A tender offer is not just a chance to sell - it's a high-stakes decision about concentration risk, taxes, and how much of your financial future you want tied to a single company.

Key Takeaways

- Tender offers can create real liquidity, but they also create decision pressure that often leads employees to act emotionally instead of strategically.

- The core issue is usually not whether you can sell shares, but whether you should based on concentration risk, taxes, and life goals.

- If too much of your net worth is tied to one private company, you do not have a diversified portfolio—you have a concentrated thesis.

- Tax treatment can vary significantly depending on whether you hold NQSOs, ISOs, or RSUs, and whether the transaction is company-funded or investor-led.

- For many high-income professionals, a partial liquidity strategy is often the most balanced path because it reduces risk while preserving upside.

There’s a moment that happens quietly for many high-income professionals working at late-stage private companies.

You open an email.

It’s from your company.

“We’re offering employees the opportunity to sell shares.”

For the first time, your equity—something that’s lived in spreadsheets, dashboards, and theoretical valuations—suddenly feels real.

Liquid. Tangible. Life-changing.

And that’s exactly where the trap begins.

Because while tender offers are often framed as opportunities, they are just as often decision traps, moments where even highly intelligent, successful people make deeply flawed financial choices.

Not because they lack intelligence.

But because they lack clarity.

This article is about bringing that clarity.

What a Tender Offer Really Is (And What It Isn’t)

At its core, a private company tender offer is a structured opportunity to sell shares either back to the company or to outside investors.

You already know the basics:

- There’s a window (often ~20 business days)

- You can only sell a portion (commonly 10–25%)

- Participation may be capped or prorated

- Demand often exceeds supply

You’re not deciding whether you can sell.

You’re deciding whether you should.

And that’s a fundamentally different question.

Why Tender Offers Exist (Hint: It’s Not Just About You)

Companies don’t run tender offers out of generosity.

They run them because:

- Employees are sitting on illiquid wealth and getting restless

- Early investors want partial exits

- New investors want access before a potential IPO

- The company wants to control secondary market activity

In other words, this is a capital markets event, not a personal finance favor.

Understanding that changes your posture.

You’re not being “given” liquidity.

You’re being invited to participate in a transaction that benefits multiple parties, some of whom are far more informed than you.

The Real Risk: You Don’t Have a Portfolio, You Have a Thesis

Most employees approaching a tender offer don’t think in these terms, but they should.

If a large portion of your net worth is tied to one private company, you don’t have a diversified financial life.

You have a single concentrated bet.

A thesis.

And it usually sounds like this:

“This company is going to be huge.”

Sometimes that thesis is right.

Think SpaceX.

Sometimes it isn’t.

The problem is that your financial life becomes disproportionately exposed to one outcome, one leadership team, one market cycle, one execution path.

A tender offer is your first real opportunity to de-risk that thesis.

And most people don’t take it seriously enough.

The Psychological Battlefield (Where Decisions Go Wrong)

The math is important. But psychology is everything.

When people face this decision, they’re not thinking like analysts.

They’re thinking like humans:

- “What if I sell and this becomes the next generational company?”

- “What if I hold, and this was my one shot at life-changing liquidity?”

- “What if I regret this forever?”

This is not a spreadsheet problem.

This is a regret minimization problem.

And left unchecked, it leads to two common mistakes:

1. The “All In” Trap

You don’t sell anything.

You convince yourself the upside is too great to dilute.

You stay fully concentrated.

2. The “Panic Liquidity” Move

You sell as much as possible without a plan.

You react to the moment rather than developing a strategy.

Both are emotional responses dressed up as rational decisions.

The VIP Framework: How to Actually Make This Decision

Here’s how we reframe this with clients.

Not as a binary “sell or hold,” but as a structured decision across five dimensions.

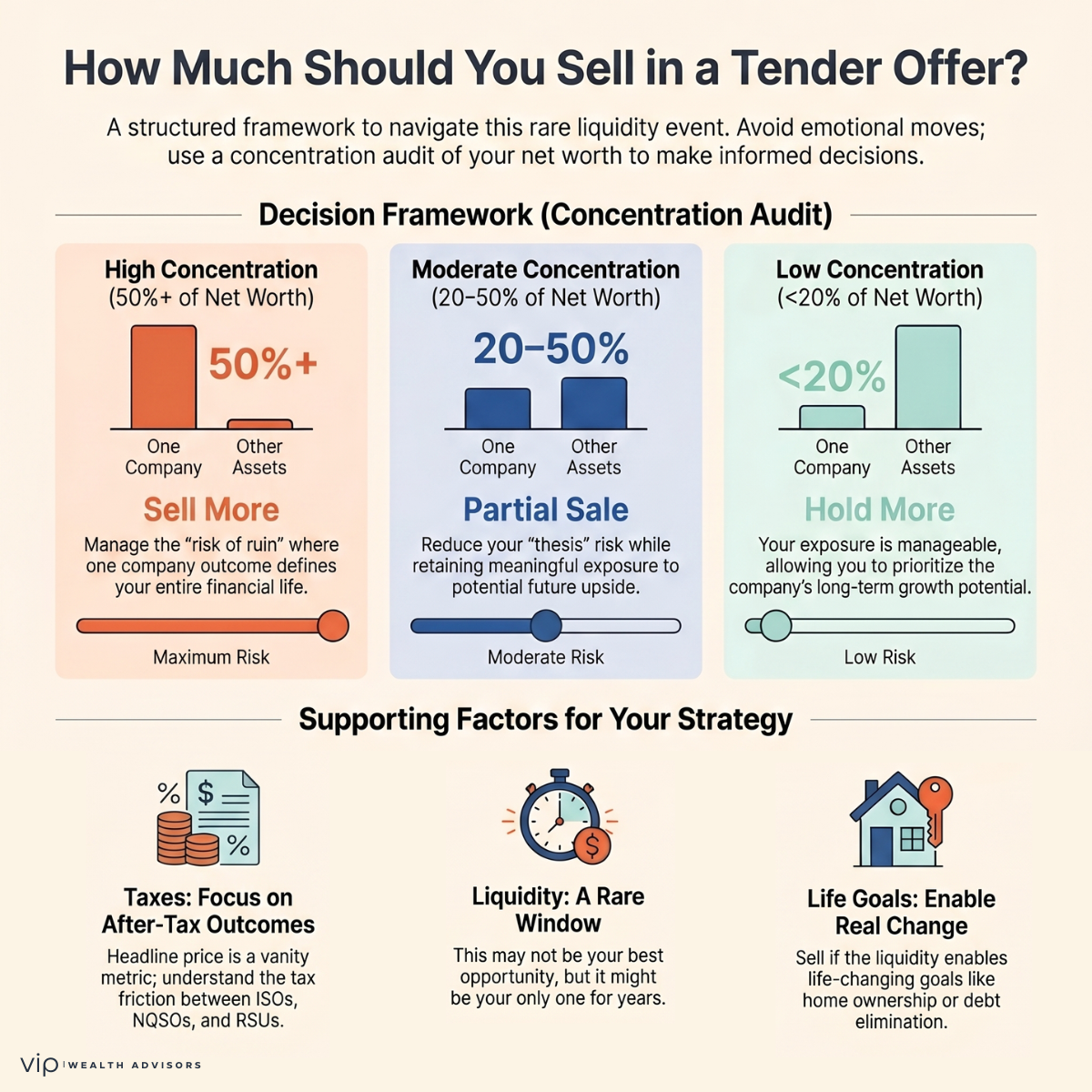

1. Concentration Audit: How Exposed Are You?

Start here.

What percentage of your net worth is tied to this company?

- Under 20% → manageable

- 20%–50% → meaningful

- 50%+ → this is your financial life

If you’re north of 50%, you’re not debating optimization.

You’re managing risk of ruin.

Diversification isn’t about maximizing returns.

It’s about making sure one outcome doesn’t define everything.

2. Liquidity Reality: Will You Get Another Shot?

Many employees assume:

“If I don’t sell now, I’ll just sell later.”

That assumption is often wrong.

While some companies run recurring programs, most do not.

- IPO timelines can stretch indefinitely

- Market conditions can shut the window

- The company may never go public

This may not be your best opportunity.

But it might be your only one for years.

3. Tax Friction: What Do You Actually Keep?

This is where decisions get distorted.

Because people anchor to the headline price, not the after-tax outcome.

Let’s break this down:

NQSOs

- Exercise spread = ordinary income

- Subject to withholding

- Immediate tax impact

ISOs

- No regular tax on exercise

- But potential AMT exposure

- If tendered immediately, often treated like NQSOs (especially in cashless structures)

RSUs

- Taxed as ordinary income at vest

- Sale creates capital gain/loss (usually minimal if immediate)

The Big Wildcard: Premium Over 409A

If you’re selling above your company’s internal valuation:

- Company-funded buybacks → often treated as ordinary income

- Investor-led transactions → more likely capital gain

That difference can be massive.

And it’s often misunderstood or ignored entirely.

4. Optionality: What Are You Giving Up?

Selling shares isn’t just about what you gain today.

It’s about what you give up tomorrow.

If the company:

- Doubles

- Triples

- Has a strong IPO

Every share you sold is gone.

This is the emotional anchor that keeps people from selling.

But here’s the reality:

You don’t need to capture 100% of the upside to change your life.

Partial liquidity can still leave you with meaningful exposure.

You’re not exiting the story.

You’re rewriting your role in it.

5. Life Alignment: What Does This Money Do For You?

This is the question almost no one asks.

What does selling actually enable?

- Paying off debt

- Funding a home

- Creating a safety buffer

- Reducing financial anxiety

- Buying back time

If liquidity doesn’t change anything in your life, holding more may make sense.

If it does?

Then this isn’t just a financial decision.

It’s a life decision.

Quick Decision Guide

If you want a simplified way to think about this decision, start here:

The Most Common Mistake: Treating This Like a Market Trade

Public market investors think in terms of:

- Valuations

- Multiples

- Timing

That mindset breaks down here.

Because this isn’t a liquid, repeatable decision.

You don’t get daily pricing.

You don’t get continuous access.

You don’t get unlimited chances.

This is closer to a once-in-a-cycle decision than a trade.

And it should be treated with that level of weight.

A More Sophisticated Approach: Partial Liquidity

For most high-income professionals, the optimal answer is not extreme.

It’s structured.

Something like:

- Sell enough to materially reduce concentration

- Retain enough to participate in future upside

- Coordinate with tax strategy

- Align proceeds with real-life goals

This isn’t about being right.

It’s about being balanced.

What You’re Really Deciding Here

A tender offer isn’t just a liquidity event.

It’s a decision about how much of your future you’re willing to leave in one place.

Smart employees don’t get this wrong because they lack intelligence.

They get it wrong because:

- They underestimate the concentration risk

- They ignore tax complexity

- They let emotion drive timing

- They fail to connect the decision to their actual life

The goal isn’t perfection.

The goal is intentionality.

Because the biggest risk in a tender offer isn’t selling too early.

It’s not having a strategy at all.

Q&A: Private Company Tender Offers

What is a tender offer in a private company?

A tender offer is a structured opportunity for employees or shareholders to sell shares back to the company or to outside investors, typically during a limited time window and subject to participation limits.

Should I sell shares in a tender offer for a private company?

It depends on your concentration risk, financial goals, tax situation, and likelihood of future liquidity. Many advisors recommend partial sales to reduce risk while maintaining upside exposure.

How many shares can I sell in a tender offer?

Most companies limit sales to a percentage of vested shares, typically 10% to 25%. Oversubscription may further reduce the amount you can actually sell.

How are tender offers taxed?

Tax treatment depends on the type of equity:

- NQSOs: ordinary income at exercise

- ISOs: potential AMT and possible reclassification if sold immediately

- RSUs: taxed as ordinary income at vest

Additional gains may be taxed as capital gains or ordinary income, depending on the structure of the tender offer.

Is the premium over 409A valuation taxed as capital gains?

Not always. If the company funds the buyback, the premium is often treated as ordinary income. If outside investors are purchasing shares, it may qualify for capital gains treatment.

Do I have to participate in a tender offer?

No. Participation is optional. However, if liquidity opportunities are rare, skipping a tender offer could delay your ability to access cash from your equity.

Will I get another chance to sell my shares?

Not necessarily. Some companies offer recurring tender offers, but many do not. IPOs or acquisitions may take years or never happen.

Should I sell all my shares in a tender offer?

For most individuals, selling all shares is not optimal. A partial sale allows for diversification while preserving exposure to future growth.

How do I decide how much to sell?

A common approach is to evaluate your total net worth and reduce exposure if your company stock represents more than 20%–30% of your assets, with more urgency above 50%.

Can a financial advisor help with a tender offer decision?

Yes. A financial advisor can analyze tax implications, concentration risk, and long-term strategy to help you make a more informed and structured decision.

Facing a tender offer and not sure how much to sell?

If a large share of your net worth is tied to one private company, this is not a decision to make casually. A structured plan can help you weigh concentration risk, taxes, future upside, and what liquidity would actually do for your life.

Talk through your tender offer strategy before the window closes.