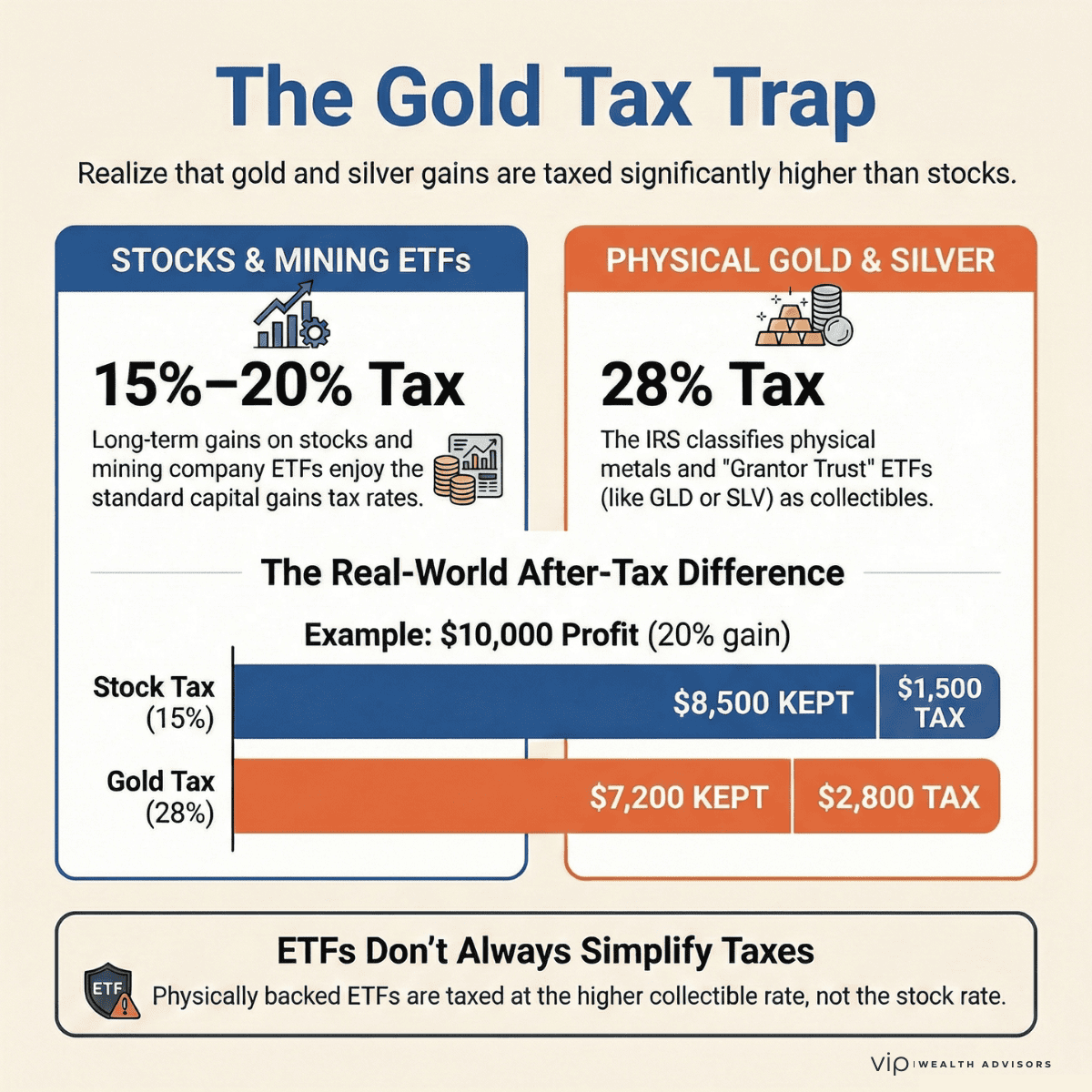

Gold and silver investments are typically taxed as collectibles at rates up to 28%, which can significantly reduce after-tax returns compared to traditional equities.

Key Takeaways Before You Buy or Sell

- Most gold and silver gains are taxed at up to 28%

- Many popular gold ETFs are taxed like physical metal

- Jewelry gains are taxable, losses are not deductible

- Mining stocks and mining ETFs have different tax treatment

- After-tax returns matter more than headline prices

- Behavior and timing often matter more than theory

Gold and silver are back in the headlines. Prices have surged, volatility has spiked, and investor interest has followed. From physically backed gold ETFs to Costco selling gold bars, precious metals are suddenly everywhere again.

But here's the problem: most investors have no idea how gold and silver are actually taxed.

They assume gains are treated like stocks. They're not.

They assume ETFs simplify things. Often, they don't.

They assume a strong rally equals a strong after-tax return. That's where many get burned.

If you're thinking about investing in gold or silver, or already own it, understanding the tax rules is not optional. It's the difference between a smart hedge and an expensive mistake.

This article breaks down how precious metals are taxed in plain English, why so many investors are caught off guard, and how to think about gold and silver inside a modern wealth plan.

Why Gold and Silver Are Treated Differently by the IRS

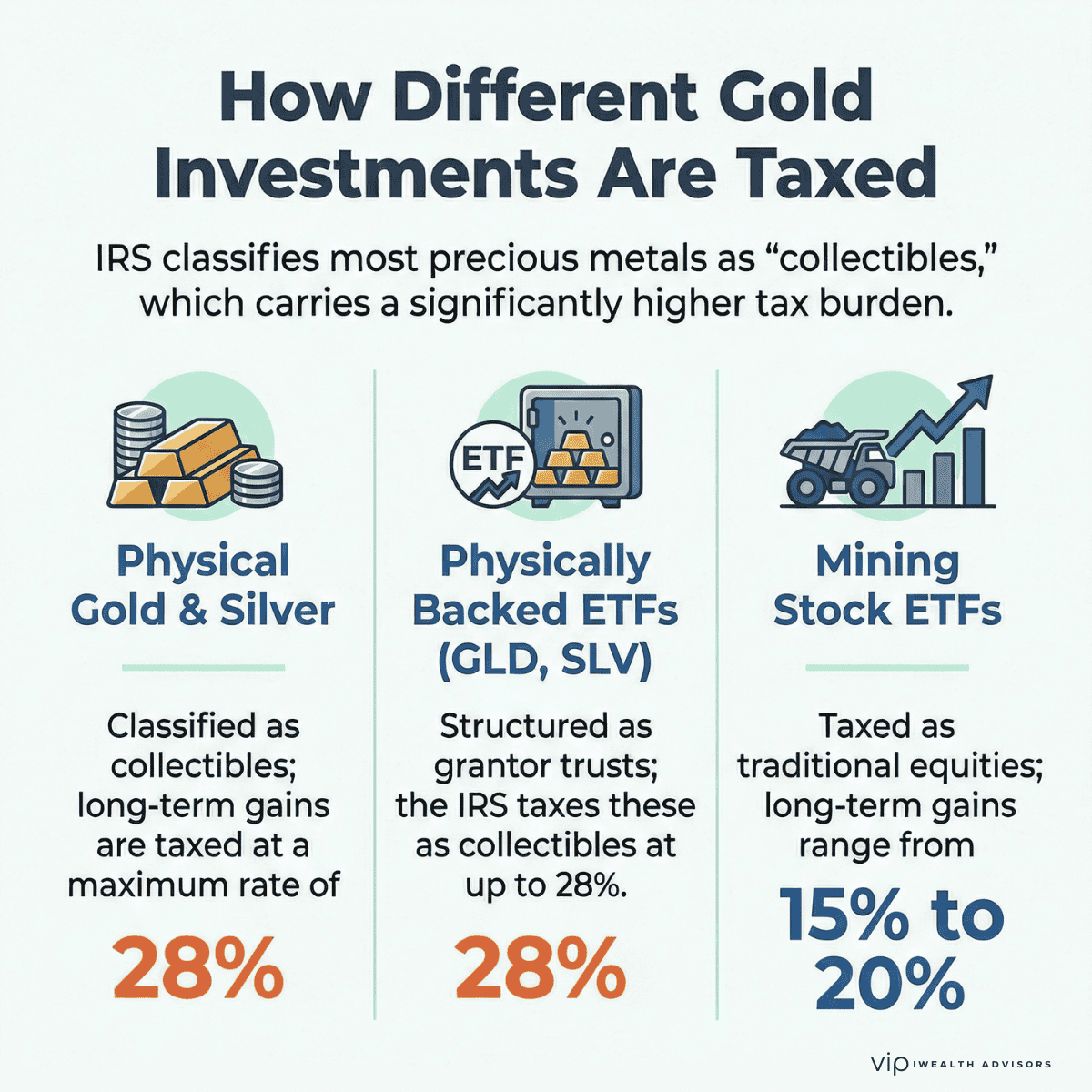

Under the U.S. tax code, most precious metals are classified as collectibles, not traditional investments.

That distinction matters.

The Collectibles Rule

Under IRC Section 408(m), collectibles include:

- Metals and gems

- Coins and bullion

- Jewelry made from precious metals

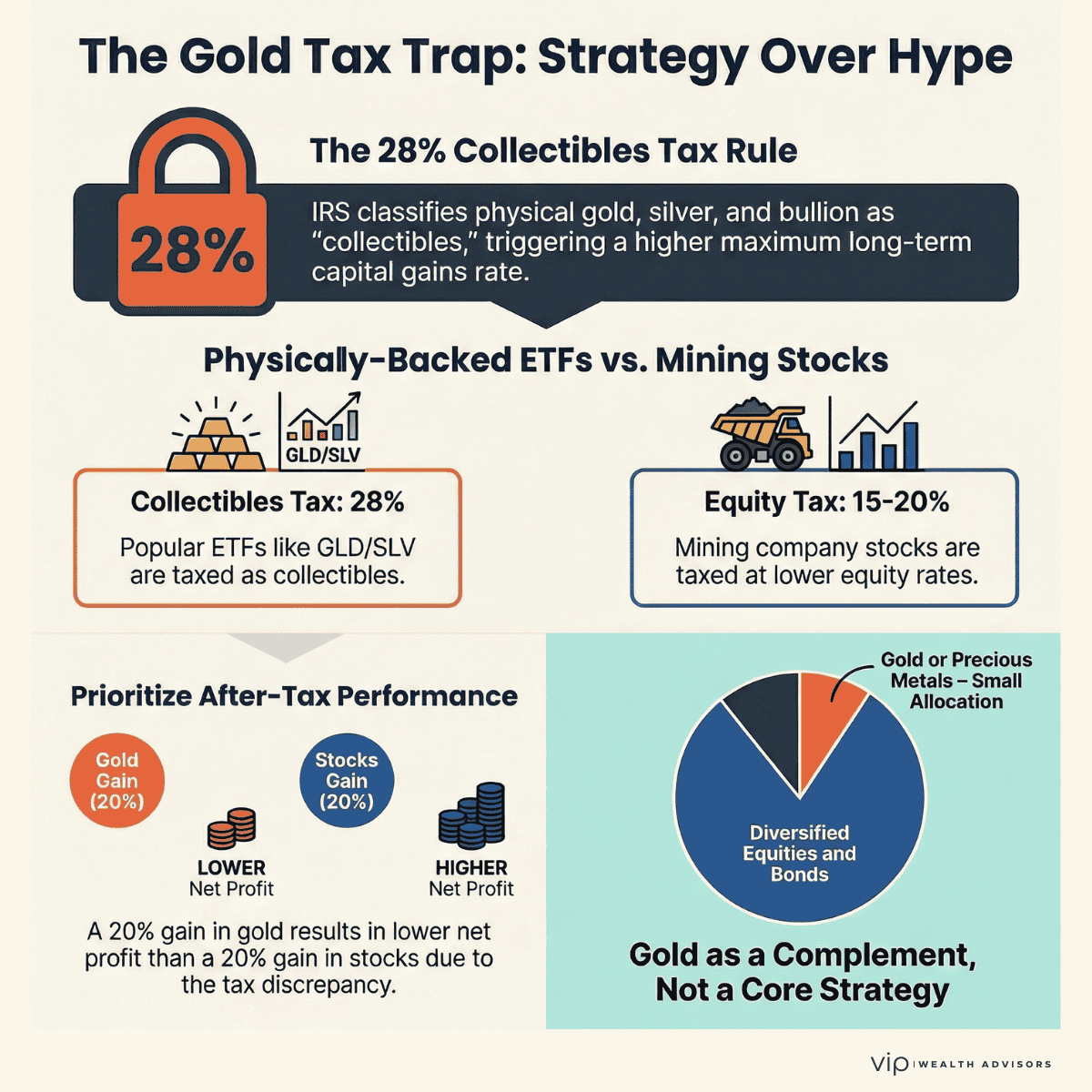

If an asset is considered a collectible and held longer than one year, long-term gains are taxed at a maximum federal rate of 28%, not the standard 15% or 20% long-term capital gains rate that applies to stocks and ETFs.

Short-term gains are taxed as ordinary income, just like stocks.

This single rule is responsible for most of the confusion and disappointment investors experience with gold and silver.

How Physical Gold and Silver Are Taxed

Buying Physical Gold or Silver

There is no tax when you buy gold or silver bars, coins, or bullion.

Sales tax may apply depending on your state, but there is no federal tax at the time of purchase.

Selling Physical Gold or Silver

When you sell:

- Your gain equals the sale price minus your cost basis

- If held more than one year, gains are taxed at up to 28%

- If held one year or less, gains are taxed as ordinary income

This applies to:

- Gold bars

- Silver bars

- Bullion coins

- Collectible coins

- Jewelry containing precious metals

If you sell jewelry at a loss, the loss is not deductible. Jewelry is considered personal-use property. That means you get taxed on gains, but you do not get tax relief on losses.

Gold and Silver ETFs: Where Many Investors Get It Wrong

A common assumption is that ETFs make taxation simpler.

With precious metals, that's often false.

Physically Backed ETFs (GLD, SLV, etc.)

Many popular gold and silver ETFs are structured as grantor trusts that hold physical metal.

For tax purposes, the IRS treats you as if you personally own a slice of that metal.

- Gains are taxed as collectibles

- Long-term rate up to 28%

- Short-term gains taxed as ordinary income

This has been confirmed by IRS guidance and technical assistance memoranda.

In other words, buying gold through an ETF does not avoid the collectibles tax.

Mining Stock ETFs and Mutual Funds

These are different.

If a fund owns:

- Gold mining companies

- Silver mining stocks

- Precious metals producers

Then gains are taxed like normal equities.

That means:

- 15% or 20% long-term capital gains rates

- Losses are deductible

- Normal tax treatment

This distinction matters enormously when building a portfolio.

Precious Metals Inside IRAs: Allowed, But Narrowly

Most investors assume gold and silver are not allowed in IRAs.

That's mostly true, with limited exceptions.

What Is Not Allowed

If an IRA purchases a collectible that doesn't qualify for an exception:

- The amount is treated as a distribution

- Income tax applies

- A 10% penalty may apply if under age 59.5

What Is Allowed

Certain coins and bullion are permitted only if:

- They meet minimum fineness standards

- They are held by a qualified trustee or custodian

- You do not personally possess the metal

Even then, gains inside the IRA are deferred, but distributions are taxed as ordinary income.

The tax benefit comes from deferral, not from avoiding the collectibles rate.

Reporting and Paperwork: What Investors Miss

When selling precious metals:

- Gains are reported on Form 8949 and Schedule D

- Dealers may issue Form 1099-B depending on the quantity and type sold

- Accurate cost basis documentation is critical

For inherited metals, a step-up in basis may apply, significantly reducing taxable gains.

This is another area where professional guidance matters.

Why Gold's After-Tax Return Often Disappoints

Gold is frequently marketed as:

- An inflation hedge

- A crisis hedge

- A portfolio diversifier

Those claims may or may not hold depending on the period.

What is often ignored is after-tax performance.

A 20% gain in gold taxed at 28% is not the same as a 20% gain in equities taxed at 15%.

Taxes matter, especially over long holding periods.

Gold as Behavior, Not Just an Asset

In practice, gold often reveals more about investor psychology than portfolio construction.

We see investors buy gold:

- After large rallies

- During periods of fear

- As a reaction to headlines, not planning

That timing risk compounds the tax inefficiency.

Gold can play a role, but it should be sized appropriately and understood clearly.

How We Think About Gold and Silver at VIP Wealth Advisors

We do not view precious metals as core growth assets.

When used, they are:

- A small allocation

- Part of a broader diversification strategy

- Evaluated on an after-tax basis

- Integrated into a comprehensive financial plan

The biggest mistake is treating gold as a standalone decision rather than part of a coordinated strategy.

Why Taxes and Structure Matter More Than Headlines

Gold and silver are emotional assets wrapped in financial clothing.

They can protect, but they can also mislead. Before buying into the hype, make sure you understand not just the price chart, but the tax bill waiting on the other side.

If you're considering precious metals, or already hold them, this is a conversation worth having before the trade, not after the sale.

Frequently Asked Questions (Q&A)

Is gold taxed higher than stocks?

Yes. Most gold investments are taxed as collectibles with a maximum long-term rate of 28%, compared to 15% or 20% for stocks.

Are gold ETFs taxed differently?

Some are. Physically backed ETFs are taxed like collectibles. Mining stock ETFs are taxed like equities.

Is there a way to avoid the collectibles tax?

Not for physical metals or grantor-trust ETFs in taxable accounts. Holding qualifying metals inside an IRA defers tax, but distributions are taxed as ordinary income.

Are silver gains taxed the same as gold?

Yes. Silver is also considered a collectible.

What about selling inherited gold or jewelry?

Inherited assets generally receive a step-up in basis, which can reduce taxable gains significantly.

Should gold be in a retirement portfolio?

It can be, but usually in moderation and with full awareness of liquidity, volatility, and tax treatment.

Is gold a good inflation hedge?

Sometimes, over certain periods. But it is volatile, produces no income, and is tax-inefficient compared to other inflation-sensitive assets.

What's the biggest mistake investors make with gold?

Ignoring taxes and chasing headlines.

Before You Buy or Sell Gold, Know the Tax Consequences

Precious metals can play a role in a portfolio, but only when properly structured and evaluated on an after-tax basis.

If you already own gold or are considering an allocation, let's make sure it fits within your broader wealth plan.