Early exercising stock options can improve tax outcomes when the spread is low, but employees should model ISO/NSO treatment, AMT, 83(b) deadlines, liquidity risk, and concentration risk before exercising.

Key Takeaways

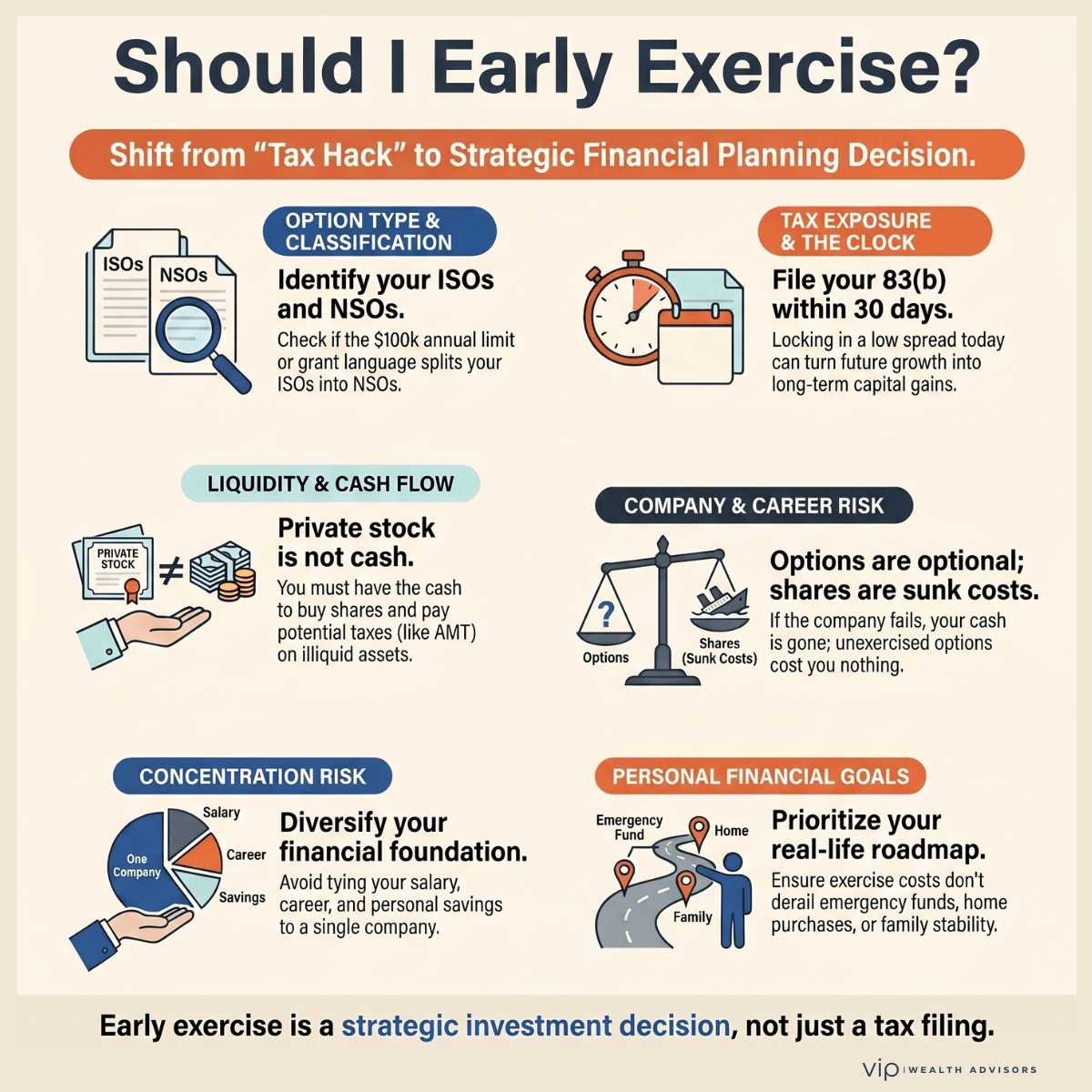

- Early exercise is both a tax decision and an investment decision because real cash is used to buy private company stock.

- ISOs and NSOs are taxed differently, and a grant labeled as an ISO may partly be treated as an NSO under the ISO $100,000 rule.

- A timely 83(b) election is often central to early exercise planning, and the 30-day filing deadline should be treated as absolute.

- ISO exercises can create AMT exposure even when shares are not sold and no cash is received.

- The strongest early exercise cases usually involve a low spread, manageable exercise cost, strong liquidity, and a realistic plan for company and concentration risk.

Stock options can be a significant wealth-building opportunity in a compensation package, especially for employees at private companies with meaningful growth potential. They can also create one of the easiest ways to make a large financial decision before the risks are fully understood. That tension becomes especially important when an employee can exercise stock options early.

Early exercising sounds simple. Instead of waiting for your options to vest, you exercise them early and purchase the shares now. If the company grows substantially, you may start the capital gains clock sooner, reduce future ordinary income, and potentially improve your after-tax outcome. In the right situation, early exercise can be an elegant tax-planning move.

The problem is that early exercise is not simply a tax strategy. It is also a liquidity decision, a company risk decision, a career risk decision, and a concentration risk decision. You are not just locking in a low tax cost. You are taking real cash and using it to buy private company stock that may be difficult to sell, may decline in value, or may never become liquid.

There is another layer as well. If your options are labeled as incentive stock options (ISOs), you still need to determine whether the entire grant qualifies for ISO treatment. The tax code imposes a $100,000 annual limit on ISOs, and an early exercise provision can have unexpected consequences if the grant language is not carefully drafted.

That does not mean early exercise is bad. It means the decision deserves a serious framework.

The better question is not, “Should I early exercise my stock options?” The better question is, “Given my type of options, current exercise price, fair market value, tax exposure, liquidity, company risk, and personal financial goals, does early exercise improve my expected after-tax outcome without exposing me to unacceptable downside?”

That is the decision worth modeling before clicking the exercise button.

Early exercise should be reviewed through taxes, liquidity, company risk, and personal goals, not treated as a one-click tax shortcut.

What Does It Mean to Exercise Stock Options Early?

Early exercise means exercising stock options before they are vested, assuming your company’s equity plan allows it.

In a typical stock option grant, your options vest over time. You may receive 100,000 options, but they may vest over four years. If the plan does not allow early exercise, you generally cannot exercise the options until they vest. If the plan does allow early exercise, you may be able to exercise some or all of the options before they vest.

When you early-exercise, you are purchasing shares before the vesting schedule has fully played out. However, that does not mean you own all the shares free and clear. Unvested shares are often subject to a company repurchase right. If you leave the company before those shares vest, the company may be able to repurchase the unvested shares, often at the price you originally paid.

For example, assume you receive 100,000 stock options with an exercise price of $1 per share. The shares vest over four years. If your company allows early exercise, you may be able to pay $100,000 now and acquire the shares before they vest. If you leave after two years, half of the shares may be vested, while the company may have the right to repurchase the unvested half.

That is why early exercise is not the same as receiving fully vested shares. It is a strategy that changes the timing of the tax and ownership consequences, but it does not eliminate the vesting rules.

Early exercise may change when you buy the shares, but it does not erase vesting, repurchase rights, or employment-related risk.

Why Employees Consider Early Exercising Stock Options

Employees usually consider early exercise for one main reason. They believe the company’s value may rise substantially, and they want to exercise while the tax cost is still low.

This can be especially attractive when the exercise price is equal to or close to the stock's current fair market value. If there is little or no spread between the exercise price and the fair market value at the time of exercise, the current tax cost may be modest. If the company later becomes far more valuable, more of that future appreciation may potentially receive capital gain treatment instead of being taxed as compensation.

Early exercise may also start the capital gains holding period sooner. That can matter if the shares eventually become liquid through a tender offer, acquisition, or IPO. With incentive stock options, early exercise may also help begin the holding period required for a qualifying disposition, although ISO rules are more complicated and must be handled carefully.

There is another reason employees consider early exercise. Waiting can make the eventual exercise decision much more expensive. If the company’s 409A valuation increases significantly, the spread at exercise may widen. For NSOs, which can create a large ordinary income tax event. For ISOs, this can create a significant alternative minimum tax adjustment.

In other words, early exercise may be attractive because it can move the tax decision from a future high-valuation moment to a current low-valuation moment. That can be powerful, but only if the employee can also handle the cash risk.

The tax opportunity is strongest when the current spread is small, but the cash risk still has to fit the employee’s broader financial life.

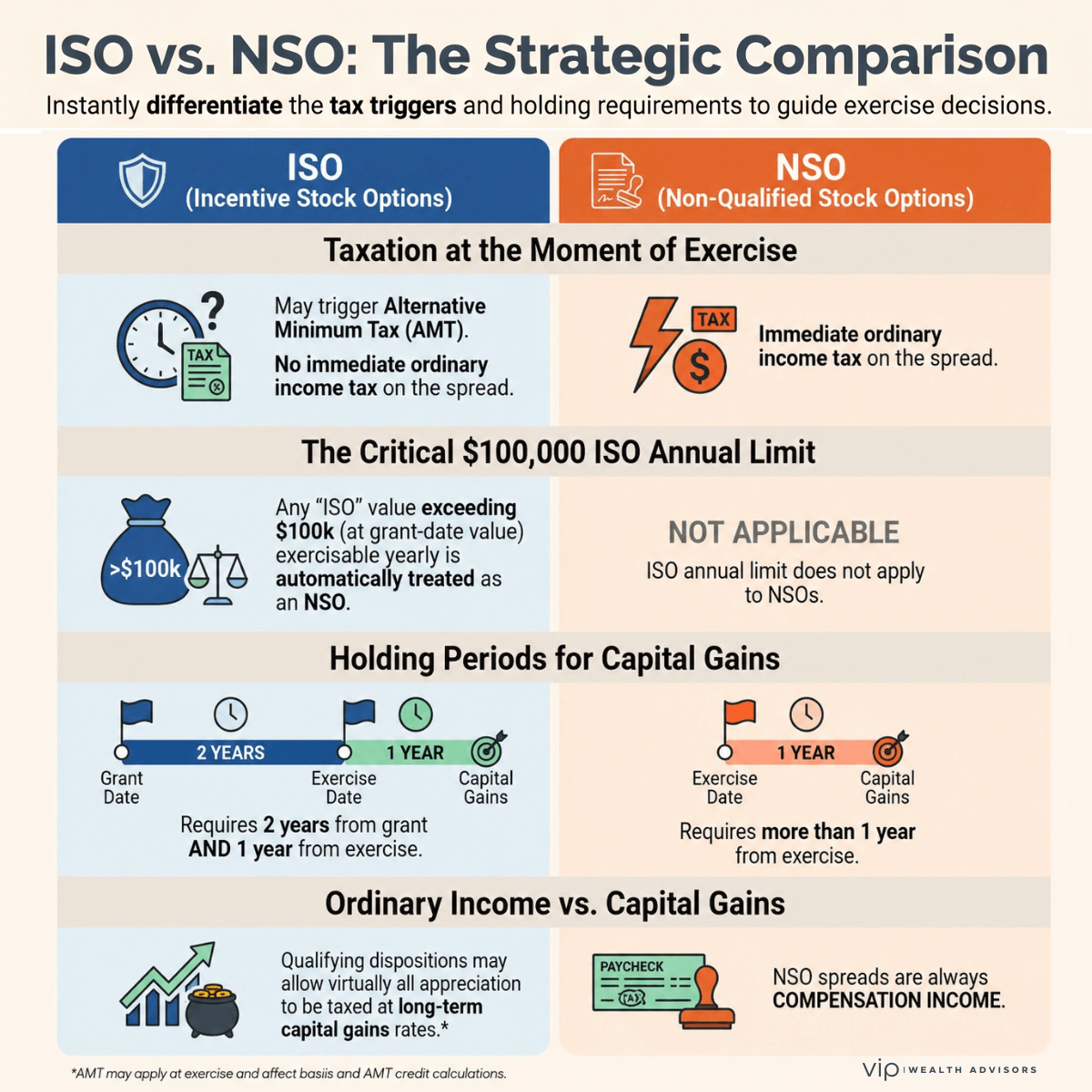

The Difference Between ISOs and NSOs

Before deciding whether to exercise early, you need to know what types of options you have. The tax treatment of incentive stock options, commonly called ISOs, differs significantly from that of nonstatutory stock options, commonly called NSOs or NQSOs.

ISOs are statutory stock options. They receive special tax treatment if specific requirements are met. NSOs are nonstatutory stock options. They are generally taxed as compensation when exercised if the fair market value of the stock is higher than the exercise price.

This distinction matters because early exercise does not work the same way for ISOs and NSOs.

It also matters because an option agreement may describe a grant as an ISO, while the tax rules may treat part of that grant as an NSO. This can happen because of the ISO $100,000 rule.

ISO vs. NSO: Why Option Type Changes the Tax Strategy

The same exercise decision can produce very different tax outcomes depending on whether the shares are treated as ISOs or NSOs.

How ISOs Are Taxed

Incentive stock options can be tax-favorable if the rules are satisfied. There is generally no regular federal income tax when ISOs are granted. There is also generally no regular federal income tax when ISOs are exercised, assuming the ISO requirements are met, and the shares are not sold immediately. That sounds wonderful until the alternative minimum tax enters the room.

When you exercise ISOs and hold the shares past the end of the year, the spread between the exercise price and the fair market value at exercise may be included as an AMT adjustment. This means you may owe AMT even if you did not sell the shares or receive cash.

For example, assume you exercise 50,000 ISOs with a $5 exercise price when the fair market value is $35 per share. The spread is $30 per share. That creates a $1,500,000 AMT adjustment.

You may not owe AMT in every case, because the final result depends on your full tax picture. However, the risk is real. An employee can exercise ISOs, hold the shares, owe a large tax bill, and still have no liquidity from the stock.

For ISOs to receive favorable long-term capital gain treatment, the employee generally must satisfy both ISO holding period requirements. The shares generally must be held for more than two years from the grant date and more than one year from the exercise date. If the shares are sold before those holding periods are met, the sale is generally a disqualifying disposition, and part of the gain may be taxed as ordinary income.

Early exercise can help start the one-year exercise-date holding period earlier, but it does not remove the AMT issue. It also does not remove company risk, liquidity risk, or concentration risk.

How NSOs Are Taxed

Nonstatutory stock options are taxed differently. When NSOs are exercised, the spread between the fair market value and the exercise price is generally treated as compensation income.

For example, assume you exercise 50,000 NSOs with a $5 exercise price when the fair market value is $35 per share. The spread is $30 per share. That creates $1,500,000 of ordinary compensation income.

For an employee, that income is generally reported through payroll and may be subject to income tax withholding and employment taxes. After exercise, the shares have a tax basis that generally includes the amount paid plus the compensation income recognized. Any subsequent appreciation or depreciation is generally treated as a capital gain or loss when the shares are sold.

This is why early exercise can be especially powerful for NSOs. If the employee exercises when the fair market value equals the exercise price, the taxable spread may be zero. If the employee makes a timely Section 83(b) election, future appreciation may avoid being taxed as compensation as the shares vest.

That is the golden pathway. The trapdoor is that the employee has now used real cash to purchase private company shares.

The ISO $100,000 Rule: Why Part of Your ISO Grant May Actually Be Treated as an NSO

There is another ISO rule that employees often miss. Even if your option agreement says you received incentive stock options, the tax code limits how much ISO stock can first become exercisable in any calendar year.

Under Internal Revenue Code Section 422(d), if the aggregate fair market value of stock with respect to which ISOs are exercisable for the first time by an employee during any calendar year exceeds $100,000, the excess portion is treated as options that are not ISOs.

In plain English, this means the excess portion is generally treated as NSOs for tax purposes.

The $100,000 limit is not based on the stock's value when you exercise. It is based on the fair market value of the stock at the time the option was granted. This is a critical distinction because employees often assume the rule is based on the company's latter value. It is not. The calculation looks at the grant-date fair market value of the shares that first become exercisable in a given calendar year.

For example, assume an employee receives 200,000 options with an exercise price of $1 per share, and the fair market value on the grant date is also $1 per share. The total grant-date value is $200,000. If all 200,000 options first become exercisable in the same calendar year, only the first $100,000 of value can receive ISO treatment. The remaining $100,000 of value is treated as NSOs.

This is commonly referred to as an ISO/NSO split.

The rule can also apply when grants vest over time. Assume an employee receives 400,000 ISOs with a grant-date fair market value of $1 per share, and the options vest 25 percent per year over four years. Each year, 100,000 options first become exercisable. Because the grant-date fair market value of the options first exercisable each year is $100,000, the grant may fit within the annual ISO limitation.

Now assume the same employee receives 800,000 options with the same $1 grant-date fair market value and the same four-year vesting schedule. Each year, 200,000 options first become exercisable. Because $200,000 of the grant-date fair market value becomes exercisable each year, only $100,000 of each year’s amount qualifies for ISO treatment. The excess $100,000 per year is treated as NSOs.

This matters because the tax consequences are different. The ISO portion may qualify for ISO tax treatment if all requirements are satisfied. The NSO portion is generally taxed as compensation at exercise based on the spread between the fair market value and the exercise price.

An employee who does not understand the ISO/NSO split may believe the entire grant receives ISO treatment when, in reality, only part of it does.

The option agreement may call it an ISO, but the tax code gets the final vote.

A label in an equity portal is not the whole analysis. Employees should confirm whether the grant is entirely ISO, entirely NSO, or split.

How an ISO/NSO Split Works in Practice

An ISO/NSO split happens when a stock option grant exceeds the ISO $100,000 limitation. The grant may still be described as an ISO grant in casual conversation, but for tax purposes, it may be split into two components.

The first piece is the ISO portion. This portion falls within the $100,000 annual limitation. The second piece is the NSO portion. This is the excess portion that does not qualify for ISO treatment.

This split is not merely cosmetic. It changes the tax result at exercise and sale.

For the ISO portion, there is generally no regular federal income tax at exercise, but the spread may create an AMT adjustment if the shares are held. If the ISO holding period rules are satisfied, the eventual sale may qualify for long-term capital gains treatment.

For the NSO portion, the spread at exercise is generally treated as ordinary compensation income. For an employee, that income may be subject to payroll tax and withholding. Later appreciation of an asset after exercise may be a capital gain or loss.

This creates a planning issue. If an employee exercises what they believe is a pure ISO grant, but part of the grant is actually treated as NSOs, the exercise may result in ordinary income the employee did not expect.

That can be especially dangerous with private company stock. The employee may owe tax on the NSO spread even if the shares remain illiquid.

A single exercise transaction can therefore create two different tax results. Part of the exercise may create an AMT adjustment, while another part may create ordinary compensation income. The employee needs to know which shares are being exercised, how the company tracks the ISO and NSO portions, and how the tax reporting will work.

This is exactly why pre-exercise planning matters. The equity portal may show one grant, but the tax law may see two different instruments.

The Early Exercise Trap: How an Early Exercise Provision Can Accidentally Trigger the $100,000 Rule

The ISO $100,000 rule becomes even more complicated when a stock option grant includes an early exercise feature.

Treasury Regulation Section 1.422-4 explains that an option is considered first exercisable during a calendar year if it will become exercisable at any time during that year, assuming any service-based condition is satisfied. This is where early exercise provisions can create unintended consequences.

If an option grant allows the employee to exercise the entire grant immediately, even before vesting, then the entire grant may be considered first exercisable in the year of the grant. That can cause the ISO $100,000 limitation to apply to the entire grant immediately.

This is the hidden problem.

A company may intend to grant ISOs that vest over a four-year period. However, if the grant also allows the employee to early exercise the entire option immediately, the entire grant may be treated as first exercisable in the year of grant for purposes of the $100,000 rule. If the grant-date fair market value of the shares exceeds $100,000, the excess portion may be treated as NSOs.

For example, assume an employee receives 400,000 options with a $1 exercise price and a $1 grant-date fair market value. The options vest over four years, with 100,000 options vesting each year. Without early exercise, the grant may fit within the $100,000 annual ISO limitation because only $100,000 of stock first becomes exercisable each year.

Now, assume the option agreement allows the employee to exercise all 400,000 options immediately, even before vesting. Because the entire grant is exercisable immediately, the full $400,000 grant-date value may be considered first exercisable in the year of grant. Only $100,000 can qualify as ISOs. The remaining $300,000 may be treated as NSOs.

That is a major unintended consequence.

The employee may think they received a four-year ISO grant. The company may think it granted a four-year ISO grant. However, the early exercise feature may result in a large portion of the grant being treated as NSOs from the outset.

This does not mean early exercise is bad. It means the plan language matters.

How Grant Language Can Help Avoid Accidentally Tainting the Entire ISO Grant

Companies and their counsel can sometimes avoid this problem by carefully drafting the early exercise feature.

Rather than allowing the employee to exercise the entire option grant immediately, the agreement can limit early exercisability so that no more than $100,000 of ISO shares, measured by grant-date fair market value, first becomes exercisable in any calendar year.

The goal is to preserve ISO treatment for the portion that can validly qualify as ISOs while clearly identifying any excess as NSOs.

A grant agreement might provide that the option is intended to qualify as an ISO only to the maximum extent permitted under Section 422 of the Internal Revenue Code, including the $100,000 limitation. The agreement may also provide that any portion of the option that exceeds the ISO limitation will be treated as a nonstatutory stock option.

The agreement may also restrict early exercise so that early exercise is only permitted to the extent it would not cause the option to exceed the ISO $100,000 limitation. This can help prevent the entire grant from being treated as first exercisable in the year of grant.

Conceptually, the protective language aims to convey three things.

First, the option is intended to qualify as an ISO only to the extent permitted by law.

Second, any excess portion should automatically be treated as an NSO rather than jeopardizing the intended ISO portion.

Third, any early exercise right should be limited or structured so that it does not inadvertently cause more than $100,000 of grant-date fair market value to become exercisable in a single calendar year.

For example, a protective provision might say that, notwithstanding any early exercise feature, the portion of the option intended to qualify as an ISO shall not become exercisable for the first time in any calendar year to the extent the aggregate fair market value of stock subject to ISOs first exercisable by the optionee in that year would exceed $100,000, measured as of the applicable grant dates. The agreement could further provide that any portion that exceeds the limitation will be treated as a nonstatutory stock option.

That language is only conceptual. The exact language should be drafted by qualified equity compensation counsel. This is not an area where employees or companies should improvise. A few words in an option agreement can change the tax character of a large equity award.

Why Employees Should Care About the ISO/NSO Split Before Exercising

Employees should not assume that every option labeled “ISO” will receive ISO treatment.

Before exercising, an employee should ask the company or equity administrator whether any portion of the grant is treated as an NSO due to the $100,000 ISO limitation. The employee should also ask how the company tracks ISO and NSO shares, how the exercise platform identifies each portion, and how the tax reporting will work.

This is especially important when the grant is large, the company permits early exercise, or the employee exercises a large number of options in a single transaction.

The employee should also understand which shares are being exercised. If the exercise includes both ISO and NSO portions, the tax consequences may be blended. Part of the exercise may create an AMT adjustment. Another part may create ordinary compensation income. A single exercise transaction may therefore create two very different tax outcomes.

This is exactly why pre-exercise tax planning matters. The option portal may show one grant, but the tax law may see two different instruments.

What Is an 83(b) Election?

A Section 83(b) election is a tax election that allows a taxpayer to include the value of property in income when the property is transferred, rather than waiting until the property vests.

This matters because early exercised shares are often subject to vesting. Without an 83(b) election, tax may be due as the shares vest. If the stock appreciates during the vesting period, the employee may recognize more taxable income later.

With a timely 83(b) election, the tax event is generally pulled forward to the date the shares are acquired. If the fair market value equals the exercise price on that date, the taxable income may be zero or very small.

The deadline is critical. A Section 83(b) election generally must be filed within 30 days after the property is transferred. This deadline is unforgiving. If the election is missed, the intended tax benefit may be lost.

The IRS now provides Form 15620 for making a Section 83(b) election. The existence of the form does not make the decision automatic. It simply gives taxpayers a more standardized way to make the election.

The key point is that the 83(b) election is not a casual administrative step. It is often the hinge on which the early exercise strategy turns.

The 83(b) election is time-sensitive. Build the filing process into the decision before exercising, not after.

How the 83(b) Election Works With Early Exercised NSOs

The 83(b) election can be especially important for early exercised NSOs.

Assume an employee receives 100,000 NSOs with an exercise price of $1 per share. The current fair market value is also $1 per share. The employee early exercises the options and pays $100,000 for the shares. Because the shares are still subject to vesting, the employee files a timely 83(b) election.

At the time of exercise, the spread is zero. The employee has paid $1 per share for stock worth $1 per share. If the 83(b) election is valid and timely, there may be no ordinary income at exercise.

Now, assume the company grows, and the shares are worth $10 per share as they vest. Without an 83(b) election, the employee might recognize ordinary income as the shares vest based on the increased value. With the 83(b) election, the employee may avoid ordinary income taxation on the later-vesting appreciation. Future gain may instead be taxed as capital gain when the shares are eventually sold.

That can be a major tax benefit.

However, the risk is just as important. The employee paid $100,000 for private company shares. If the company fails, the employee may lose that cash. If the employee leaves before vesting, the company may repurchase unvested shares. If the stock remains illiquid for years, the employee may have wealth on paper but no ability to convert it into usable cash.

The tax savings may be real, but the cash risk is real too.

How the 83(b) Election Works With Early Exercised ISOs

The 83(b) election can also be relevant when ISOs are early exercised before vesting, but this area requires more nuance.

With ISOs, the spread at exercise may create an AMT adjustment. If the exercise price equals the fair market value at the time of early exercise, the AMT adjustment may be zero or small. That is one reason early exercise can be attractive for ISOs. It may allow the employee to exercise before the company’s valuation rises and before the AMT spread becomes painful.

For example, assume an employee receives 100,000 ISOs with a $1 exercise price. The current fair market value is also $1. The employee early exercises and files a timely 83(b) election. The exercise cost is $100,000, and the AMT spread may be zero because the exercise price and fair market value are the same.

If the company later increases in value, the employee has already exercised at the lower valuation. The employee may also be working toward the ISO holding periods, assuming all ISO rules are satisfied.

However, early exercising ISOs does not magically solve every tax problem. The employee still needs to evaluate AMT, holding periods, potential disqualifying dispositions, state tax rules, liquidity, and the risk that the shares never become valuable.

The 83(b) election may help with timing, but it does not guarantee a private company stock sale.

The AMT Trap With ISOs

The alternative minimum tax is one of the biggest reasons ISO planning must be modeled before exercise.

An employee may hear that ISOs are not taxed at exercise for regular federal income tax purposes. That statement can be technically true and still dangerously incomplete. If the employee exercises and holds the shares, the ISO spread may create an AMT adjustment.

This can create a strange and painful result. The employee may owe tax on economic income that has not been converted into cash. The shares may be private. There may be no public market. A tender offer may not be available. An IPO may be years away. The tax bill, however, may arrive now.

That is why early exercise can be attractive when the spread is small. If the fair market value is close to the exercise price, the AMT adjustment may be modest. If the employee waits until the company’s value rises sharply, the AMT adjustment may become substantial.

The key is not to guess. The employee should model regular tax, AMT, state tax, and future sale scenarios before exercising.

The Upside Case for Early Exercise

Early exercise can make sense when several favorable conditions line up.

It may be attractive when the exercise price and current fair market value are close together. This reduces the immediate taxable spread and may improve the tax outcome if the company later appreciates significantly.

It may also make sense when the employee has strong financial liquidity outside the company stock. The employee should be able to pay the cost of the exercise and any related taxes without disrupting emergency reserves, home purchase plans, family obligations, or other important financial goals.

Early exercise may be more reasonable when the employee has a high conviction in the company and expects to remain employed long enough for the shares to vest. The employee should also understand what happens if employment ends early.

The strategy is stronger when the potential tax savings are meaningful, the company allows early exercise, and the 83(b) election can be filed correctly within the 30-day deadline.

The strongest cases often involve early-stage employees whose exercise price is low, whose current 409A value is still modest, and whose exercise cost represents a manageable portion of their overall financial life.

In that scenario, early exercise may allow the employee to move future appreciation into a better tax posture while taking a calculated risk.

The Downside Case Against Early Exercise

Early exercise can be a poor decision when the employee cannot afford to incur the cost of the exercise.

This is the first and most important filter. If losing the exercise money would harm your financial life, early exercise may be too risky. Private company stock can become worthless. It can also remain illiquid for longer than expected.

Early exercise can also be problematic when the spread is already large. For NSOs, a large spread can create immediate ordinary income. For ISOs, a large spread can create a significant AMT adjustment. In both cases, the tax bill may be too large relative to the potential benefit.

The strategy may also be inappropriate when the employee is unsure whether to stay with the company. If the shares are still subject to vesting and the employee leaves early, the company may repurchase unvested shares. That may reduce the expected benefit of the strategy.

Early exercise can also create dangerous concentration. The employee may already depend on the company for salary, bonus, health benefits, career advancement, unvested equity, and future earning power. Adding a large personal cash investment into the same company can create a financial tower built on one foundation.

The tax benefits may look beautiful on a spreadsheet, but the spreadsheet needs to survive contact with real life.

If losing the exercise cost would meaningfully damage the employee’s financial life, the strategy may be too aggressive.

What If the Stock Goes to Zero?

When you hold an unexercised option, you have the right to buy shares. You do not have to exercise if the stock becomes worthless. The option may expire worthless, but you may not have committed additional cash.

When you exercise early, you change the equation. You have purchased the shares. Your cash is now at risk.

The company may fail. The company may raise money at a lower valuation. Your ownership may be diluted. Preferred shareholders may have liquidation preferences that leave common shareholders with less than expected. The company may be acquired at a price that sounds impressive in the news but does not produce a meaningful outcome for common stockholders.

This is why early exercise should not be framed as a tax hack. It is an investment decision.

The tax code may reward the right timing, but it does not reimburse for poor outcomes.

Early Exercise and Holding Periods

Holding periods are another reason early exercise can matter.

For NSOs, the holding period after exercise generally determines whether later appreciation is taxed as short-term or long-term capital gain when the shares are sold. If the shares are held for more than one year after exercise, post-exercise appreciation may qualify for long-term capital gain treatment.

For ISOs, the holding period rules are more specific. To receive favorable ISO treatment, the shares generally must be held for more than two years from the grant date and more than one year from the exercise date. Selling before those requirements are satisfied generally creates a disqualifying disposition.

Early exercise can help start the exercise date holding period sooner. That can be valuable if the company later has a liquidity event. However, holding periods do not override the need for tax modeling. A favorable holding period is useful only if the employee can manage the tax cost, liquidity risk, and company risk over time.

Early Exercise Before a Tender Offer, IPO, or Acquisition

Employees often begin thinking seriously about exercise when a liquidity event feels closer.

A company may be rumored to go public. A tender offer may be announced. A new funding round may be expected. The company may be discussing an acquisition. The 409A valuation may be about to increase. Suddenly, the option grant that sat quietly in the portal becomes urgent.

These moments require planning, not panic.

Before exercising, employees should understand whether the exercise will occur before or after a new valuation. They should know whether there is enough time to file an 83(b) election if the shares are unvested. They should evaluate whether the shares can actually be sold in the liquidity event. They should understand whether lockup rules may apply. They should calculate whether taxes can be paid without selling shares.

They should also consider whether a same-year exercise and sale may be better than exercising and holding, especially for ISOs, where AMT could be an issue.

The worst time to learn the tax rules is after the transaction window opens.

A Case Study Where Early Exercise Works Well

Assume an employee receives 100,000 NSOs with an exercise price of $1 per share. The company allows early exercise. The current fair market value is also $1 per share. The employee pays $100,000 to exercise and files a timely 83(b) election.

Because the exercise price equals the current fair market value, the taxable spread at exercise is zero. The employee has used cash, but the immediate income tax cost may be minimal.

Five years later, the company is acquired for $20 per share. The employee sells the shares for $2,000,000. The employee paid $100,000, so the economic gain is $1,900,000.

In this example, the early exercise strategy worked well because the employee exercised when the spread was low, filed the 83(b) election on time, had the liquidity to fund the exercise, stayed long enough for the shares to vest, and ultimately received a successful exit.

This is the version of the story that gets repeated in startup circles.

It is real, but it is not the only version.

A Case Study Where Early Exercise Backfires

Assume another employee early exercises 100,000 shares at $2 per share. The employee pays $200,000 and files a timely 83(b) election. At the time, the company appeared promising. Management is optimistic. Investors are excited. The employee believes the shares could eventually be worth far more.

Two years later, the company struggles to raise capital. The valuation falls. The business eventually shuts down, and the common shares become worthless.

The employee may have lost the $200,000 exercise cost. Any tax benefit may be limited, delayed, or far less useful than expected.

This is the version of the story that does not get as much airtime.

It is also real.

Early exercise can create an excellent tax outcome when the company succeeds. It can create a painful cash loss when the company fails.

A Case Study Involving ISO AMT Risk

Assume an employee holds 50,000 ISOs with a $5 exercise price. The current fair market value is $35 per share. The employee exercises and holds the shares.

The spread is $30 per share. The total spread is $1,500,000.

That spread may be included as an AMT adjustment. The employee may owe significant tax even though no shares were sold. If the stock later falls, the employee may have paid tax based on a value that no longer exists.

This is one of the classic ISO planning problems. It is not enough to know that ISOs can receive favorable tax treatment. The timing of exercise, sale, AMT exposure, and liquidity all need to be coordinated.

A Case Study Involving the ISO $100,000 Rule and an Early Exercise Provision

Assume an employee receives 400,000 options with an exercise price of $1 per share. The fair market value on the grant date is also $1 per share. The grant vests over four years, with 100,000 options vesting each year.

If the options are exercisable only as they vest, the grant may fit within the ISO $100,000 annual limitation. Each year, $100,000 of grant-date fair market value first becomes exercisable.

Now, let’s assume the agreement includes an early exercise provision that allows the employee to exercise all 400,000 options immediately. The employee may believe the four-year vesting schedule still controls the ISO analysis. However, because the entire option may be immediately exercisable, the full $400,000 of grant-date fair market value may be treated as first exercisable in the year of grant.

As a result, only $100,000 of the grant may qualify as ISOs. The remaining $300,000 may be treated as NSOs.

This can dramatically change the tax outcome. If the employee later exercises the entire grant at a fair market value of $10 per share, the ISO and NSO portions may be taxed differently. The ISO portion may create an AMT adjustment if the shares are held. The NSO portion may create ordinary compensation income at exercise.

This is why employees should not focus only on whether an early exercise feature exists. They should also understand how that feature interacts with the ISO $100,000 rule.

When Early Exercise May Make Sense

Early exercise may make sense when the spread between the exercise price and the fair market value is very small. It may also make sense when the exercise cost is affordable, the employee has strong liquidity, and the employee can tolerate the possibility that the shares may become worthless.

It may be a strong planning opportunity when the company is still early in its growth cycle, the employee expects to stay long enough for the shares to vest, and the potential future appreciation is meaningful.

The strategy may also make sense when the employee can file a timely 83(b) election and has carefully modeled the tax impact. With ISOs, this includes AMT modeling and analysis of the $100,000 ISO limitation. With NSOs, this includes ordinary income, payroll tax, withholding, and future capital gain planning.

Early exercise tends to work best when the employee is making a deliberate, informed decision rather than reacting to coworker chatter, IPO rumors, or fear of missing out.

When Early Exercise May Not Make Sense

Early exercise may not make sense when the exercise cost is too large relative to the employee’s net worth.

It may also be a poor fit when the company’s future is highly uncertain, the employee may leave soon, or the shares would represent too large a share of the employee’s financial life. If the employee already has a salary, career trajectory, bonus compensation, and unvested equity tied to the same company, adding a large out-of-pocket investment may create excessive concentration risk.

Early exercise may also be unattractive when the spread is already large. For NSOs, this may create a large ordinary income tax event. For ISOs, it may create a large AMT adjustment.

It may also be a mistake when the employee does not understand the 83(b) deadline. Missing the 30-day filing deadline can materially change the economics of the strategy.

Finally, early exercise may be problematic if an ISO grant has not been reviewed for compliance with the $100,000 rule. If part of the grant is treated as NSOs, the tax cost of exercise may be higher than the employee expects.

The central question is not whether early exercise could save taxes. The question is whether the potential tax savings justify the cash, tax, liquidity, and company risks.

The 83(b) Election Checklist

Before making an 83(b) election, an employee should confirm that the company allows early exercise and that the shares being acquired are subject to vesting or another substantial risk of forfeiture.

The employee should document the exercise date, the number of shares, the amount paid, the fair market value, and the type of equity involved. The employee should also confirm the correct filing procedure and retain copies of the filing with permanent tax records.

The election generally must be filed within 30 days after the property is transferred. That deadline should be treated as absolute. This is not a task to leave for the end of the month, the end of the quarter, or the next tax filing season.

An employee should also coordinate with a qualified tax advisor before filing. The election itself may look simple, but the decision behind it is not.

The Questions to Ask Before Early Exercising

Before early exercising stock options, you should know exactly what type of options you have. ISOs and NSOs are taxed differently, and the decision framework varies by option type.

You should know whether your company allows early exercise. You should know your exercise price, the current 409A value, the current spread, and the total cash required to exercise.

You should understand whether the exercise will create ordinary income, AMT exposure, payroll withholding, or state tax consequences. You should know whether you can file a timely 83(b) election and what happens if you miss the deadline.

If you have ISOs, you should ask whether the entire grant qualifies for ISO treatment or whether part of the grant is treated as NSOs because of the $100,000 rule. You should also ask whether the early exercise provision causes the entire grant to become first exercisable in the year of grant.

You should ask how your company tracks the ISO and NSO portions of the grant. You should ask whether the exercise platform will clearly identify the tax character of the shares being exercised. You should also ask how the company will report the exercise for tax purposes.

You should also ask whether you can afford to lose the full cost of the exercise. That question may feel harsh, but it is essential. Private company equity can produce life-changing gains, but it can also become worthless.

You should also ask how much of your net worth, income, and future career capital is already tied to the same company. A concentrated position may be exciting when the company is rising, but concentration can become suffocating when the story changes.

Finally, you should ask whether early exercise fits your broader financial plan. A good decision should not depend solely on the company’s best-case scenario.

The Early Exercise Decision Framework

Taxes matter, but they are only one variable. The strongest early exercise decisions balance tax efficiency with liquidity, risk, and long-term financial goals.

How VIP Wealth Advisors Thinks About Early Exercise Decisions

At VIP Wealth Advisors, we view early exercise as a multi-layered planning decision rather than a narrow tax question.

The first layer is tax modeling. This includes regular income tax, AMT, payroll tax, state tax, capital gains, and future sale scenarios. The goal is to understand the full tax picture before exercise, not after the tax bill arrives.

The second layer is equity classification. This includes reviewing whether the grant is entirely ISO, entirely NSO, or split between ISO and NSO treatment because of the $100,000 ISO rule. It also includes understanding whether an early exercise provision changes the first-exercisable analysis.

The third layer is liquidity planning. Exercising options requires cash. Taxes may require more cash. Private shares may not provide liquidity for years. The exercise decision should not put emergency reserves, family goals, home purchases, or lifestyle stability at risk.

The fourth layer is concentration risk. Employees at private companies often already have substantial exposure to their employer. Their salary, bonus, career path, unvested equity, and future opportunities may all depend on the same company. Exercising options adds another layer of exposure.

The fifth layer is exit scenario analysis. A thoughtful plan should consider an IPO, a tender offer, an acquisition, a delayed exit, a down round, or company failure. The right strategy should not rely only on the happiest version of the future.

The sixth layer is behavioral discipline. Equity compensation decisions are often made in emotionally charged environments. Coworkers talk. IPO rumors spread. Valuations rise. Fear of missing out takes over. A good planning process slows the decision down enough to make it rational.

The right stock option decision is rarely found inside the equity portal. It is found by integrating taxes, liquidity, risk, timing, grant language, and real-life priorities.

The best exercise decision is usually the one that still works if the future is slower, messier, or less profitable than expected.

Once the cash leaves your account, the decision becomes real.

The Moment the Option Stops Being Optional

Exercising stock options early can be a smart strategy when the conditions are right. It can reduce future ordinary income, start holding periods sooner, manage ISO AMT exposure, and position future appreciation for better tax treatment.

It can also be a costly mistake. Early exercise can require substantial cash, create tax exposure before liquidity, increase concentration risk, and leave the employee holding private shares that may decline in value or never become liquid.

For employees with ISOs, there is another key issue. The grant may be subject to the $100,000 ISO limitation. If the grant is too large or the early exercise feature is not carefully drafted, part of the grant may be treated as NSOs. That can meaningfully change the tax result.

The decision should never be made from excitement alone. It should also never be made from fear alone.

The right question is not, “Can I early exercise?”

The right question is, “Should I early exercise based on my option type, ISO/NSO classification, tax exposure, liquidity, company risk, and personal financial plan?”

That question deserves careful modeling before the exercise is made, because once the cash leaves your account, the decision becomes real.

Frequently Asked Questions About Early Exercising Stock Options

What does it mean to early-exercise stock options?

Early exercise means exercising stock options before they are vested, if the company’s equity plan allows it. The employee buys the shares now, but unvested shares may still be subject to a company repurchase right if the employee leaves before they vest.

Why would someone exercise stock options early?

Someone may exercise stock options early to reduce the taxable spread, start the capital gains holding period sooner, manage AMT exposure, and potentially shift future appreciation into capital gains treatment.

Is early exercise available for every stock option grant?

No. Early exercise is available only if the company’s equity plan and option agreement permit it. Many companies do not allow employees to exercise options before they vest.

What is an 83(b) election?

An 83(b) election allows a taxpayer to include the value of property in income when the property is transferred rather than when it vests. For early exercised stock options, it can be important because the shares may still be subject to vesting.

How long do I have to file an 83(b) election?

An 83(b) election generally must be filed within 30 days after the property is transferred. Missing the deadline can materially change the tax outcome.

Does an 83(b) election apply to NSOs?

Yes. An 83(b) election can be especially important for early-exercised NSOs because it may prevent future appreciation from being taxed as ordinary income when the shares vest.

Does an 83(b) election apply to ISOs?

An 83(b) election may be relevant when ISOs are exercised early before vesting, but ISO and AMT rules still need to be modeled carefully.

Can early exercising ISOs trigger AMT?

Yes. Exercising ISOs and holding the shares can create an AMT adjustment based on the spread between the exercise price and the fair market value at exercise.

What is the ISO $100,000 rule?

The ISO $100,000 rule limits the amount of stock that can first become exercisable as ISOs in any calendar year. The limit is based on the grant-date fair market value of the shares. If the amount first exercisable in a year exceeds $100,000, the excess is generally treated as NSOs.

What is an ISO/NSO split?

An ISO/NSO split occurs when part of a stock option grant qualifies for ISO treatment, and another part is treated as NSOs. This often happens because of the ISO $100,000 annual limitation.

Can an early exercise provision affect ISO treatment?

Yes. If an early exercise provision allows the entire option grant to be exercised immediately, the entire grant may be considered first exercisable in the year of grant for purposes of the ISO $100,000 rule. This can cause part of the grant to be treated as NSOs.

Can grant language help prevent an early exercise feature from creating unintended ISO/NSO treatment?

Careful grant language may help by limiting early exercisability so that no more than $100,000 of grant-date fair market value first becomes exercisable as ISOs in any calendar year. The agreement may also state that any excess portion will be treated as NSOs. This language should be drafted by qualified equity compensation counsel.

Is early exercise always a good idea?

No. Early exercise can create tax benefits, but it also creates cash risk, liquidity risk, company risk, and concentration risk.

What is the biggest risk of early exercising stock options?

The biggest risk is using real cash to buy private company shares that may decline in value, remain illiquid, or become worthless.

Should I early exercise before an IPO?

Early exercise before an IPO may be beneficial in some cases, but it depends on the option type, exercise price, fair market value, tax exposure, lockup rules, liquidity needs, and expected sale strategy.

What happens if I early exercise and leave the company?

If shares are unvested when you leave, the company may have the right to repurchase those shares. The exact treatment depends on the company’s equity plan and option agreement.

How do I know if early exercise makes sense?

Early exercise should be evaluated through tax projections, AMT modeling, ISO/NSO classification review, liquidity planning, company risk analysis, and concentration risk review. It should fit into a broader financial plan rather than being made as a standalone tax decision.

Before You Early Exercise, Model the Decision

Early exercise can be powerful, but only when the tax benefit, cash cost, ISO/NSO treatment, AMT exposure, 83(b) timing, and company risk all make sense together.

VIP Wealth Advisors helps employees evaluate equity compensation decisions before they become expensive, irreversible choices.