Every year, millions of dollars quietly change hands between family members, friends, and even business associates. While most people think of taxes as something you deal with only when you earn income, Uncle Sam also pays attention when you give it away. That’s where the federal gift tax comes in.

In 2025, the rules for gift taxes are clearer than ever but still full of nuance. The annual exclusion has ticked upward, the lifetime exemption remains sky-high (for now), and special planning opportunities continue to make gifting one of the most powerful estate and tax strategies available to high-net-worth families.

This guide breaks down how the federal gift tax works in 2025, the key numbers to know, and the planning strategies that can help you transfer wealth while minimizing taxes.

1. What Is the Gift Tax?

The federal gift tax is part of the broader “transfer tax” system, which also includes the estate tax and the generation-skipping transfer (GST) tax. Its purpose is simple: to prevent wealthy individuals from dodging the estate tax by giving away all of their property during their lives.

The tax applies to transfers of property for less than full value. That means cash, real estate, securities, business interests, or even the right to use or receive income from property can all be considered taxable gifts if they aren’t exchanged for something of equal value.

Two crucial points set the stage:

- The donor (the person making the gift) is the one responsible for the gift tax.

- The recipient (the donee) never pays gift tax and does not include the gift in income.

So while you might give your niece $200,000 to buy her first house, the IRS looks to you, not her, when asking whether tax is due.

2. What Counts as a Gift?

At its core, a gift is any transfer for less than full consideration. That could mean handing over cash, selling property at a bargain price, or forgiving a loan without repayment. Even “interest-free” loans can be treated as gifts if the foregone interest exceeds certain thresholds.

But not every transfer is taxable. Exemptions include:

- Transfers to a U.S. citizen spouse (unlimited marital deduction).

- Tuition or medical payments made directly to providers (a powerful tool for grandparents funding education or healthcare).

- Gifts to political organizations.

- Gifts to qualified charities.

These carve-outs create opportunities for strategic planning, particularly when combined with the annual exclusion.

3. The 2025 Annual Gift Tax Exclusion

For 2025, the annual exclusion is $19,000 per recipient. This is one of the simplest and most effective tools in wealth transfer planning.

You can give $19,000 to as many individuals as you like: your children, grandchildren, friends, even neighbors, without triggering gift tax or the need to file a return.

If you’re married, you and your spouse can “gift split,” effectively doubling this to $38,000 per recipient. For a couple with three children, that’s $114,000 per year transferred completely tax-free, with no impact on the lifetime exemption.

The key is that gifts must be of present interest, meaning the recipient can use and enjoy the gift immediately. Transfers to trusts or future rights to property often don’t qualify.

4. Gift Splitting for Married Couples

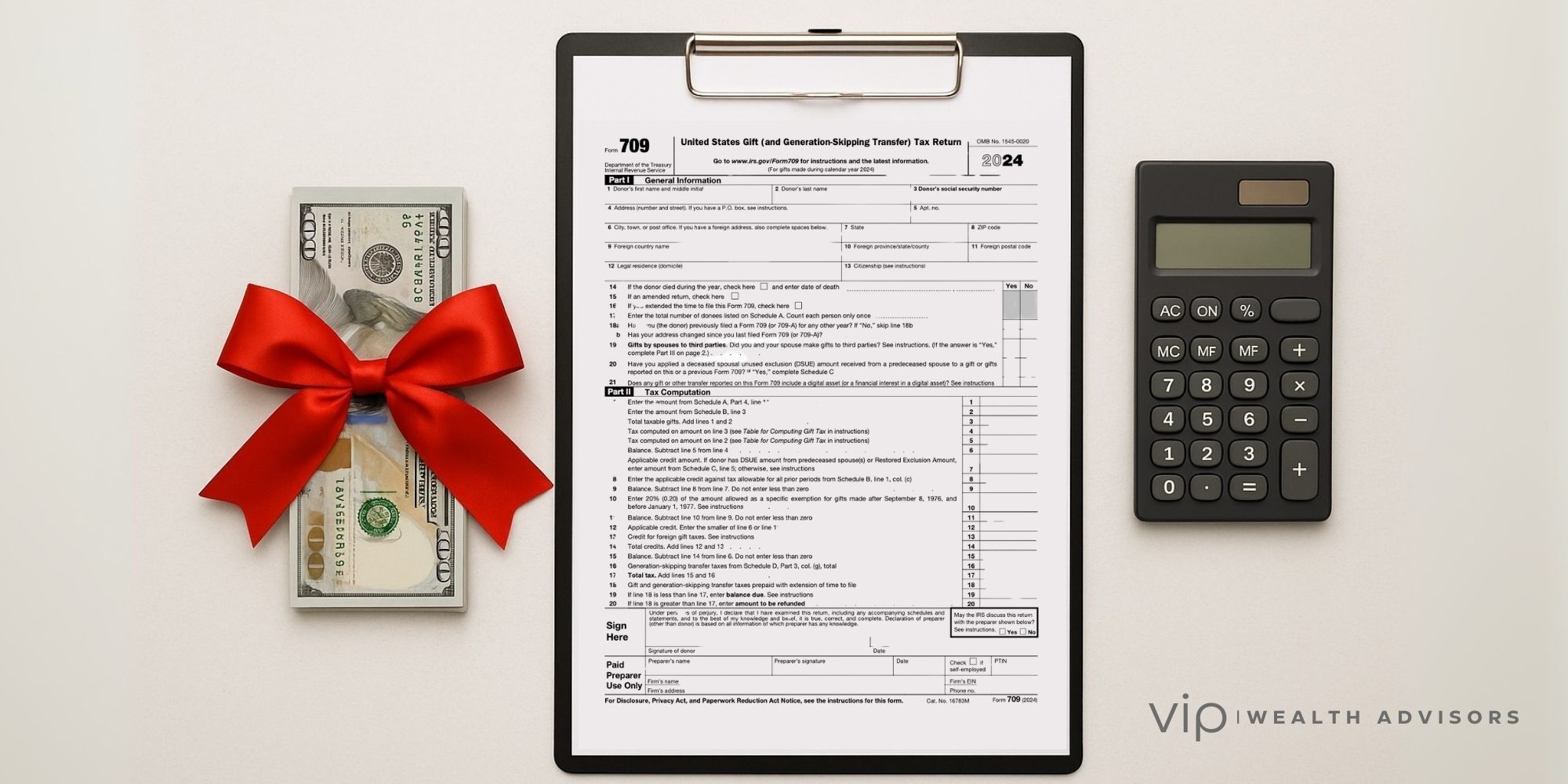

Gift splitting allows a couple to maximize exclusions, but it comes with paperwork. Both spouses must consent, and a gift tax return (Form 709) must be filed even if no tax is owed.

Example:

A father gives his daughter $30,000 in 2025. If he files alone, $19,000 is covered by the exclusion and $11,000 chips into his lifetime exemption. But if he and his wife elect gift splitting, it is treated as two $15,000 gifts, both within the exclusion, and no exemption is used.

This strategy is beneficial for families funding education, helping children buy homes, or transferring business interests.

5. The Lifetime Gift Tax Exemption in 2025

In addition to the annual exclusion, the IRS provides a massive lifetime exemption, also known as the unified credit. In 2025, that figure is $13,990,000 per person.

This exemption is “unified” with the estate tax exemption, meaning every dollar of taxable gifts you make during life reduces the amount you can shield from estate tax at death.

So, if you’ve already given away $5 million in taxable gifts during life, only $8.99 million of your estate will be protected by the exemption when you pass.

Important legislative note: Under the One Big Beautiful Bill Act (OBBBA), the lifetime exemption is scheduled to increase to $15 million starting in 2026, with inflation indexing beginning in 2027. However, political winds could shift, and many advisors warn clients to plan for the possibility of lower exemptions if Congress revisits estate tax rules.

6. Special Rules for Gifts to Non-Citizen Spouses

While gifts to a U.S. citizen spouse are unlimited, gifts to a non-citizen spouse face a cap. In 2025, the annual exclusion for gifts to a non-citizen spouse is $190,000.

This rule prevents wealthy individuals from sidestepping the estate tax entirely by gifting unlimited wealth to spouses abroad. Couples in cross-border marriages should plan carefully around this restriction.

7. When Must You File a Gift Tax Return?

Not every gift requires paperwork. But you must file Form 709 if you:

- Give any individual more than $19,000 in 2025.

- Elect gift splitting with a spouse.

- Make gifts of future interests (e.g., into certain trusts).

- Gift more than $190,000 to a non-citizen spouse.

Form 709 is due April 15 of the following year, with extensions available if you extend your income tax return.

Filing Triggers Summary

| Situation | What You Must Do |

|---|---|

| Give any individual more than $19,000 in 2025 | File Form 709 |

| Elect gift splitting with a spouse | Both spouses consent; file Form 709 |

| Make gifts of future interests | File Form 709 |

| Gift more than $190,000 to a non-citizen spouse | File Form 709 |

| Due date | April 15 of the following year (extensions available with income tax extension) |

8. How the Gift Tax Is Calculated

Gift tax isn’t applied piecemeal each year; it’s cumulative. That means the IRS tracks your total taxable gifts since 1976.

Here’s how it works:

- Add taxable gifts from the current year to all prior years.

- Calculate the tentative tax on the total.

- Subtract the unified credit (lifetime exemption) already used.

- The remainder, if any, is gift tax due.

Example:

Suppose you give your son $1,019,000 in 2025. $19,000 is excluded. The remaining $1,000,000 reduces your lifetime exemption, leaving $12,990,000. No gift tax is owed now, but your estate exemption at death is smaller.

9. Special Exclusions Worth Knowing

Education and Medical Transfers: Pay tuition or medical bills directly, and they are excluded from gift tax. Writing checks directly to universities or hospitals can transfer large amounts outside the system entirely.

Charitable Gifts: 100% deductible against gift tax.

Political Organizations: Gifts to political groups are excluded.

These carve-outs are frequently used by families funding education for grandchildren or covering medical expenses for aging parents.

10. The Generation-Skipping Transfer (GST) Tax

When wealth skips a generation—say, a grandparent gifts directly to a grandchild—the IRS imposes a separate GST tax. In 2025, the GST exemption matches the gift and estate exemption at $13,990,000.

High-net-worth families often use dynasty trusts to maximize GST planning, ensuring wealth compounds for multiple generations without estate tax erosion.

11. Gift Tax Rates

Gift tax rates mirror estate tax rates, topping out at 40% on transfers above the exemption.

This flat top rate is why strategic gifting before thresholds are reached can dramatically improve long-term wealth transfer outcomes.

12. Basis of Gifted Property

Unlike inheritances, which receive a step-up in basis at death, gifted property carries over the donor’s basis.

Example: If you give your daughter stock you bought for $50,000 that’s now worth $500,000, she takes your $50,000 basis. If she sells immediately, she owes capital gains tax on $450,000.

This rule means gifting highly appreciated assets can backfire if the recipient plans to sell quickly. Sometimes it’s more efficient to hold assets until death to lock in a step-up in basis.

13. State Gift Taxes

Most states do not impose a gift tax, but a few have estate or inheritance taxes that complicate planning. Families with multi-state property holdings should consult local rules.

14. Penalties and Compliance

Failing to file Form 709 when required can trigger penalties, interest, and headaches during IRS audits. Undervaluing gifts of property (like business interests) can also lead to disputes. Professional appraisals are critical for non-cash transfers.

15. Planning Considerations for 2025

✅ Gift Splitting: Married couples can double exclusions, but paperwork is key.

✅ Coordinate with Estate Planning: Remember that gifts reduce your estate exemption. Work with professionals to balance lifetime giving and legacy planning.

✅ Leverage Tuition and Medical Transfers: Direct payments to schools or hospitals bypass the system entirely.

✅ Be Strategic With Appreciated Assets: Sometimes it’s smarter to hold until death to secure a step-up basis.

Conclusion

The federal gift tax in 2025 is both a guardrail and an opportunity. While its purpose is to limit tax-free transfers, the generous annual exclusion and lifetime exemption create powerful ways for families to move wealth without immediate tax.

For those with large estates, gifting can be an essential tool in reducing future estate tax liability. For others, it’s a way to see the impact of generosity during life rather than leaving everything to be settled after death.

Key 2025 Numbers at a Glance:

| Item | 2025 Amount / Rate |

|---|---|

| Annual exclusion | $19,000 per recipient |

| Lifetime exemption | $13,990,000 (rising to $15,000,000 after 2025) |

| Notable exclusion for gifts to non-citizen spouses | $190,000 |

| Top gift tax rate | 40% |

With exemptions at historic highs, 2025 may be one of the most favorable years in history for strategic wealth transfer. The question is whether you’ll use these opportunities—or let them pass by.

Common Form 709 Triggers and When You Do Not Need to File

Here are the most common triggers for filing Form 709:

Gifts over the annual exclusion

In 2025, that’s $19,000 per recipient.

Example: You give your son $50,000 for a down payment. The first $19,000 is excluded, but the remaining $31,000 is a taxable gift. No tax is due if you apply it against your lifetime exemption, but you must report it on Form 709.

Gift-splitting with a spouse

Even if each spouse’s "share" of the gift is below $19,000, if you elect to split gifts, both spouses must file Form 709 to document the split.

Example: You write your daughter a $30,000 check, but you and your spouse elect to treat it as two $15,000 gifts. That’s within the exclusion, but both spouses must file 709s to elect the split.

Gifts of future interests

The annual exclusion only applies to "present interest" gifts (the recipient can use it right away). If you transfer money into certain trusts or give someone the right to receive income or property in the future, you have to file Form 709—no matter the amount.

Gifts to a non-citizen spouse

You can give up to $190,000 in 2025 to a non-U.S.-citizen spouse tax-free. Go over that amount, and you must file Form 709 to report it.

Indirect or unusual gifts

Forgiving a loan, selling something for less than fair market value, or giving an interest-free loan often counts as a gift. Those situations frequently trigger a filing requirement.

When you don’t need to file Form 709:

- Gifts under $19,000 per recipient (present interest only).

- Direct payments of tuition or medical expenses to schools or providers (these are excluded entirely).

- Gifts to a U.S. citizen spouse (unlimited marital deduction).

- Gifts to charities (deductible and not subject to gift tax).

🔎 Want a 2025 Gifting Plan That Minimizes Taxes?

At VIP Wealth Advisors, we design wealth transfer strategies that coordinate annual exclusions, lifetime exemption usage, GST planning, and state residency rules—so more of your capital reaches the people and causes you care about.

Get a customized roadmap for gifts, trusts, and timing—before year-end deadlines sneak up.

📅 Book Your VIP Planning CallView More Articles by Topic

- Taxes (93)

- Financial Planning (61)

- Equity Compensation (46)

- Investments (35)

- RSU (25)

- Tax Policy & Legislation (20)

- Incentive Stock Options (19)

- Retirement (19)

- Business Owner Planning (18)

- Psychology of Money (18)

- Alternative Investments (15)

- Pre-IPO Planning (12)

- Real Estate (11)

- Estate Planning (10)

- AMT (9)

- Fiduciary Standard (8)

- Capital Gains Tax (7)

- Private Investments (7)

- The Boring Investment Strategy (7)

- Crypto (6)

- NSOs (6)

- QSBS (5)

- 401(k) Strategy (4)

- Market Insights (4)

- Market Timing (4)

- Post-IPO Tax Strategy (4)

- Venture Capital (4)

- International Financial Strategies (3)

- Legacy Wealth (3)

- Q&A (3)

- Stock Market (3)

- Altruist (2)

- Charitable Giving (2)

- ETF Taxes (2)

- Education Planning (2)

- IRA Strategy (2)

- Irrevocable Trust (2)

- Risk Management (2)

- Video (2)

- AUM vs Flat Fee (1)

- Atlanta (1)

- Book Review (1)

- Carried Interest Planning (1)

- Depreciation & Deductions (1)

- Energy Markets (1)

- Exit Planning (1)

- Geopolitics (1)

- Precious Metals (1)

- QTIP Trust (1)

- Revocable Trust (1)

- Schwab (1)

- Solo 401k (1)

- metals (1)