Gen X investors typically want integrated, tax-aware, judgment-driven financial advice that prioritizes clarity, optionality, and real-world complexity over products or performance theater.

Key Takeaways

- Gen X investors tend to value judgment, integration, and tax-aware strategy over product recommendations or performance claims.

- Complexity, not motivation, is the defining financial challenge at this stage of life.

- Optionality, flexibility, and risk reduction often matter more than maximizing returns.

- The right advisor functions as a coordinator and translator, not a salesperson.

If you're Gen X, you've already done the hard part.

You built the income.

You accumulated assets.

You survived market crashes, tech bubbles, restructurings, layoffs, and more than one "this time is different" moment.

What you're dealing with now isn't motivation. It's complexity.

Complex taxes. Concentrated positions. Equity compensation that doesn't behave the way the brochure implied. Business value tied up in something illiquid. Kids who are suddenly expensive adults. Parents who are quietly becoming a financial variable.

I know this because I'm Gen X too.

I grew up learning early that institutions don't always hold, careers aren't linear, and no one is coming to clean up the mess if you get it wrong. That worldview shapes how I think about money and it's usually the same worldview shared by the Gen X clients who find their way here.

This article is for you if generic financial advice has started to feel increasingly irrelevant and you're looking for something more grounded, more integrated, and frankly more adult.

Why You Likely Approach Wealth Differently Than the Generations Around You

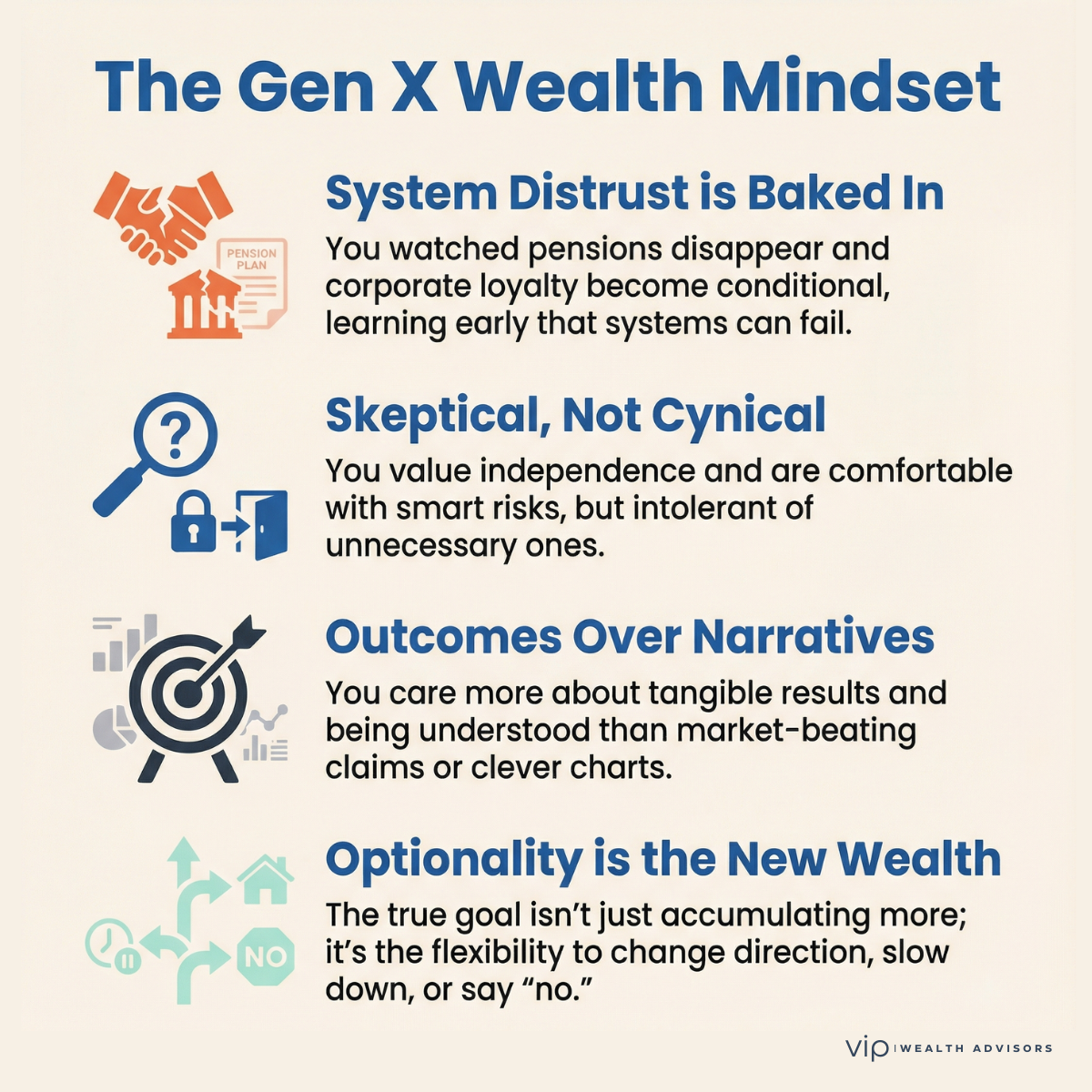

If you're Gen X, you didn't grow up expecting the system to work perfectly.

You watched pensions disappear mid-career.

You saw corporate loyalty turn conditional.

You lived through multiple market cycles early enough to know volatility isn't theoretical.

As a result, you probably relate to a few of these instincts:

- You're skeptical, but not cynical

- You value independence, but not recklessness

- You're comfortable with risk, but intolerant of unnecessary risk

- You care far more about outcomes than narratives

You don't want to be impressed. You want to be understood.

And that fundamentally changes what you expect from a financial advisor.

What You're Probably Done With by Now

Most Gen X clients I work with don't struggle to articulate what they want.

They struggle to find anyone who isn't still offering what they've already outgrown.

Product-First Advice

If advice feels like a prelude to a pitch, your guard goes up immediately. You've seen enough cycles to know no product is a strategy by itself.

Performance Theater

Market-beating claims, clever charts, and short-term comparisons feel hollow once you've lived through 2000, 2008, 2020, and everything since. Returns matter, but they are rarely the real problem.

Being the Project Manager of Your Own Wealth

You're busy. You don't want to coordinate among an advisor, a CPA, an estate attorney, and a benefits department, hoping nothing falls through the cracks. You want someone who actually sees the whole picture.

Generic Planning Frameworks

Once equity compensation, business ownership, multi-state taxes, or liquidity events enter the picture, cookie-cutter advice breaks down fast. You can usually tell within minutes when the advice isn't tailored to your situation.

What You Probably Want Instead

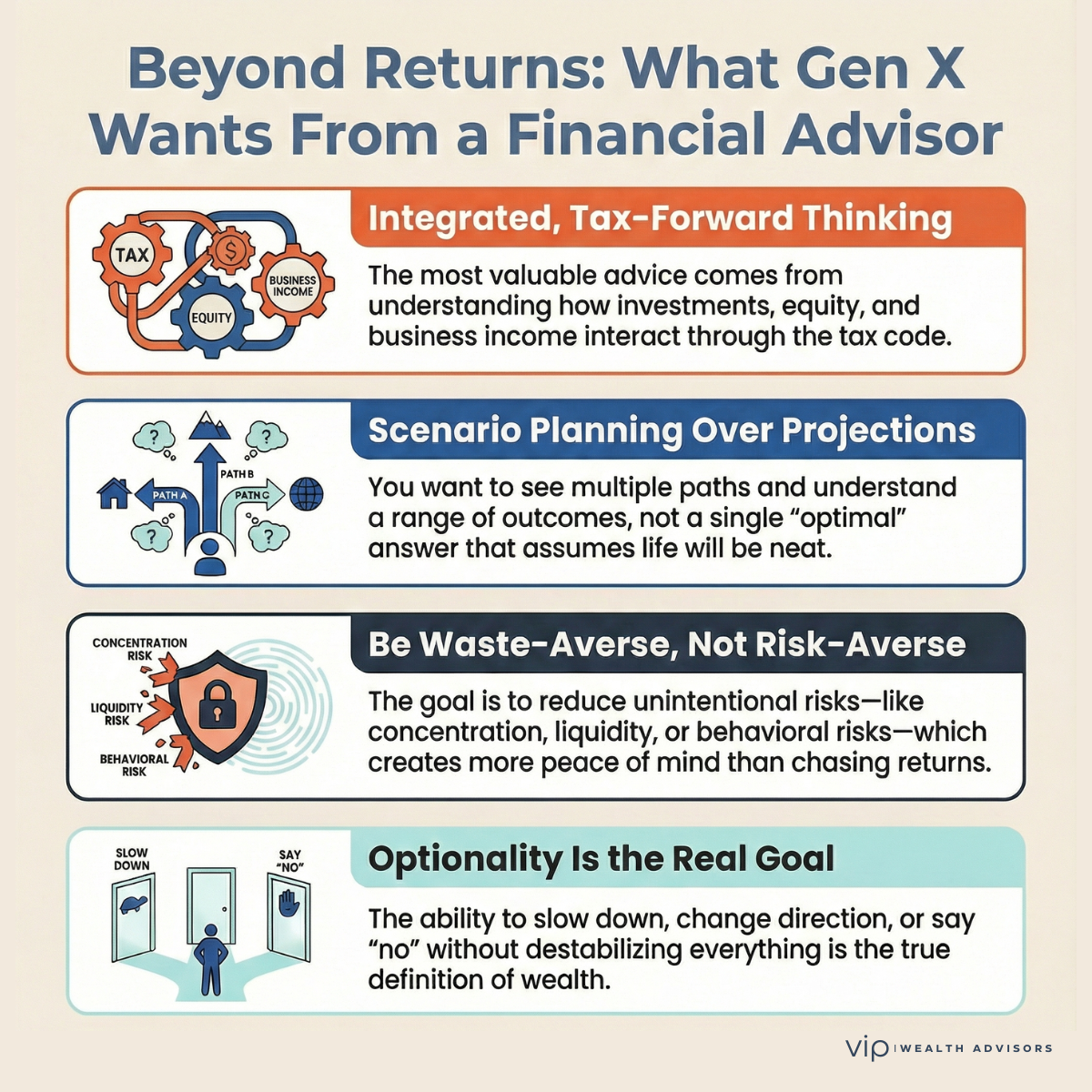

Integrated, Tax-Forward Thinking

At this stage, taxes aren't a footnote. They're a compounding force.

The most valuable advice doesn't come from chasing returns. It comes from understanding how investment decisions, equity compensation, business income, and estate planning interact through the tax code over time.

As a Gen Xer, you likely care less about headlines and more about what you keep.

Smart timing. Smart structuring. Fewer irreversible mistakes.

For Gen X investors, tax efficiency often has a larger long-term impact than incremental differences in investment performance.

Scenario Planning, Not a Single "Optimal" Answer

You don't want one answer that assumes life will behave neatly.

You want to see paths.

What if you sell the business sooner than planned?

What if equity compensation accelerates or stalls?

What if one of you steps back earlier than expected?

The value isn't the projection. It's understanding the range of outcomes and knowing where you still have control.

Risk Reduction That Doesn't Feel Like Retreat

You're not risk-averse. You're waste-averse.

You want to know where risk is intentional and where it's accidental. Concentration risk. Liquidity risk. Legislative risk. Behavioral risk.

Reducing these exposures often creates more peace of mind than chasing incremental returns ever could.

Optionality as the Real Goal

Earlier in life, maximizing wealth made sense.

Now, optionality matters more.

The ability to slow down. Change direction. Say no. Support family. Fund interests that don't need to scale. Take time without destabilizing everything else.

For many Gen Xers, that flexibility is the true definition of wealth.

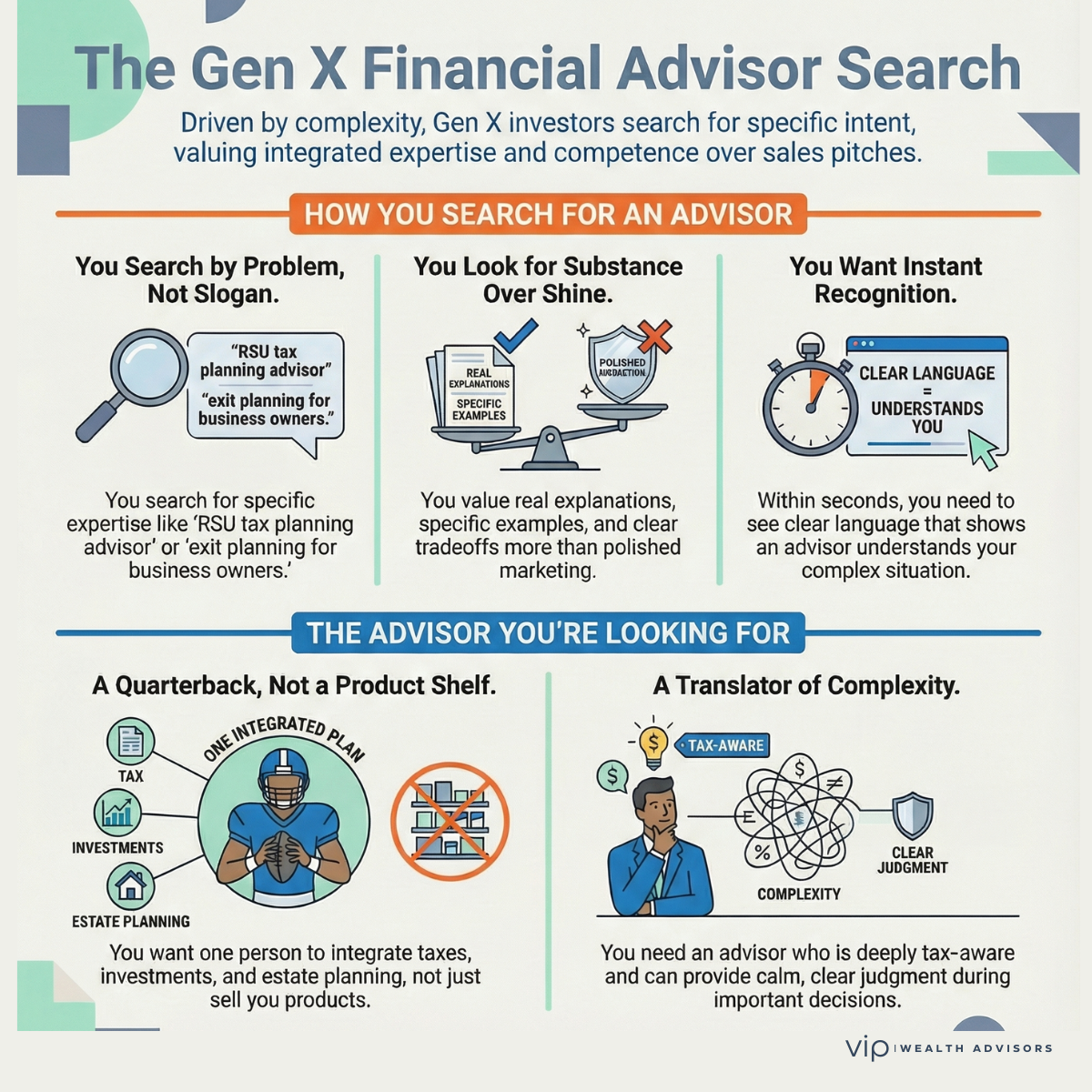

How You Likely Search for a Financial Advisor

Most Gen X investors don't browse for advisors. They search with intent.

Usually, it starts with a specific issue that's become too consequential to ignore.

Common searches look like:

- "fee-only financial advisor for executives"

- "RSU and stock option tax planning advisor"

- "AMT ISO exercise advisor"

- "flat fee financial advisor high income"

- "exit planning advisor for business owners"

Notice the pattern. The problem comes first. The advisor comes second.

You're not comparing slogans. You're evaluating competence.

You read long-form content. You scan for depth. You pay attention to how tradeoffs are explained. You want to see evidence of pattern recognition, not theory.

What Makes You Lean In When You Land on an Advisor's Website

Recognition, Immediately

Within seconds, you want to know whether this advisor actually works with people like you.

Clear language beats clever language every time.

"If you're a high-earning professional or business owner with complex taxes and concentrated wealth, you're in the right place."

That kind of clarity builds trust quickly.

Substance Over Shine

You're not looking for polish. You're looking for understanding.

Real explanations. Specific examples. Honest math. Clear tradeoffs. Depth signals seriousness.

A Point of View

You don't need neutrality. You need judgment.

Advisors who have thought deeply about what works, what doesn't, and why tend to stand out. Boundaries and opinions matter more than universal disclaimers.

Rational, Transparent Pricing

You don't mind paying for expertise. You mind feeling skimmed.

Flat, transparent fees often feel more aligned than percentage-based pricing that rises regardless of complexity or workload. You want to pay for value, not permanence.

The Advisor You're Probably Looking For (Whether You'd Phrase It This Way or Not)

Most Gen X clients aren't looking for a cheerleader.

They're looking for someone who functions as:

- A quarterback, not a product shelf

- A translator between complexity and clarity

- Someone deeply tax-aware by default

- Calm and experienced during high-stakes decisions

- Comfortable saying "not yet" or "don't do this"

You want fewer meetings, but better ones. Fewer recommendations, but stronger conviction behind them.

You want to simplify your financial life without breaking anything important.

Why This Stage Matters More Than the Ones Before It

If you're Gen X, you're entering one of the most financially consequential decades of your life.

- Peak earnings

- Liquidity events

- Major tax exposure

- Intergenerational planning

- Lifestyle decisions that don't rewind easily

The cost of poor advice now isn't inconvenience. It's lost optionality.

That's why the advisor relationship matters more now than ever before, and why the wrong fit feels increasingly apparent.

A Closing Thought From One Gen Xer to Another

You don't need to be sold.

You don't need to be dazzled.

You need clarity. Integration. Judgment. And the quiet confidence that someone is watching the whole picture while you live your life.

If this article resonates, it's likely because generic advice has already stopped adding value.

That realization alone puts you ahead of the curve.

FAQ - Frequently Asked Questions

What should I look for in a financial advisor as a Gen X high-income professional?

You should look for an advisor who understands complex tax planning, equity compensation, or business ownership and integrates investments, taxes, and estate planning into a cohesive strategy. Experience, judgment, and transparency matter more than salesmanship.

Why do many Gen X investors prefer fee-only or flat-fee financial advisors?

Flat-fee or fee-only pricing often feels more aligned because it's transparent and not tied solely to asset growth. Many Gen X investors prefer paying for expertise and complexity rather than an ongoing percentage of their net worth.

Is investment performance the most important factor for Gen X investors?

Investment performance matters, but it's rarely the primary driver. Gen X investors often prioritize tax efficiency, risk management, decision support, and preserving long-term flexibility over chasing incremental returns.

How do Gen X investors typically find financial advisors?

Most Gen X investors search online for specific problems, such as tax planning for stock options, business exit planning, or fee-only advisors for executives. They evaluate advisors based on depth, clarity, and demonstrated experience.

What financial challenges tend to matter most to Gen X?

Common challenges include managing concentrated stock positions, navigating equity compensation taxes, planning for business exits, coordinating tax and estate strategies, supporting both children and aging parents, and simplifying increasingly complex finances.

Why does optionality matter so much to Gen X?

Gen X values optionality because they grew up learning that stability isn't guaranteed. Having flexibility, control, and the ability to adapt matters more than maximizing wealth at all costs.

Looking for Advice That Actually Fits This Stage of Life?

If you're a Gen X professional or business owner dealing with complex taxes, concentrated wealth, or high-stakes decisions, the right guidance can protect your optionality and simplify everything else.