Moving to cash feels safe, but it often causes investors to miss the market’s strongest recovery days.

Key Takeaways

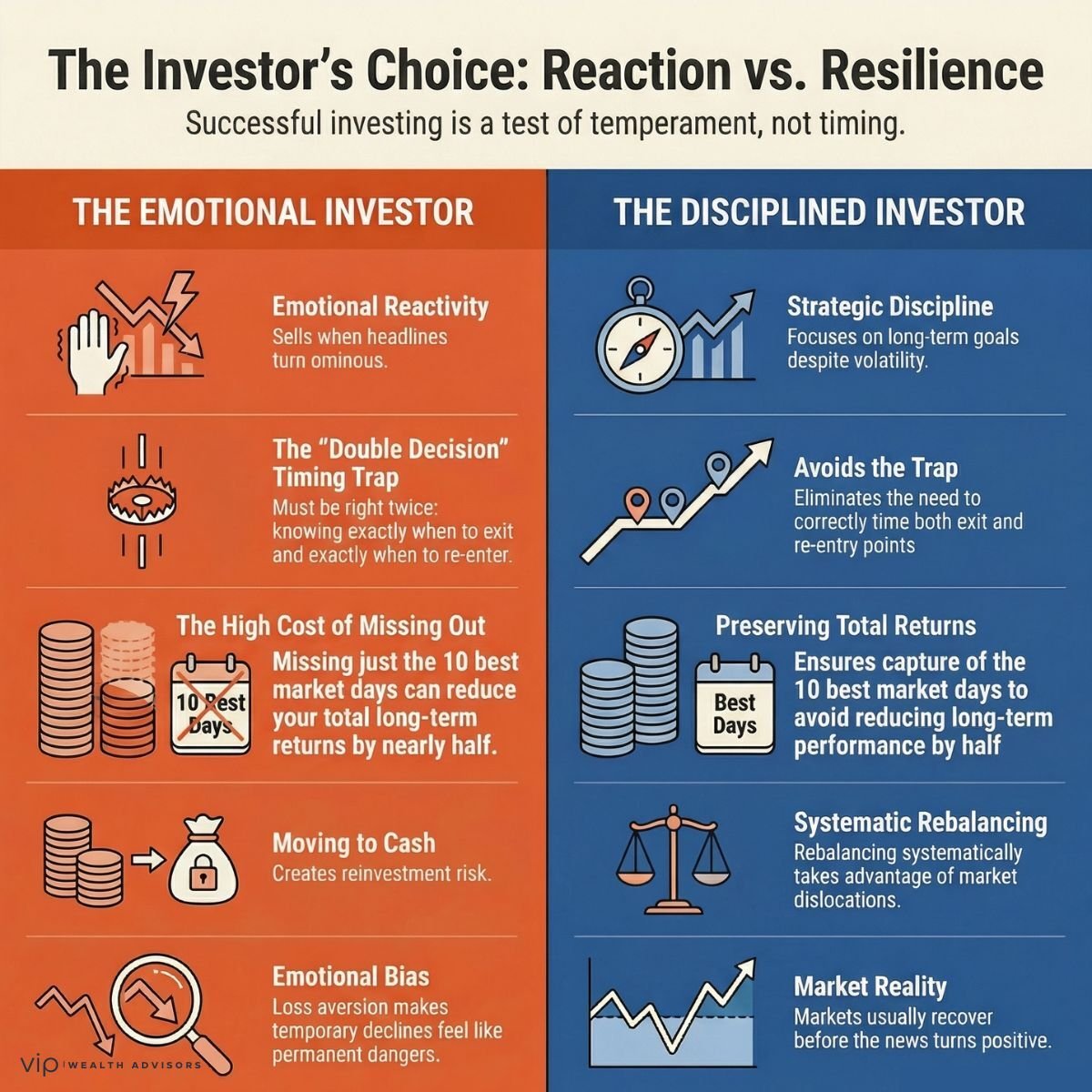

- Deciding whether to move to cash is not just one decision, it is two: when to get out and when to get back in, and most investors get the second part wrong.

- The strongest market recovery days often happen during periods of fear and volatility, when investors are least likely to be invested.

- Missing just a handful of these key days can reduce long-term returns by 30 percent or more.

- This is called market timing, and it is one of the most common and costly mistakes investors make.

- Going to cash may reduce short-term anxiety, but it introduces reinvestment risk that can be far more damaging over time.

- A disciplined strategy focused on allocation, rebalancing, and tax efficiency is more reliable than trying to time the market.

There is a moment that nearly every investor encounters at some point in their investing life, and it rarely arrives during periods of calm or steady growth, but instead emerges precisely when markets become unsettled, headlines turn ominous, and the sense of uncertainty begins to feel less like a passing phase and more like a permanent condition.

It is in moments like these, such as the one we are experiencing now, with geopolitical tensions escalating, oil prices surging, and both stock and bond markets exhibiting unusual and uncomfortable behavior, that even disciplined, experienced investors begin to ask a deceptively simple question: would it be prudent to step aside, move to cash, and wait for clarity before re-engaging?

On its surface, this line of thinking appears rational, even responsible, as it is framed not as panic but as prudence, not as fear but as tactical decision-making; however, the reality is that market timing does not fail because investors lack intelligence or sophistication, but because both markets and human behavior are structured in such a way that consistently executing such a strategy is extraordinarily difficult, if not practically impossible, over time.

Why Market Timing Feels So Right (And Goes So Wrong)

At present, investors are not reacting to abstract fears or hypothetical risks, but to a tangible macroeconomic shock, driven largely by escalating tensions in the Middle East, which have contributed to a sharp increase in oil prices and, by extension, a renewed rise in inflation expectations that is reverberating across global markets.

When energy prices rise in such a pronounced fashion, the effects do not remain confined to a single sector, but instead propagate through transportation costs, manufacturing inputs, supply chains, and ultimately consumer prices, creating a broad-based inflationary impulse that forces markets to reconsider the path of interest rates, monetary policy, and economic growth.

In this environment, the traditional relationships that investors have come to rely upon, such as bonds providing a buffer when equities decline, can break down, leaving investors with the unsettling experience of seeing multiple asset classes under pressure simultaneously, thereby intensifying the emotional discomfort and reinforcing the temptation to seek refuge in cash.

It is precisely under these conditions that market timing begins to feel not only appealing but almost necessary, as it offers the illusion of control in a situation that otherwise feels increasingly unpredictable; however, markets do not reward clarity or comfort, but rather tend to reward discipline exercised in the absence of both.

The Double Decision Problem (The Fatal Flaw)

One of the most fundamental yet frequently overlooked realities of market timing is that it is not a single decision but a sequence of two distinct and equally critical decisions, each of which must be executed correctly for the strategy to succeed.

The first decision, when to exit the market, receives the most attention, as it is often driven by visible declines, alarming headlines, and a desire to mitigate further losses, all of which combine to create a powerful sense of urgency and justification for action.

The second decision, when to re-enter the market, is far more complex and, in practice, far more consequential, as it requires investors to overcome the very same fears and uncertainties that prompted the initial exit, but now with the added burden of having already stepped away from the market.

You have to be right twice. Most investors only focus on getting out and completely underestimate how hard it is to get back in.

The difficulty lies in the fact that markets do not wait for conditions to feel stable or for narratives to resolve neatly; instead, they tend to recover rapidly and often unexpectedly, with some of the strongest market days occurring in close proximity to the most volatile and negative periods.

As a result, investors who successfully exit during periods of decline frequently find themselves paralyzed when it comes time to re-enter, waiting for confirmation that the recovery is “real,” only to discover that a significant portion of the rebound has already taken place.

The Math That Breaks Market Timing

While the conceptual challenges of market timing are significant, the empirical evidence is even more compelling, as numerous studies have demonstrated the disproportionate impact that a small number of strong market days can have on long-term investment outcomes.

Research from Fidelity Investments illustrates that a hypothetical $10,000 investment in the S&P 500, held consistently over several decades, could grow to more than $500,000; however, if an investor were to miss just the five best days during that same period, the ending value would decline by approximately one-third, and missing the ten best days would reduce the outcome by nearly half.

The majority of your long-term returns may come from a surprisingly small number of days. Miss them, and the entire strategy breaks.

What makes this data particularly striking is not merely the magnitude of the impact, but the fact that these best-performing days are not distributed evenly over time, but rather tend to occur during periods of heightened volatility, when investor sentiment is most negative, and the temptation to remain on the sidelines is strongest.

In other words, the very moments that feel least conducive to investing are often the moments that contribute most significantly to long-term returns, thereby creating a paradox in which emotional instincts are directly at odds with optimal financial outcomes.

Behavioral Economics: Your Brain Is Not Your Ally Here

The challenges associated with market timing cannot be fully understood without considering the role of human psychology, as the decisions investors make during periods of volatility are influenced as much by cognitive biases and emotional responses as they are by objective analysis.

The work of Daniel Kahneman, particularly his research on prospect theory, provides critical insight into this dynamic, demonstrating that individuals tend to experience losses with significantly greater intensity than gains of an equivalent magnitude, thereby skewing risk perception and decision-making.

This phenomenon, commonly referred to as loss aversion, helps explain why temporary declines in portfolio value can feel intolerable, even when they are well within the range of expected market behavior, and why investors may feel compelled to take action in order to alleviate that discomfort.

In addition to loss aversion, several other behavioral biases contribute to poor timing decisions, including recency bias, which leads investors to extrapolate recent trends into the future; action bias, which creates a preference for doing something rather than nothing; and regret aversion, which encourages decisions aimed at minimizing future emotional discomfort rather than maximizing long-term outcomes.

Your instincts during volatility are often precisely what lead to bad outcomes.

Collectively, these biases create a powerful psychological environment in which market timing appears not only reasonable but necessary, even as it undermines long-term investment success.

Why This Environment Feels Especially Uncomfortable

The current market environment presents a particularly challenging scenario for investors, as it disrupts the traditional diversification framework that many have come to rely upon, with both equities and fixed income experiencing simultaneous pressure.

This dynamic is largely driven by the inflationary implications of rising energy prices, which have led to higher interest rates and, consequently, declining bond prices, thereby removing one of the primary stabilizing forces within a balanced portfolio.

As a result, investors may feel as though there is no obvious place to seek refuge, which can amplify the sense of urgency and increase the likelihood of reactive decision-making, including attempts to time the market.

However, it is important to recognize that discomfort, while unpleasant, is not synonymous with danger, and that environments characterized by elevated uncertainty are often the same environments in which long-term opportunities begin to emerge.

History’s Verdict: Volatility Is Normal, Timing Is Not

A review of market history reveals a consistent pattern: periods of significant volatility are often accompanied by compelling narratives that appear to justify exiting the market, whether rooted in financial crises, geopolitical conflicts, pandemics, or inflationary shocks.

In each case, the circumstances surrounding the downturn may differ, but the investor response often follows a similar trajectory: many choose to reduce exposure in the face of uncertainty, only to find that markets begin to recover before the underlying concerns have fully resolved.

This recurring pattern underscores a critical point: markets are forward-looking mechanisms that anticipate future developments, rather than reacting solely to current conditions, and as such, they tend to recover in advance of visible improvements in the economic or geopolitical landscape.

Consequently, attempts to time the market based on current events are inherently flawed, as they rely on information already reflected in asset prices.

The Hidden Risk of Going to Cash

While moving to cash during periods of volatility may appear to reduce risk in the short term, it introduces a different and often more insidious form of risk, namely the challenge of determining when to reinvest.

This reinvestment decision is frequently complicated by the same factors that prompted the initial exit, including uncertainty, fear, and a lack of clear signals, which can lead investors to delay re-entry until conditions appear more favorable.

Unfortunately, by the time such conditions are evident, markets have often already experienced a significant recovery, resulting in missed opportunities and diminished long-term returns.

In this way, going to cash does not eliminate risk; rather, it transforms it into a timing problem that is difficult to solve and costly to get wrong. How we help clients stay invested through volatility.

Reframing This Moment: From Threat to Opportunity

Rather than viewing market volatility solely as a source of risk, it can be more productive to view it as a mechanism that creates future return opportunities, as declining asset prices effectively increase the expected returns for investors who can deploy capital during periods of weakness.

This perspective does not imply that investors should act recklessly or disregard risk, but rather that they should approach volatility with a disciplined framework that enables them to take advantage of dislocations in a measured, intentional manner.

Such actions may include continuing regular investment contributions, rebalancing portfolios to maintain target allocations, and selectively increasing exposure to high-quality assets that have become more attractively valued.

Importantly, these decisions are rarely accompanied by a sense of comfort or certainty, and may, in fact, feel counterintuitive, which is precisely why they tend to be effective over the long term.

What Real Risk Management Actually Looks Like

Effective risk management is not achieved through ad hoc decisions or reactive strategies, but through the implementation of a structured and comprehensive plan that accounts for both financial objectives and behavioral tendencies.

This includes maintaining sufficient liquidity to meet near-term needs, thereby reducing the likelihood of forced asset sales during market downturns; constructing a diversified portfolio that aligns with long-term goals and risk tolerance; and establishing a disciplined rebalancing process that systematically adjusts exposures in response to market movements.

In addition, tax-aware strategies, such as harvesting losses to offset future gains, can enhance after-tax returns and provide an additional layer of value during periods of volatility.

Perhaps most importantly, effective risk management requires an awareness of the psychological factors that influence decision-making, and a commitment to adhering to a well-defined plan even when emotions are running high.

The VIP Perspective: Depth Over Reaction

At VIP Wealth Advisors, the emphasis is not on predicting short-term market movements or anticipating every potential risk, but on developing strategies that are robust enough to withstand a wide range of market conditions without requiring constant adjustment.

This approach is particularly relevant for high-income and high-net-worth individuals, whose financial situations often involve additional layers of complexity, including equity compensation, concentrated positions, and significant tax considerations.

In such cases, the primary risks are often not driven solely by market fluctuations, but by the decisions made in response to them, underscoring the importance of a disciplined, process-oriented approach.

When Control Becomes the Risk

Market timing is appealing because it offers the promise of control in an environment that feels uncertain and unpredictable; however, this promise is largely illusory, as the successful execution of such a strategy requires a level of precision and foresight that is difficult to achieve consistently.

The evidence from both historical data and behavioral research suggests that the costs of attempting to time the market, particularly the risk of missing key periods of recovery, can be substantial and long-lasting.

Ultimately, the challenge is not simply avoiding losses but ensuring participation in the gains that follow, which requires a willingness to remain invested even when conditions are less than ideal.

A Better Way Forward

Rather than attempting to navigate market volatility through timing decisions, investors may be better served by focusing on the elements of their financial plan that are within their control, including asset allocation, liquidity management, and disciplined investment processes.

By maintaining a long-term perspective and adhering to a well-structured strategy, investors can position themselves to benefit from market recoveries while minimizing the impact of short-term fluctuations.

In doing so, they shift the focus from predicting the future to preparing for it, which, in the context of investing, is often the more reliable path to achieving sustained success.

Frequently Asked Questions

Does market timing ever work?

Market timing can occasionally succeed over short periods, but it is extremely difficult to execute consistently because it requires accurately predicting both market exits and re-entries.

Why is it so difficult to time the market?

Markets are influenced by countless variables and often recover before conditions feel stable, making it challenging to identify the optimal moments to buy and sell.

What happens if you miss the best days in the market?

Missing even a small number of the market’s best-performing days can significantly reduce long-term returns, sometimes by 30% or more.

Is moving to cash during volatility a good idea?

While it may reduce short-term volatility, moving to cash introduces reinvestment risk and increases the likelihood of missing the market’s recovery.

What role does behavioral finance play in investing?

Behavioral finance explains how cognitive biases and emotional responses can lead investors to make suboptimal decisions, particularly during periods of market stress.

What is a better alternative to market timing?

A disciplined investment approach that includes diversification, rebalancing, and a long-term perspective is generally more effective than attempting to time the market.

Worried About Making the Wrong Move Right Now?

If you're sitting on cash, second-guessing your portfolio, or feeling the urge to "wait it out," you're not alone. But the cost of getting this wrong can be massive.

We help high-income professionals make clear, confident decisions in uncertain markets without relying on guesswork or headlines.