Trump Accounts are a new tax-deferred investment account for children that may complement, but not automatically replace, 529 plans, custodial accounts, or other long-term family savings strategies.

Watch: 3 Things to Know Before Opening a Trump Account

Key Takeaways

- Trump Accounts are not Roth IRAs for kids; they are closer to traditional IRA-style accounts with special childhood rules.

- The primary tax benefit is tax-deferred growth, not tax-free withdrawals.

- Eligible children born after December 31, 2024 and before January 1, 2029 may qualify for a $1,000 federal pilot contribution.

- Before age 18, investment choices are generally limited to qualifying low-cost U.S. index mutual funds or ETFs.

- For many families, the planning question is not whether a Trump Account replaces a 529 plan, but whether it fits alongside a broader savings strategy.

Congress officially launched Trump Accounts on July 4th, 2026, creating an entirely new investment account for children that is likely to generate both excitement and confusion.

You’ve probably already seen them described as “Roth IRAs for kids.” That’s incorrect. They’re also not 529 plans, custodial brokerage accounts, or savings accounts. Instead, Trump Accounts occupy their own space in the tax code, combining elements of a traditional IRA with several unique rules that apply only to minors. The name may dominate the headlines, but the planning opportunities and limitations are what deserve your attention.

For some families, opening a Trump Account will be an easy decision. For others, it may make sense to prioritize different savings vehicles first. As with most tax planning strategies, the value of the account depends less on what Congress called it and more on how it fits into your family’s long-term financial plan. Here’s what every parent should know.

What Is a Trump Account?

Trump Accounts were created under the One Big Beautiful Bill Act (OBBBA) through the addition of Internal Revenue Code Section 530A. Legally, they’re treated much like a traditional IRA, with several important modifications designed specifically for children. That distinction matters because the account’s tax treatment is fundamentally different from a Roth IRA.

Money contributed during childhood generally does not generate a tax deduction, but it can grow tax-deferred for years or even decades. Later distributions generally follow traditional IRA taxation rules, meaning investment earnings are typically taxed as ordinary income rather than received tax-free.

The key distinction is tax-deferred, not tax-free. That difference matters when comparing Trump Accounts to Roth IRAs, 529 plans, and taxable brokerage accounts.

In other words, the primary tax benefit isn’t tax-free withdrawals; it’s the ability to allow investments to compound for many years without annual taxation. That makes Trump Accounts much closer to retirement accounts than to college savings accounts.

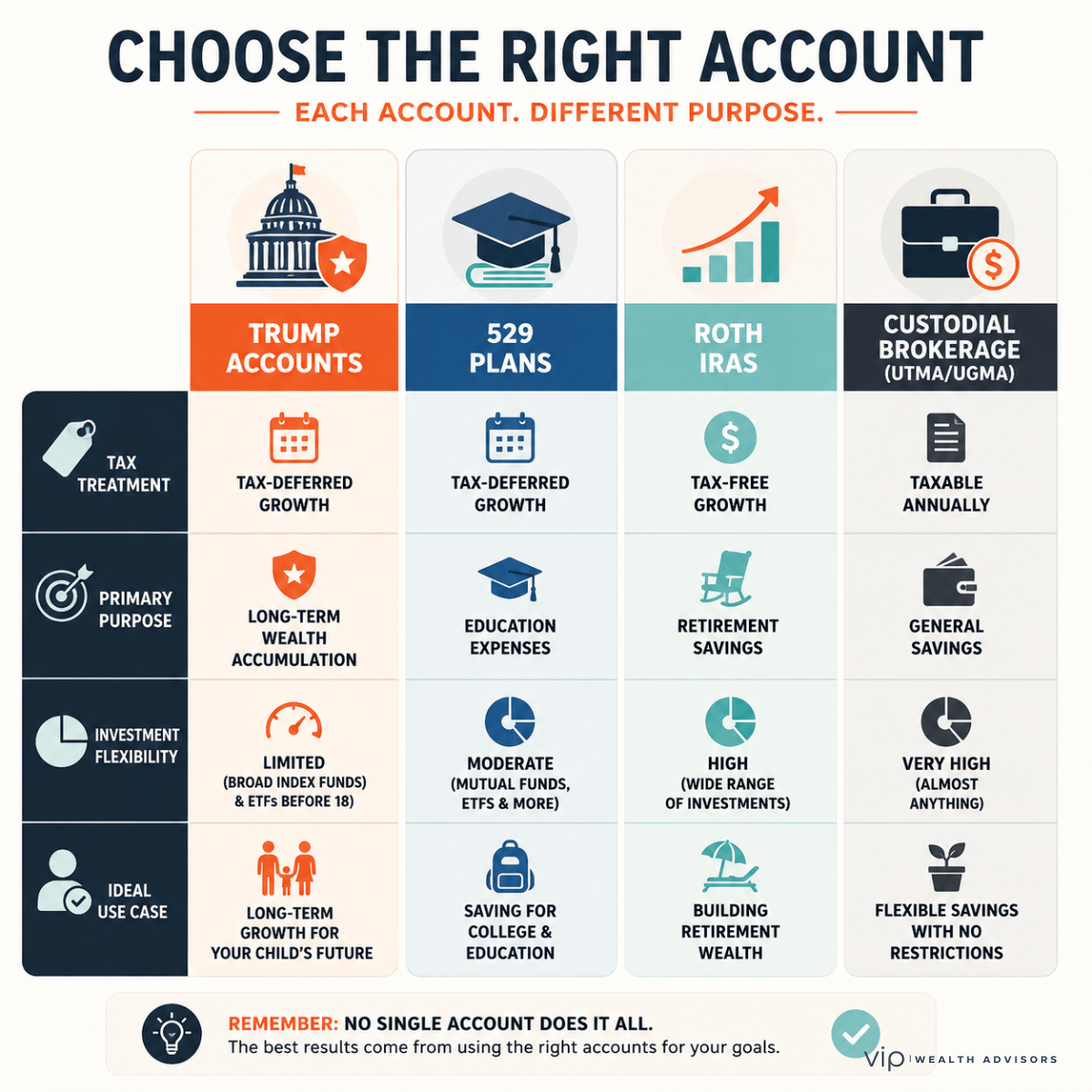

Trump Accounts vs. Other Popular Savings Accounts

| Feature | Trump Account | Roth IRA | 529 Plan | Custodial Brokerage (UTMA/UGMA) |

|---|---|---|---|---|

| Tax-deferred growth | ✅ | ❌ (tax-free growth) | ✅ | ❌ |

| Tax-free qualified withdrawals | ❌ | ✅ | ✅ | ❌ |

| Annual taxation on investments | No | No | No | Yes |

| Contributions deductible | No | No | State benefits may apply | No |

| Intended purpose | Long-term wealth accumulation | Retirement | Education | General savings |

| Restricted before age 18 | Yes | N/A | No | No |

Each account solves a different planning problem. Trump Accounts are not replacing 529 plans or Roth IRAs; they simply add another tool to the financial planning toolbox.

Which Account Is Built for Which Goal?

Every savings account solves a different planning problem. The best choice depends on what you're trying to accomplish—not which account is newest.

Who Can Open a Trump Account?

An eligible child generally must:

- Be under 18 at the time the account is established.

- Have a valid Social Security Number.

- Have a Trump Account election properly filed.

The account is initially established by an authorized adult, typically following this order:

- Legal guardian

- Parent

- Adult sibling

- Grandparent

Only one Trump Account may be established for each eligible child.

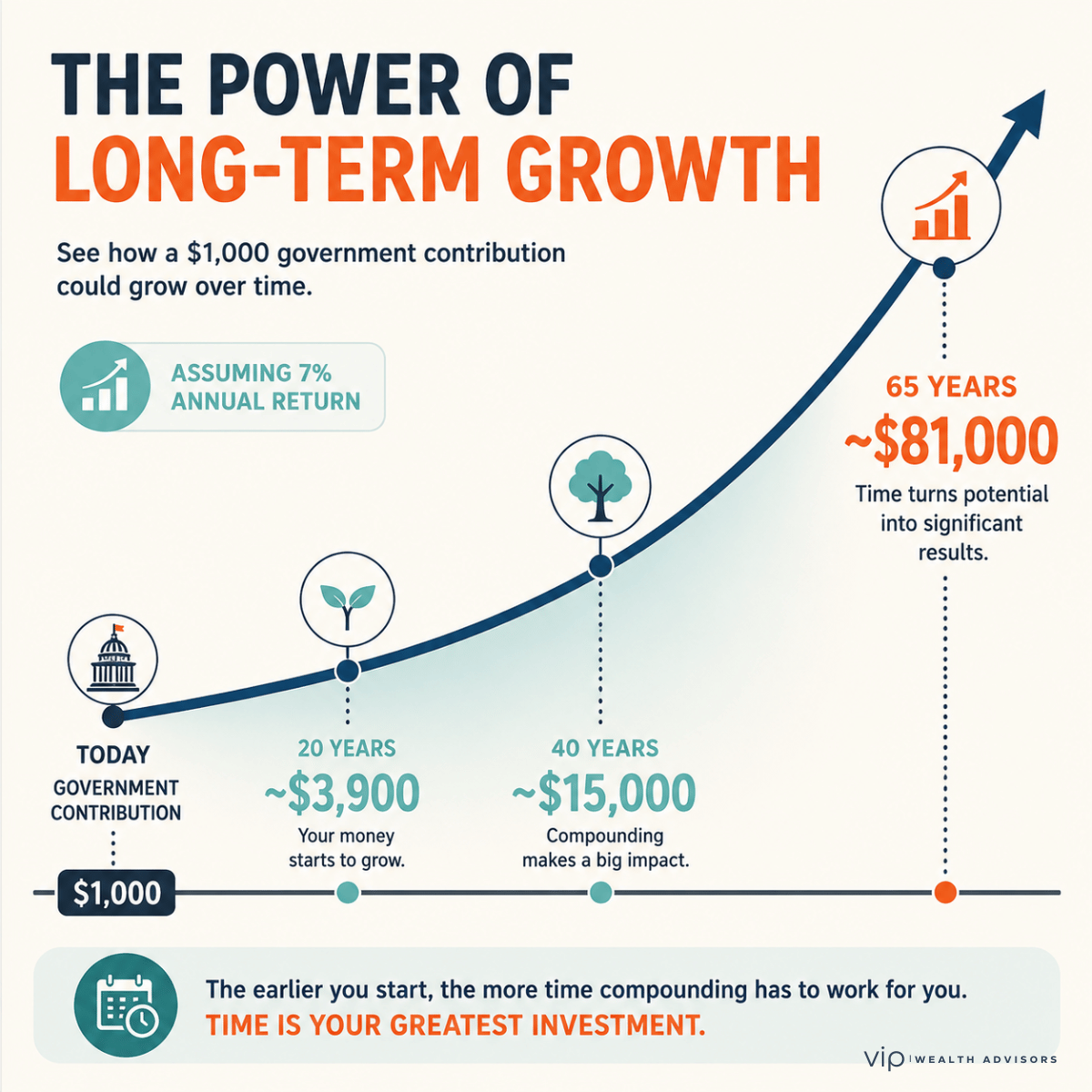

The $1,000 Government Contribution

One of the most talked-about features is the federal government’s $1,000 pilot contribution.

Children generally qualify if they:

- Were born after December 31, 2024,

- Before January 1, 2029,

- Meet the statutory eligibility requirements,

- Have a valid Social Security Number.

Unlike regular contributions, this government deposit does not count toward the annual contribution limit. While $1,000 may not sound life-changing today, time dramatically changes the math.

Time is often a more powerful wealth-building tool than the initial investment itself.

Assume that $1,000 earns an average annual return of 7%.

- After 20 years, it could grow to roughly $3,900.

- After 40 years, approximately $15,000.

- After 65 years, nearly $81,000.

No one knows what future investment returns will be, but this illustrates an important principle: time is often a more powerful wealth-building tool than the initial investment itself.

Time May Be the Biggest Advantage

The $1,000 government contribution isn't valuable because of its size today. Its potential comes from giving decades of compounding a chance to work.

How Contributions Work

Parents, grandparents, relatives, and others may generally contribute to a child’s Trump Account.

Before age 18:

- Annual contributions are generally limited to $5,000 (indexed for inflation beginning after 2027).

- Contributions are made with after-tax dollars.

- Contributions are not tax-deductible.

Several types of contributions receive special treatment, including government pilot contributions, qualified rollovers, and certain charitable or governmental contributions. One important distinction is that not every dollar entering the account counts toward the annual contribution cap.

Employers Can Help Fund Trump Accounts

One of the least discussed provisions may ultimately become one of the most valuable.

For employers, Trump Account contributions may become another way to support employees with children while expanding family-friendly benefit programs.

Beginning under new Internal Revenue Code Section 128, employers may contribute up to $2,500 annually (subject to future inflation adjustments) to an employee’s Trump Account or to the Trump Account of the employee’s dependent child through a qualifying written program.

For employers looking to expand family-friendly benefits, this could become an attractive alternative to traditional compensation. Whether companies broadly adopt these programs remains to be seen, but it’s an important feature that deserves attention.

Investment Choices Are Surprisingly Limited

Congress intentionally designed Trump Accounts around broad, low-cost investing. Before age 18, investments generally must consist of qualifying index mutual funds or ETFs that:

- Track a broad U.S. equity index,

- Do not use leverage,

- Have annual expenses of 0.10% or less, and

- Meet additional Treasury requirements.

That means you generally cannot invest in:

- Individual stocks

- Cryptocurrency

- Options

- Leveraged ETFs

- Sector-specific funds

This isn’t an oversight. The legislation intentionally favors diversified, low-cost, long-term investing over speculation.

While some investors may find these restrictions limiting, they’re also consistent with decades of research showing that broad-market index investing has historically outperformed many active investment strategies over long periods.

You Can’t Simply Take the Money Back

Before the child reaches the applicable age, distributions are generally prohibited except for a handful of very limited exceptions, including:

- Qualified rollovers

- Certain ABLE account rollovers

- Correction of excess contributions

- Death of the beneficiary

There are no general hardship withdrawals during the growth period.

If flexibility is the main priority, this may not be the right first account to fund.

That means parents should only contribute money they genuinely intend to leave invested for the child’s future. If flexibility is your primary goal, a custodial brokerage account may be more appropriate.

They’re Not Tax-Free Accounts, and That’s an Important Distinction

A misconception surrounding Trump Accounts is likely the belief that investment growth is completely tax-exempt. They aren’t. Instead, Trump Accounts operate much more like nondeductible traditional IRAs. Here’s a simplified example.

Suppose parents contribute a total of $25,000 during their child’s early years.

Decades later, the account has grown to $95,000.

Of that balance:

- $25,000 represents after-tax contributions (basis).

- $70,000 represents investment growth.

If the child later withdraws the money under ordinary IRA rules, the earnings portion generally becomes taxable as ordinary income, not long-term capital gains. Depending on age and circumstances, an additional 10% early distribution penalty may also apply unless an exception exists. That is a very different outcome than a Roth IRA, where qualified withdrawals can generally be received tax-free.

One Technical Rule Financial Planners Should Appreciate

One of the more interesting provisions involves basis tracking. Normally, nondeductible traditional IRA basis is aggregated across all of an individual’s traditional IRAs. Trump Accounts work differently.

The tax code requires that the basis within a Trump Account be tracked separately from the individual’s other IRAs. That separate accounting could become especially valuable if the beneficiary later considers a Roth conversion or other long-term tax planning strategies. While this won’t matter to every family immediately, it’s a meaningful planning feature that advisors will likely pay close attention to in the coming years.

Can a Trump Account Be Converted to a Roth IRA?

Potentially, yes. Once the special childhood rules expire and the account transitions into ordinary traditional IRA treatment, beneficiaries may generally have the ability to convert some or all of the account into a Roth IRA. Of course, a Roth conversion typically creates taxable income in the year of conversion, so timing becomes extremely important.

A beneficiary who converts during a lower-income year may pay substantially less tax than someone who waits until their highest-earning years. Ultimately, this may present a substantial planning opportunity for many families.

Should Parents Open One?

Like nearly every financial planning decision, the answer depends on your goals. If your primary objective is paying for college, a 529 plan will often remain the stronger choice because qualified education withdrawals are generally tax-free.

If your objective is to provide maximum flexibility for future spending, a custodial brokerage account may offer fewer restrictions. But if your goal is creating long-term wealth for your child, and especially if your child qualifies for the government’s $1,000 seed contribution, a Trump Account deserves serious consideration.

In many cases, the question isn’t whether a Trump Account should replace your existing strategy. It’s whether it should become one component of a broader savings plan that may also include a 529 plan, custodial investments, retirement accounts, and taxable investments.

The best financial plans rarely rely on a single account type. They combine multiple tools, each serving a different purpose.

A New Tool…Not a New Silver Bullet

The introduction of Trump Accounts marks the most substantial expansion of savings options for children in many years.

- They’re not Roth IRAs for kids.

- They’re not 529 plans.

- They’re not ordinary custodial investment accounts.

Instead, they introduce a new tax-deferred investment vehicle built around long-term compounding, limited investment choices, strict early-withdrawal rules, and a potentially valuable federal seed contribution for eligible children.

For families with a long investment horizon, those features may prove quite powerful. For others, alternate savings vehicles may remain the better fit. As with every major investment and tax planning opportunity, the right answer depends less on the account itself and more on how it fits into your family’s overall financial plan.

Frequently Asked Questions About Trump Accounts

What is a Trump Account?

A Trump Account is a new investment account for children created under Internal Revenue Code Section 530A. It generally functions like a traditional IRA with special rules governing contributions, investments, and distributions before age 18.

Are Trump Accounts the same as Roth IRAs?

No. Trump Accounts are not Roth IRAs. Investment earnings generally grow tax-deferred rather than tax-free, and post-18 distributions generally follow traditional IRA taxation rules.

Who qualifies for a Trump Account?

Generally, children under age 18 with a valid Social Security Number who meet the statutory eligibility requirements may have a Trump Account established on their behalf.

How much can be contributed each year?

The general annual contribution limit before age 18 is $5,000, indexed for inflation after 2027. Certain government and qualified contributions receive different treatment and may not count toward this limit.

Does every child receive the $1,000 government contribution?

No. The pilot program generally applies only to eligible children born between January 1st, 2025, and December 31st, 2028, who satisfy the statutory requirements.

Can grandparents contribute?

Yes. Grandparents, parents, relatives, and other individuals may generally contribute, subject to the applicable contribution rules and annual limits.

Can employers contribute?

Yes. Qualifying employers may contribute up to $2,500 annually under certain written contribution programs established under Internal Revenue Code Section 128.

Can the account invest in individual stocks?

No. Before age 18, investments are generally limited to qualifying low-cost index mutual funds and ETFs that satisfy Treasury requirements.

Can money be withdrawn before age 18?

Generally, no. The law allows only a handful of limited exceptions, such as certain rollovers, correction of excess contributions, and distributions following the beneficiary’s death.

Can a Trump Account later be converted to a Roth IRA?

In many cases, yes. Once the account transitions into ordinary traditional IRA treatment, a Roth conversion may be available, although taxes generally apply to the converted amount.

Are Trump Accounts better than 529 plans?

No. Each account serves a different purpose. A 529 plan is generally more advantageous for education funding, while a Trump Account is designed primarily for long-term, tax-deferred wealth accumulation.

Should every parent open one?

Not automatically. Families should evaluate Trump Accounts alongside other savings options such as 529 plans, custodial brokerage accounts, and retirement accounts to determine which combination best supports their long-term goals.

Is a Trump Account the Right Fit for Your Family?

Trump Accounts may create a meaningful planning opportunity, but the best choice depends on how they fit alongside your 529 plan, gifting strategy, tax picture, and long-term goals.

We can help you evaluate the tradeoffs and build a coordinated savings strategy for your child’s future.