Venezuela's oil headlines mask deep political, legal, and capital risks that make it a poor foundation for disciplined investment decisions.

Key Takeaways

- Venezuela's oil reserves do not translate into near-term or reliable investment returns.

- Political risk, legal uncertainty, and capital intensity overwhelm headline-driven optimism.

- Energy projects require decades of stability, while governments operate on short election cycles.

- Any Venezuela exposure should be treated as optional upside, never a core thesis.

- Disciplined investors focus on cash flow durability, not geopolitical narratives.

The United States just entered Venezuela and arrested Nicolas Maduro.

That sentence alone should stop people cold.

This was not a sanctions update or a diplomatic reshuffling. It was a direct, unprecedented intervention into a country that sits on some of the world's largest oil reserves. Almost immediately, the narrative shifted from geopolitics to opportunity.

Venezuela has oil. A lot of it.

And now, with Maduro removed and a U.S.-backed transition taking shape, investors are hearing a familiar refrain.

Trump is openly talking about stabilizing the country, bringing in U.S. oil companies, rebuilding production, and unlocking billions in value. If that happens, the thinking goes, this could be a once-in-a-generation opportunity.

So the investor's question naturally follows:

"If the U.S. is effectively running Venezuela and American oil companies get the green light, shouldn't this be a great time to invest in U.S. oil stocks?"

It is a reasonable question.

It is also the wrong one.

Because Venezuela is not an oil investment story, it is a case study in political risk, capital intensity, and the brutal mismatch between the time it takes for energy investments to pay off and how quickly political priorities change.

For disciplined investors, the real issue is not whether Venezuela has oil, or even whether U.S. companies are invited in. The issue is whether capital deployed into one of the most politically unstable energy markets in the world can survive long enough, legally enough, and consistently enough ever to earn an acceptable return.

That distinction changes everything.

Why Oil Headlines Create Bad Investment Decisions

Oil stories have a way of short-circuiting investor judgment. Large reserves trigger large assumptions. But reserves do not generate returns. Capital does. And capital only earns a return when it is protected, productive, and patient.

Venezuela has never lacked oil. It has lacked institutions.

That reality does not change because the political wind shifts or because foreign governments step in. The oil has always been there. What has been missing is the infrastructure, legal certainty, operational competence, and political continuity required to turn barrels in the ground into cash flow in shareholders' pockets.

This is where most investment narratives fall apart.

The First Hard Truth: Venezuela's Oil Cannot Produce Returns Quickly

This Is Not Shale. It Is Heavy Oil With Heavy Problems.

A significant portion of Venezuela's reserves sit in the Orinoco Belt and consist of very heavy crude. This is not U.S. shale, where capital can be deployed, recycled, and pulled back quickly.

Heavy oil requires:

- Diluent or upgrading to be marketable

- Specialized refining and blending infrastructure

- Reliable power, pipelines, ports, and export terminals

- Skilled labor and a functioning maintenance culture

Years of underinvestment, corruption, and mismanagement have degraded nearly every part of that system. Even under optimistic political assumptions, this is not a plug-and-play operation.

The Capex Timeline Reality

Investors need to think in timelines, not headlines.

0 to 18 months

The most optimistic outcome is stabilization. Repairs, spare parts, basic maintenance, and debottlenecking. Production might improve modestly, but this is survival mode, not value creation.

2 to 5 years

Meaningful capital deployment begins, assuming contracts hold and politics remain stable. Infrastructure can be upgraded, but risks remain elevated, and returns remain fragile.

5 to 10+ years

A real rebuild only happens if multiple administrations, both U.S. and Venezuelan, remain aligned. That is a very high bar.

Oil projects operate for decades. Governments operate on election cycles. That mismatch is the core risk investors keep ignoring.

Why CEOs and Boards Are Not Rushing In

Political rhetoric can change overnight. Capital allocation does not.

Behind closed doors, oil company boards are asking very different questions than the ones investors hear on television:

- Is this activity legal today, and will it remain legal next year?

- Can profits be repatriated without restriction?

- Can reserves be booked on the balance sheet?

- Are contracts enforceable under international law?

- What happens if the political environment shifts again?

If a project only works as long as political goodwill remains intact, it is not an investment. It is a policy-dependent trade.

Boards remember history. Venezuela has nationalized assets before. Arbitration battles have dragged on for years. Those scars do not disappear because of a press conference.

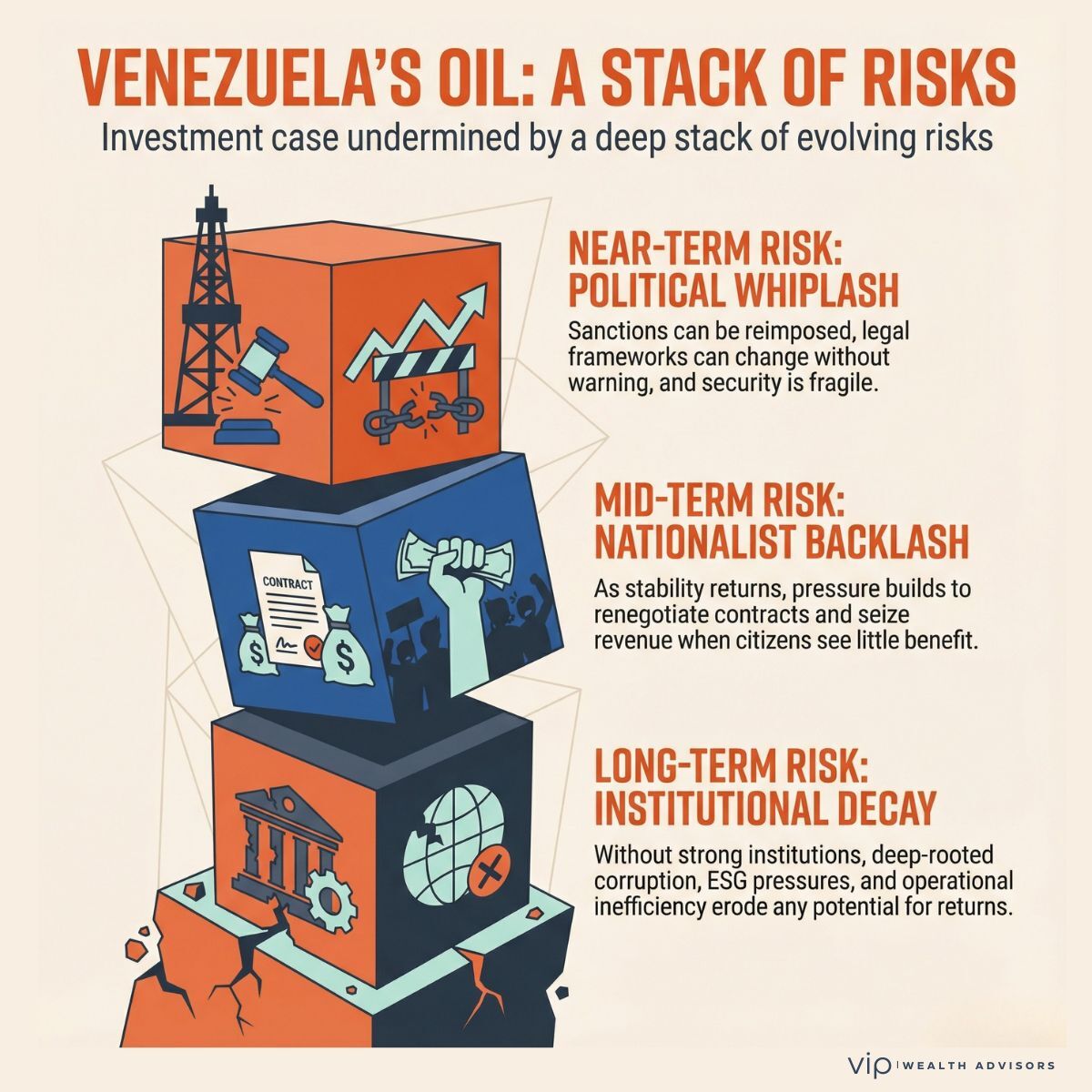

The Risk Stack Investors Are Underestimating

Near-Term Risks (0 to 12 Months)

- Sanctions can be loosened and reimposed quickly

- Legal frameworks can change without warning

- Security risks spike during political transitions

- Operational continuity is fragile

Mid-Term Risks (1 to 5 Years)

- Resource nationalism often returns once public pressure builds

- Contracts get renegotiated when citizens see limited benefit

- Payment and receivables risk increases

- Governments seek revenue wherever it can be extracted

Long-Term Risks (5 to 15 Years)

- Heavy oil faces increasing economic and environmental pressure

- ESG, litigation, and reputational risks compound

- Weak institutions invite corruption and inefficiency

- The resource curse reasserts itself

These are not hypothetical risks. They are structural.

The Regime Change Question No One Wants to Answer Honestly

Oil infrastructure does not care who occupies the presidential palace. Capital markets do.

If the timeline to meaningful returns stretches five to ten years or longer, investors must confront a simple reality: political alignment today does not guarantee policy continuity tomorrow.

What happens when Trump leaves office?

What happens if the next administration has different priorities?

What happens if sanctions return or contracts are challenged?

Boards discount all of this heavily. Investors should, too.

Will Venezuelans Actually Benefit From This Oil?

This is not a moral debate. It is a financial one.

If Venezuelan citizens do not see tangible improvements in living standards, political pressure will rise. When that happens, oil companies become convenient targets.

For long-term success, Venezuela would need:

- Transparent royalty and tax systems

- Audited national oil revenues

- Infrastructure reinvestment

- Anti-corruption enforcement

- Stabilization mechanisms to manage boom and bust cycles

Without institutions, oil wealth concentrates. When it concentrates, backlash follows. When backlash follows, investors pay the price.

Is This Legal or Is It Just Colonization With Better Branding?

Legality and legitimacy are not the same thing.

U.S. companies cannot operate in Venezuela without lawful authorization under U.S. sanctions rules and valid Venezuelan contracts. Even then, legality does not shield companies from protests, political backlash, or reputational damage.

Optics matter because optics shape policy. Policy shapes cash flow. Cash flow determines valuation.

This is not ideology. It is risk pricing.

How Investors Should Actually Think About U.S. Oil Companies

Here is the key takeaway:

If Venezuela works, it is an optional upside.

If it fails, it should not impair the core business.

Better investor questions include:

- Does this company generate strong returns without Venezuela?

- Is capital allocation disciplined or empire-driven?

- Are dividends and buybacks prioritized?

- How explicitly does management discuss political risk?

The strongest oil companies do not need Venezuela to justify their valuations. If they participate, it should be cautiously, selectively, and opportunistically.

The Bigger Portfolio Lesson

Venezuela is a reminder that:

- Headlines are not investment theses

- Concentration risk hides inside narratives

- Political risk compounds slowly, then suddenly

The Difference Between Investing and Believing a Story

Venezuela is not an oil opportunity. It is a stress test.

The real question is not whether oil can be extracted. It is whether capital can survive long enough to earn a return.

That is the difference between investing and speculating.

Venezuela Oil and Investing: Investor Questions Answered

Can U.S. oil companies legally invest in Venezuela right now?

Only with explicit authorization under U.S. sanctions law and valid contracts under Venezuelan law. These permissions can change quickly.

How long will it take for U.S. oil companies to see a return?

Meaningful returns are likely to require sustained capital investment over multiple years, stable contracts, and political continuity.

Is Venezuela's oil actually profitable to extract?

It can be, but heavy crude carries higher costs, requires specialized infrastructure, and often trades at a discount.

What are the biggest risks over the next 12 months?

Sanctions reversals, legal uncertainty, political instability, and security risks during any transition period.

Could Venezuela nationalize assets again?

History suggests it is possible. This risk never fully disappears without strong institutions.

How does regime change impact oil investments?

Oil projects outlive governments. Policy reversals can strand capital or destroy expected returns.

Will the next U.S. administration support this approach?

There is no guarantee. That uncertainty alone raises the required return threshold.

Will Venezuelan citizens benefit from oil production?

Only if revenues are transparently managed and reinvested, without that, the backlash risk grows.

Is investing in oil companies with exposure to Venezuela ethical?

Ethics and economics often intersect. Reputational and ESG risks can become financial risks.

Should investors buy U.S. oil stocks because of Venezuela?

No. Venezuela should be treated as an optional upside, not a core thesis.

What is a smarter way to gain energy exposure today?

Own high-quality operators with disciplined capital allocation, strong balance sheets, and diversified asset bases.

Thinking About Energy Exposure or Political Risk in Your Portfolio?

This article highlights why headlines are not investment theses. If you want help stress-testing your portfolio, identifying hidden concentration risk, and building resilient exposure to real return drivers, a strategic review matters.