantly, it keeps everything simple and under your control.

What a Grandparent-Owned 529 Looks Like

In this structure:

- The grandparent owns the account

- It is not counted at all on the FAFSA

- Withdrawals do not affect financial aid under current rules

On paper, that sounds like a clear advantage.

But that’s only part of the story.

Where a Grandparent-Owned 529 Can Be Helpful

1. It Can Help With Estate Planning

If grandparents are planning to help fund education anyway, a 529 can be a very efficient way to do it.

- The money is removed from their taxable estate

- They can still maintain control over how it’s used

- They can contribute large amounts using special gifting rules

For families thinking long-term, this is often the strongest reason to use this structure.

2. It May Improve Financial Aid Positioning (In Certain Cases)

Because the account isn’t counted as an asset, it can help families who are:

- Close to financial aid eligibility thresholds

- Experiencing fluctuating income

- Trying to manage how their financial picture appears on paper

That said, many high-income families find that financial aid is already limited regardless of structure. So while this benefit exists, it’s often not the deciding factor.

3. It Allows Grandparents to Stay Directly Involved

Some families like the idea of grandparents having a defined role in funding education.

In those cases, owning the 529s themselves can feel intentional and meaningful.

The Real-World Tradeoffs: What You Won’t Often Find in Print

This is where the real-world tradeoffs start to matter.

Because while the structure can work well, it introduces a few things that aren’t always obvious upfront.

1. You’re Adding Another Decision-Maker

When a parent owns the 529, decisions are straightforward.

When a grandparent owns it:

- They control when money is distributed

- They decide how and when it’s used

- Coordination becomes necessary

In many families, this works smoothly. In others, it can create friction especially when timing matters.

2. It Can Make Things More Complicated Than They Need to Be

Instead of one plan, you may now have:

- Multiple accounts

- Different owners

- Coordination around distributions and timing

None of this is unmanageable. But it does add layers that don’t exist in a simpler structure.

3. You Could Miss Out on State Tax Benefits

Many states offer tax incentives for contributing to a 529 plan.

But those benefits often depend on:

- Who owns the account

- Where they live

If grandparents are in a different state, your family may lose out on those benefits entirely.

4. Not All Schools Use the Same Rules

While FAFSA has simplified things, some private colleges use a different system called the CSS Profile.

These schools often take a more detailed look at family finances.

And in some cases, they may still consider grandparent-owned 529 plans. So the “invisible” advantage doesn’t always hold.

A Better Way to Think About This Decision

It’s easy to get caught up in optimizing a single variable, like financial aid.

But for most families, the better question is:

What structure would actually make this easier, more efficient, and better aligned with how we operate as a family?

Because college funding doesn’t happen in a vacuum.

It’s part of a broader financial life that includes:

- Cash flow

- Taxes

- Family dynamics

- Long-term planning

What We Typically See Works Best

Parent-Owned 529 as the Foundation

- Keeps control centralized

- Simplifies decision-making

- Preserves flexibility

Grandparent Contributions as a Complement

- Grandparents can still contribute

- They can gift into the parent-owned plan

- Or maintain a separate account if estate planning is a priority

This approach creates balance:

- Simplicity where it matters

- Flexibility where it adds value

When a Grandparent-Owned 529 Makes the Most Sense

This structure tends to work well when:

- Grandparents are leading the funding effort

- Estate planning is a key objective

- The family communicates clearly and consistently

- Financial aid eligibility is a real consideration

In these cases, the strategy becomes purposeful, not just tactical.

When Simplicity Is the Better Choice

A parent-owned 529 is often the better fit when:

- You want full control over decisions

- You value simplicity and clarity

- State tax benefits matter

- Financial aid isn’t a major factor

In these situations, keeping things streamlined usually leads to better outcomes.

Why This Decision Matters More Than It Seems

At first, this feels like a technical detail.

But it’s really about something bigger: How your family makes financial decisions.

There’s no shortage of strategies online. But not all of them are built for real life.

The goal isn’t to find the most clever workaround.

It’s to build a plan that works consistently, predictably, and without unnecessary complexity.

The Bottom Line: It’s Not About the “Best” Strategy

A grandparent-owned 529 used to be a workaround for financial aid rules.

Today, it’s better understood as:

An estate planning tool that may offer some additional planning flexibility.

For some families, that’s valuable.

For others, it’s unnecessary.

A Simple Way to Think About It

If you’re trying to decide, start here:

- Who is funding the education?

- Who should have control over the money?

- How important is simplicity?

- Do financial aid considerations actually apply?

Once those answers are clear, the right structure usually becomes obvious.

Final Thought: The Right Plan Should Feel Straightforward

The best financial decisions don’t feel complicated.

They feel aligned.

They reflect how your family actually operates, not how a strategy looks on paper.

Because at the end of the day, the goal isn’t just to fund college.

It’s to do it in a way that’s thoughtful, efficient, and easy to execute when the time comes.

Frequently Asked Questions

Does a grandparent-owned 529 affect financial aid?

Under current FAFSA rules, it does not count as an asset, and withdrawals are not treated as student income.

Is a grandparent-owned 529 better than a parent-owned 529?

Not necessarily. It depends on your family’s goals, including control, tax considerations, and whether financial aid is a factor.

Can grandparents contribute to a parent-owned 529 plan?

Yes. This is often the simplest and most effective approach.

Do all colleges treat 529 plans the same way?

No. Some private colleges using the CSS Profile may evaluate grandparent-owned 529 plans differently.

What is the biggest downside of a grandparent-owned 529?

Loss of control and added complexity, particularly around coordinating distributions.

Are there tax benefits to using a grandparent-owned 529?

There can be estate planning benefits, but state-level tax advantages may be reduced or lost depending on where the grandparents live.

Wondering Which 529 Strategy Makes Sense for Your Family?

College funding decisions rarely exist in isolation. The right 529 structure should fit your family's broader financial plan, tax situation, estate planning goals, and financial aid considerations.

If you're evaluating how to fund education while balancing long-term wealth planning, we'd be happy to help you think through the tradeoffs.