Primary residences often create wealth through forced savings and leverage, not exceptional investment returns. A home should support a broader financial strategy, not replace disciplined investing.

Key Takeaways

- Homeownership built wealth through behavior. The biggest driver was consistent mortgage payments over long holding periods.

- Home appreciation is modest. U.S. single-family homes have historically returned about 3–5% per year, or roughly 0–2% after inflation.

- Leverage magnifies housing outcomes. Borrowing amplifies gains in rising markets and losses during downturns.

- A primary residence provides utility. Homeowners benefit from stability and avoided rent, known as "imputed rent."

- REITs represent real estate as an investment. They offer diversified exposure to income-producing property markets.

- Your home should support your wealth plan. Long-term wealth is primarily built through investing, tax strategy, and disciplined saving.

For generations, Americans have been taught a simple financial truth:

Buy a home. Build wealth. Everything else will take care of itself.

It's advice passed down by parents, reinforced by policymakers, echoed by lenders, and rarely questioned. For many families, it even felt true. They bought a home, stayed put for decades, paid off the mortgage, and retired with meaningful net worth.

But here's the question today's high-income professionals are quietly asking:

Was homeownership actually a great wealth-building strategy, or was it the only one most people consistently stuck with?

The answer matters. Especially for executives, founders, and business owners navigating a far more complex financial landscape than prior generations ever faced.

This article unpacks:

- Why homeownership did create wealth for many Americans

- Why that story is often misunderstood

- What homes actually return over time

- How real estate truly shows up as an investable asset class

- And how a primary residence should be framed inside a modern, high-income financial plan

Not to tear down the myth, but to replace it with something more accurate and useful.

Why Homeownership Became the Cornerstone of American Wealth

Historically, buying a home worked because several powerful tailwinds aligned at once.

The 20th-Century Housing Advantage

For much of the post–World War II era, homeownership benefited from:

- Strong wage growth relative to home prices

- Broad access to long-term fixed-rate mortgages

- Government-backed lending programs (FHA, VA, GSEs)

- High inflation that quietly reduced the real value of mortgage debt

- Favorable tax treatment on mortgage interest and capital gains

- Cultural norms that encouraged staying put and paying down debt

In that environment, buying a home served as a powerful financial force.

You didn't need to be a disciplined investor.

You just needed to keep making the payment.

Over time, this created equity, stability, and net worth.

The Crucial Distinction People Miss

Here's the nuance that often gets lost:

Homes didn't build wealth because they were exceptional investments. They built wealth by enforcing consistent behavior over long periods of time.

That difference matters.

Most households:

- Didn't invest regularly in markets

- Didn't rebalance portfolios

- Didn't optimize tax strategy

- Didn't save aggressively outside their home

The house “won” because it was the only asset demanding attention every month.

What the Data Actually Says About Home Returns

When stripped of leverage and emotion, the long-term numbers are surprisingly modest.

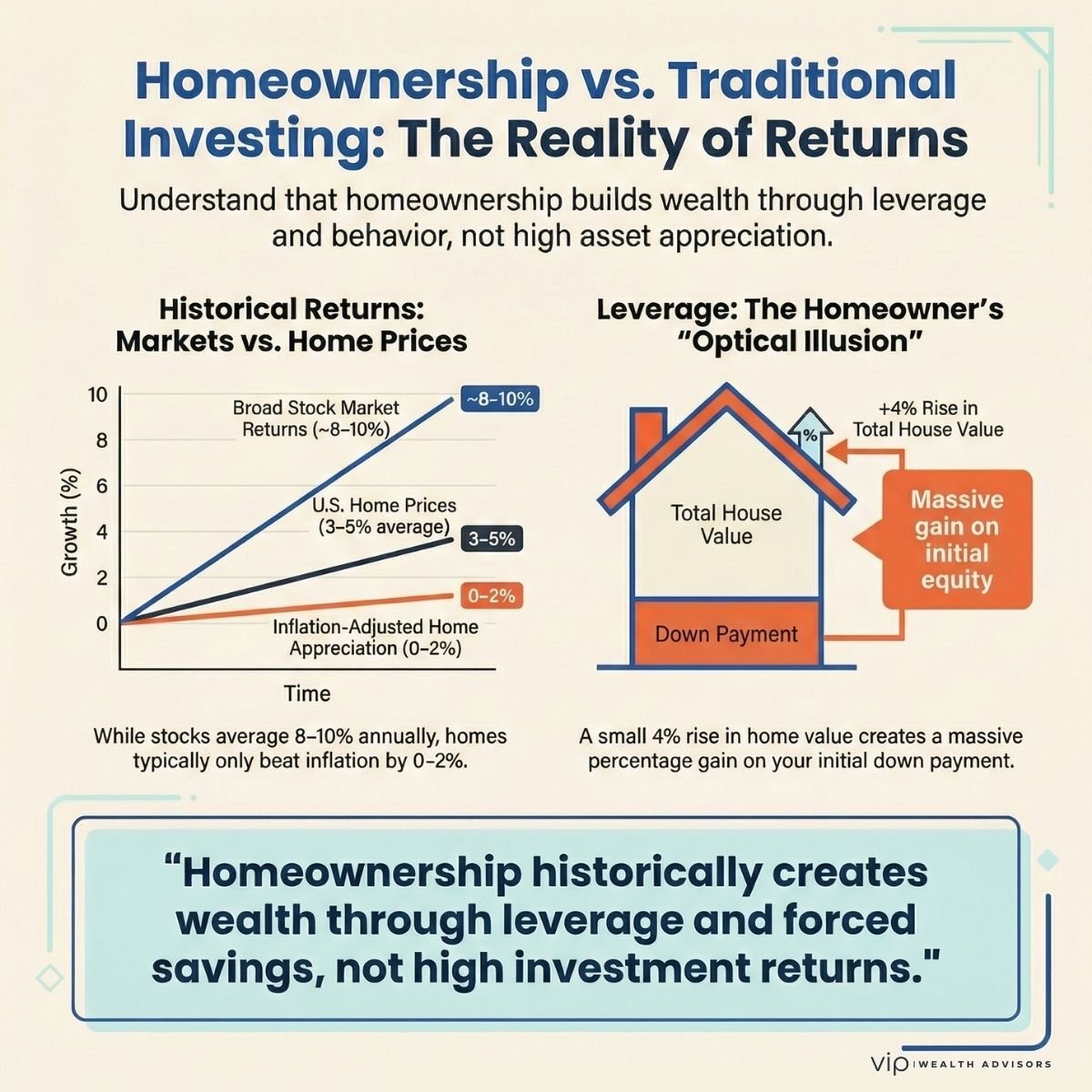

Infographic comparing homeownership and stock market returns, showing leverage benefits in real estate despite historically lower home price appreciation.

Single-Family Home Appreciation

Historically in the U.S.:

- Nominal appreciation: ~3–5% annually

- Inflation-adjusted (real) appreciation: ~0–2% annually

Over long periods, home prices tend to track inflation with a small real premium driven by land scarcity, zoning constraints, and local economics.

This doesn't mean homes are bad assets. It means they are slow, steady, inflation-sensitive assets, not growth engines.

Leverage: The Optical Illusion That Fuels the Myth

Homes feel like extraordinary investments because they are:

- Highly leveraged

- Purchased early in adulthood

- Held for decades

A 4% appreciation rate on a leveraged asset can look like spectacular equity growth, particularly during housing booms.

Leverage doesn't create return. It magnifies outcomes.

It works beautifully on the way up.

It's punishing on the way down.

The Overlooked Benefit: Living in the Asset

Now we arrive at what spreadsheets rarely capture.

A primary residence delivers something few assets can:

Daily utility.

Economists call this imputed rent.

Even though no rent check changes hands, the homeowner is effectively:

- Consuming housing services

- Avoiding market rent

- While participating in long-term appreciation

That avoided rent is a real economic benefit, even if it never appears on a statement.

This is why a home can simultaneously be:

- A mediocre standalone investment

- And a sound financial decision

Context matters.

How REITs Fit Into the Conversation

At this point, a natural question arises:

If single-family homes aren't high-growth investments, how does real estate function as an asset class in diversified portfolios?

This is where REITs enter the picture.

What Is a REIT?

A Real Estate Investment Trust (REIT) is a company that owns, operates, or finances income-producing real estate. When you invest in a REIT, you are not buying a house. You are buying shares in a real estate operating business.

REITs typically own portfolios of:

- Apartment communities and multifamily buildings

- Industrial warehouses and logistics centers

- Office and medical office buildings

- Retail centers and net-lease properties

- Data centers, cell towers, and infrastructure

- Healthcare facilities and senior housing

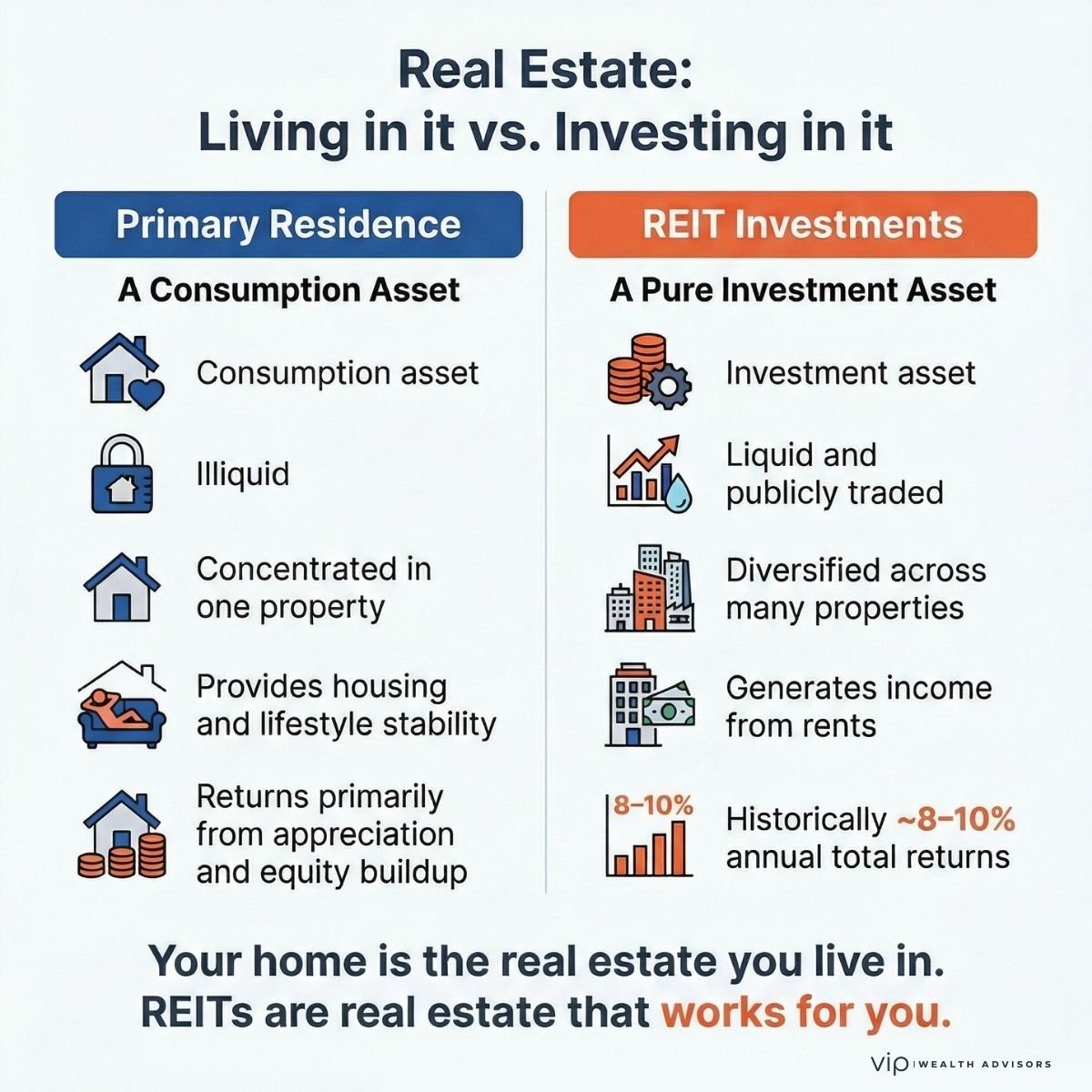

How REITs Differ Fundamentally From Homes

A primary residence is:

- A consumption asset with financial characteristics

- Illiquid and highly concentrated

- Personally managed

- Dependent on one local market

REITs, by contrast, are:

- Pure investment vehicles

- Professionally managed at scale

- Diversified across properties, tenants, and geographies

- Liquid and publicly traded

- Required by law to distribute most taxable income as dividends

In short, REITs represent real estate as an asset class, not housing as a lifestyle choice.

Infographic comparing a primary residence and REIT investments, highlighting liquidity, diversification, income potential, and historical real estate investment returns.

Historical Return Profile of REITs

Over long periods, broad publicly traded REIT indexes have delivered:

- ~8–10% average annual total returns

- A meaningful portion of the return from dividends

- Equity-like volatility over shorter time frames

REIT returns are driven by:

- Rental income

- Rent growth

- Property value appreciation

- Capital structure efficiency

This is meaningfully different from single-family homes, where appreciation alone often defines the conversation.

How Investors Should Think About REITs

REITs belong in a portfolio as:

- A real asset allocation

- A partial inflation hedge

- A source of income

- diversification tool alongside stocks and bonds

They do not replace homeownership.

They solve a different problem.

Your primary residence is the real estate you live in.

REITs are real estate that works for you.

Reframing the Role of a Primary Residence

At VIP Wealth Advisors, we view a primary residence as a hybrid asset with three roles.

1. A Use Asset

A home provides:

- Stability

- Control

- Privacy

- Psychological safety

- A sense of identity

This is the asset you wake up in. That alone changes how it should be evaluated.

2. A Cost Stabilizer

Owning a home, especially with a fixed-rate mortgage, converts:

- Rising rents

- Housing market volatility

Into:

- Predictable long-term housing costs

Over time, inflation works for the homeowner.

3. A Slow Compounding Balance Sheet Asset

Through:

- Loan amortization

- Modest appreciation

A home builds equity quietly in the background.

But it is not designed to maximize returns.

It's designed not to undermine the rest of the plan.

Why the “Greatest Wealth Tool” Narrative Is Outdated

The belief persists because it once fit the environment.

Today's conditions are very different:

- Home prices have outpaced income growth

- Higher interest rates increase lifetime ownership costs

- Taxes, insurance, and maintenance rise faster than inflation

- Career mobility matters more than ever

- Buyers often stretch just to get in

In many markets today, buying a home can:

- Delay investing

- Reduce liquidity

- Increase stress

- Concentrate risk

That doesn't make homeownership wrong. It makes it something that must be planned deliberately.

The Uncomfortable Truth

For many Americans, the home wasn't their best investment.

It was their only disciplined investment.

That distinction is critical.

Modern high-income households have more tools, more access, and more optionality. The home no longer needs to carry the full burden of wealth creation.

The Modern Planning Takeaway

Your primary residence isn't your growth engine. It's your lifestyle anchor and balance-sheet stabilizer. Wealth comes from saving, investing, tax strategy, and staying invested. The house supports the plan. It doesn't replace it.

When clients understand this, decision-making improves dramatically.

Frequently Asked Questions

Is buying a house the best way to build wealth?

Buying a home has historically contributed to net worth for many Americans, but it is not inherently a high-return investment. Its wealth impact comes from forced savings, leverage, and long holding periods rather than superior appreciation.

How much do single-family homes appreciate annually?

U.S. single-family homes have historically appreciated nominally by about 3–5% per year and, over long periods, by roughly 0–2% per year after inflation.

Are homes or REITs better investments?

They serve different purposes. Homes provide utility and stability, while REITs are designed as income-producing investment vehicles with historically higher long-term returns.

What is a REIT?

A REIT is a company that owns or finances income-producing real estate such as apartments, offices, warehouses, and data centers. Investors own shares, not properties.

Do REITs replace owning a home?

No. REITs provide portfolio exposure to real estate, while a home provides lifestyle stability. They complement, not replace, each other.

Should high-income earners prioritize investing over buying a home?

Housing decisions should align with the broader financial plan. Overspending on housing can crowd out investing, while right-sized ownership can support long-term goals.

Does home equity replace diversified investing?

No. Home equity is illiquid and concentrated. Diversified investing remains essential for long-term wealth creation.

How should a home be treated in a financial plan?

A home should be treated as a lifestyle anchor and balance-sheet stabilizer, not a growth engine.

Make Your Home Part of the Plan, Not the Whole Plan

For high-income professionals, housing decisions should support a broader strategy that includes tax planning, investing, and long-term wealth design.

If you're thinking about how your home fits into your financial future, the right framework can make every other decision clearer.