Tax-managed long-short strategies can help investors defer taxes and diversify concentrated stock positions — but they do not eliminate taxes, and the real value often comes from risk reduction and planning flexibility.

Key Takeaways

- Tax-managed long-short strategies are designed to generate tax losses that can offset large capital gains, particularly from concentrated stock positions.

- These strategies primarily create tax deferral, not permanent tax elimination. Future embedded gains often replace the original gain.

- The biggest long-term benefit is often diversification and risk reduction rather than tax savings alone.

- Long-short strategies can introduce higher fees, leverage risk, tracking error, and complexity compared to simpler investment approaches.

- These strategies tend to work best for investors facing large one-time liquidity events such as IPOs, business sales, or concentrated stock exits.

- Tax deferral becomes significantly more valuable when paired with advanced planning strategies such as charitable giving, estate planning, or relocation to lower-tax states.

The Pitch Sounds Brilliant

Wall Street has a new favorite solution for high-income investors sitting on large capital gains:

“We can help you diversify your concentrated stock position without paying taxes.”

That’s the hook.

The mechanism?

Tax-managed long-short strategies.

At first glance, it sounds like financial alchemy:

- Generate losses

- Offset gains

- Reinvest into a diversified portfolio

- Avoid taxes

But like most things in wealth management, the reality is more nuanced.

What These Strategies Actually Do

A tax-managed long-short strategy typically:

- Goes long high-conviction stocks

- Shorts overvalued or weak companies

- Uses leverage (often 130/30 structures)

- Actively trades to harvest tax losses

The promise:

- Accelerate loss harvesting

- Offset large capital gains

- Help you exit concentrated positions more efficiently

That’s the theory.

The Truth

This is not tax elimination. It’s a tax deferral.

Here’s what’s really happening behind the curtain:

Step 1 — You Generate Losses

Through active trading (not magically from shorts), the strategy realizes losses.

Step 2 — You Use Those Losses

You sell your concentrated stock and use the harvested losses to offset the gain.

Step 3 — You Reinvest

Now you own a diversified portfolio.

So far, so good.

The Reality: Relocating the Gain

Your new portfolio doesn’t come tax-free.

It comes with:

- Embedded unrealized gains

- Positions that will eventually be sold

- Future tax liability

You didn’t eliminate the tax. You moved it forward in time.

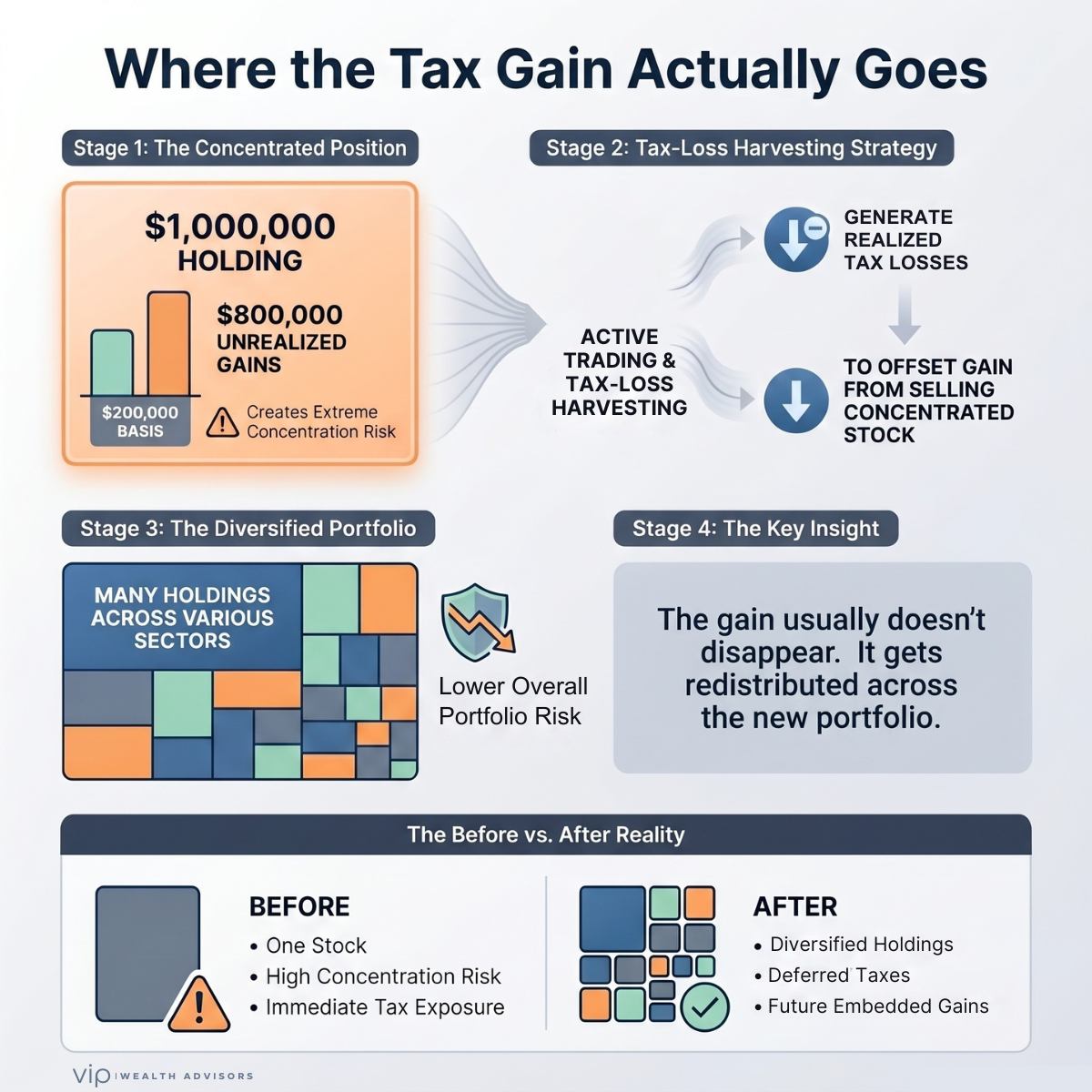

How Tax Deferral Actually Works

This simplified visual shows how tax-managed long-short strategies often relocate embedded gains into a diversified portfolio rather than permanently eliminating taxes.

Let’s Walk Through a Real Example

This is where the concept becomes clear.

Starting Point

You own a concentrated stock position:

- Value: $1,000,000

- Cost basis: $200,000

- Unrealized gain: $800,000

If you sell today, you’ll owe tax on that $800,000 gain.

Step 1: Introduce the Strategy

You allocate to a tax-managed long-short portfolio.

Over time, the strategy generates:

- $800,000 in realized losses through active trading

Step 2: You Sell the Concentrated Stock

- Realized gain: $800,000

- Offset by: $800,000 in harvested losses

✅ Tax owed today: $0

You’ve now:

- Fully exited the concentrated position

- Reinvested into a diversified portfolio

Step 3: What You Now Own (This Is the Critical Part)

Your portfolio is now diversified, which is a win.

But look under the hood:

- Portfolio value: $1,000,000

- Cost basis: ~$200,000

That means you now have $800,000 of embedded unrealized gains again.

Wait… how did that happen?

Because the losses you used didn’t come from nowhere.

They came from:

- Selling positions inside the strategy at a loss

- Rotating into new positions

- Continuing to stay invested in the market

So economically, your portfolio kept growing.

You did two things at the same time:

- Used losses to cancel out your original $800,000 gain

- Stayed invested in assets that appreciated

Those new assets now carry the gain instead.

A Cleaner Way to Visualize It

Before:

- One stock → $800,000 gain

After:

- Many stocks → $800,000 total gain

👉 The gain didn’t disappear

👉 It just got redistributed across the portfolio

Why Is the Cost Basis Still Low?

Your cost basis remains around $200,000 because:

- You didn’t “reset” the basis to $1,000,000

- You harvested losses, but stayed invested

- The portfolio’s appreciation created new unrealized gains

So now you hold:

- A diversified portfolio

- With the same economic gain, just in a different form

The Hidden Reality of Reinvestment

You used losses to unlock your concentrated stock…

But you replaced it with a diversified portfolio carrying similar embedded gains.

Why This Matters

Because eventually:

- When you sell these new positions

- The $800,000 gain becomes taxable

👉 That’s the deferred tax coming back.

The Honest Framing

You didn’t eliminate the gain — you relocated it.

From:

- One risky stock

To:

- A diversified portfolio

Step 4: The Future

At some point, when you sell:

- That $800,000 gain becomes taxable

- The tax bill returns

What Actually Happened

You didn’t avoid the tax.

You:

- Eliminated it today

- Recreated it in a new portfolio

- Gained diversification and flexibility

Why This Still Matters

Even though the tax is deferred, two important things changed:

- You eliminated single-stock risk

- You gained control over when taxes are paid

That control is where planning value lives.

You used losses to exit your concentrated position, but replaced it with a diversified portfolio carrying future gains.

Where This Becomes Powerful

Deferral becomes real savings when paired with:

- Lower future income

- Relocation to a lower-tax state

- Charitable strategies

- Estate planning (step-up in basis)

Without that?

You likely end up paying similar taxes, just later.

Why That Still Might Be Worth It

Here’s where sophisticated investors lean in.

Even though the tax is deferred, two powerful things happen:

1. You Eliminate Concentration Risk

This is the real win.

Holding a single stock:

- Creates massive downside risk

- Introduces emotional decision-making

- Often leads to poor timing

Diversification:

- Reduces volatility

- Improves long-term outcomes

- Protects against catastrophic loss

Concentration builds wealth. Diversification preserves it.

2. You Gain Control Over Timing

Deferral creates optionality.

You now control:

- When gains are realized

- Which assets to sell

- How taxes are triggered

That flexibility opens the door to smarter planning.

When Deferral Becomes Real Tax Savings

This is where elite planning separates from average advice.

Deferral turns into permanent tax savings when paired with:

- Moving to a lower-tax state

- Retiring into a lower income bracket

- Donating appreciated assets

- Using charitable trusts

- Holding assets until death (step-up in basis)

The strategy itself doesn’t create the savings. What you do after does.

Where These Strategies Go Wrong

1. Overpaying for Complexity

These strategies often cost:

- 40–50 bps management fee

- 25–30 bps financing cost

You’re approaching 1% all-in before alpha.

2. Underperformance Risk

- Limited upside in bull markets

- Tracking error vs benchmarks

- Mixed long-term results across funds

You’re not buying the S&P 500.

You’re buying a managed, hedged experience.

3. Misusing Leverage

To generate losses faster, some strategies increase leverage.

That introduces:

- Amplified downside risk

- Greater volatility

- Behavioral risk (clients panic)

4. Using It When It’s Not Needed

This is the biggest mistake.

If you don’t have:

- A large, immediate capital gain

- A need for rapid diversification

Then you’re likely paying for a solution to a problem you don’t have.

The Real Role of Long-Short Strategies

This is a tactical tax tool, not a core investment strategy.

Used correctly:

- It helps unwind concentrated positions

- It accelerates tax-loss harvesting

- It creates planning flexibility

Used incorrectly:

- It adds cost

- Adds complexity

- Dilutes returns

What Smart Investors Should Ask

Before implementing a strategy like this, ask:

- What problem are we solving — tax or concentration?

- How large is the tax benefit really?

- What are the all-in costs?

- What does the portfolio look like long-term?

- What is the exit strategy?

The Bottom Line

Tax-managed long-short strategies aren’t magic.

They’re a tool.

A sophisticated one, but still just a tool.

You’re not avoiding taxes.

You’re choosing when and how to deal with them.

And in many cases, the biggest value isn’t tax-related at all.

It’s this:

You finally move from a risky, concentrated position to a disciplined, diversified portfolio.

That’s where real wealth management begins.

How We Think About It at VIP Wealth Advisors

We don’t start with products or strategies.

We start with the decision:

Should you diversify?

If the answer is yes, then we evaluate:

- Tax impact

- Timing

- Strategy options

Long-short is one option.

Not the default. Not the answer. Just one tool in the toolkit.

Because real planning isn’t about complexity.

It’s about clarity.

Frequently Asked Questions About Tax-Managed Long-Short Strategies

What is a tax-managed long-short strategy?

A tax-managed long-short strategy is an investment approach that combines long positions (stocks expected to rise) with short positions (stocks expected to fall) while actively trading to generate realized losses. These losses can be used to offset capital gains elsewhere in an investor’s portfolio, improving after-tax outcomes.

How do long-short strategies generate tax losses?

Tax losses are typically generated through active trading and tax-loss harvesting, not simply from short positions losing money. Managers sell securities that have declined in value to realize losses, which can then offset gains from other investments.

Do short positions automatically create tax losses?

No. Short positions only create tax losses if they lose money, which happens when the stock price rises. However, at the same time, long positions in the portfolio are often gaining value. The strategy relies on active management and volatility, not just short losses, to generate usable tax losses.

Are tax-managed long-short strategies tax-free?

No. These strategies do not eliminate taxes — they primarily defer them. Losses used today to offset gains are often replaced by future gains embedded in the portfolio, which will eventually be taxed when realized.

What does tax deferral mean in this context?

Tax deferral means delaying the payment of taxes. Instead of paying capital gains tax today, the investor offsets gains with harvested losses and reinvests the proceeds. The tax liability is deferred until the new investments are eventually sold.

When do tax-managed long-short strategies make sense?

They are most effective when an investor has a large, one-time capital gain event, such as:

- Selling a business

- IPO liquidity

- Concentrated stock position sales

They are especially useful when losses need to be generated quickly.

Are these strategies suitable for long-term investing?

Not typically. These strategies are better viewed as tactical tools rather than core portfolio allocations. Long-term use can introduce unnecessary costs, complexity, and potential underperformance.

What are the main risks of long-short strategies?

Key risks include:

- Higher fees and financing costs

- Use of leverage

- Tracking error relative to benchmarks

- Limited upside in strong bull markets

- Complexity that may be difficult for investors to understand

Do long-short strategies outperform the market?

Not consistently. Many long-short strategies underperform traditional long-only benchmarks over time due to hedging, fees, and trading costs. Their primary value is tax management and risk control, not necessarily outperformance.

What is a 130/30 long-short strategy?

A 130/30 strategy means the portfolio is:

- 130% long (using borrowed capital)

- 30% short

This creates 100% net market exposure while allowing the manager to express both positive and negative views on stocks.

How does this strategy help with concentrated stock positions?

It allows investors to generate tax losses that can offset gains from selling a concentrated position. This can make it easier to diversify without triggering a large immediate tax bill.

Is diversification the main benefit of this strategy?

Yes — in many cases, diversification is the most valuable outcome. Reducing exposure to a single stock lowers risk and improves long-term portfolio stability. The tax strategy is simply a way to make that transition more efficient.

What are the costs associated with long-short strategies?

Typical costs include:

- Management fees (often 0.40% to 0.50%)

- Financing costs for leverage (0.25% to 0.30% or more)

Total costs can approach or exceed 0.75% annually before any performance considerations.

How does this compare to direct indexing?

Direct indexing:

- Lower cost

- Slower loss harvesting

- No leverage

Long-short strategies:

- Faster loss generation

- Higher cost and complexity

- Use leverage and shorting

Each has different use cases depending on timing and tax needs.

What happens when the strategy is unwound?

Unwinding the strategy typically triggers a taxable event. Any embedded gains in the portfolio may be realized, creating a future tax liability. This is why exit planning is critical.

Can this strategy eliminate capital gains taxes permanently?

Not on its own. Permanent tax savings occur only when the deferral is paired with additional planning strategies, such as charitable giving, relocating to a lower-tax state, or a step-up in basis at death.

Why are advisors increasingly using these strategies?

Rising market volatility, large embedded gains, and increased awareness of tax-efficient investing have driven adoption. They are particularly attractive for high-income investors facing significant tax events.

Should I use a tax-managed long-short strategy?

It depends on your situation. These strategies are best suited for investors with:

- Large, immediate capital gains

- Concentrated stock exposure

- A need for rapid diversification

For many investors, simpler and lower-cost strategies may be more appropriate.

Need Help Evaluating a Concentrated Stock Position?

Tax-managed long-short strategies can be useful in the right situation — but they are not a universal solution. The real question is whether the strategy improves your long-term financial outcome after taxes, fees, risk, and planning considerations.

At VIP Wealth Advisors, we help investors evaluate diversification decisions with clarity, not product hype.