Founder exits succeed long-term when the transaction is planned around the life, purpose, and wealth strategy that follows.

Key Takeaways

- An exit is a beginning, not an ending. Founders often underestimate the emotional, psychological, and financial complexity that follows liquidity.

- The most valuable planning happens pre-exit. QSBS, option strategy, AMT mitigation, and estate planning must be executed years in advance.

- Deal structure drives after-tax outcomes. Valuation matters less than stock vs. asset treatment, rollover equity, and state tax exposure.

- Post-exit behavior determines success. Without structure, founders often overspend, overinvest, or rush into the wrong second act.

- The VIP Framework creates intentional outcomes. A staged approach helps founders preserve wealth, design purpose, and avoid common traps.

For years, often decades, founders pour everything they have into building their companies: time, identity, relationships, health, and nearly every ounce of creative energy. The business becomes more than a business. It becomes a mission, a container for ambition, and in many cases, the defining chapter of a founder's life.

So, when that long-awaited moment finally arrives, the term sheet, the LOI, the definitive agreement, the wire hitting the account, founders expect to feel fulfilled. But more often than not, what they actually feel is something far more complicated.

Yes, the exit brings options. Yes, it can create generational wealth. But financial independence is only one piece of a much larger story. The truth is something founders aren't told enough:

An exit is not the destination. It's the beginning of the next chapter, and for many founders, it's the chapter they're least prepared for.

At VIP Wealth Advisors, we've seen this play out across many liquidity events. The founders and early-stage employees who thrive after an exit aren't the ones who sold at the highest valuation. They're the ones who treated their exit as a strategic transformation: financially, psychologically, and professionally.

This article is your blueprint for making that happen. Whether you're five years out, twelve months from an LOI, or already staring down a term sheet, this is your guide to designing the life that comes after the liquidity.

The Founder Reality: You Don't Plan an Exit for the Transaction; You Plan It for the Life That Follows

Founders often prepare meticulously for the financial aspects of an exit. What they rarely prepare for is the emotional shift that follows.

Founders often experience:

- Loss of identity: "Who am I now that the company isn't mine?"

- Decision overload: An influx of liquidity with no plan creates hidden anxiety.

- Lack of structure: The calendar goes silent overnight.

- Social dislocation: The world treats you differently post-liquidity.

- Purpose drift: Without the problem-solving pressure cooker, many founders feel aimless.

- Lifestyle inflation pressure: The people around you suddenly have big ideas for your money.

These challenges are normal. But without a plan, they can lead to destructive financial decisions, including overallocation to risky ventures, poor tax decisions, impulsive lifestyle choices, or jumping into a second business out of boredom rather than clarity.

This is why VIP Wealth Advisors approaches founder planning through a three-part structure:

The VIP Framework: Pre-Exit → At-Exit → Post-Exit

This isn't a slogan, it's an operating system. And it's built around one premise:

Everything founders want after an exit must be designed before the exit.

Let's break it down.

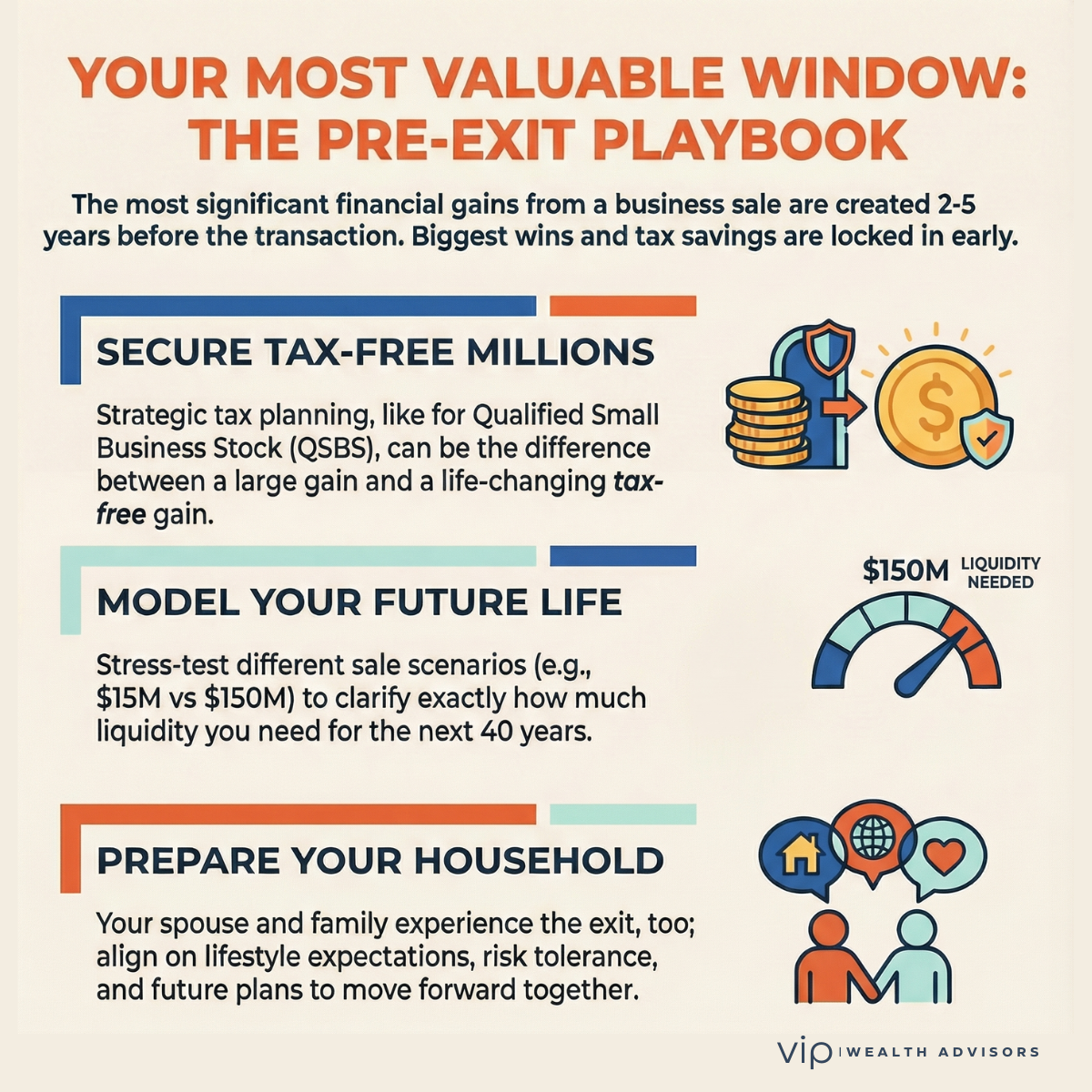

1. Pre-Exit (2–5 Years Before a Liquidity Event): The Most Valuable Phase

The most significant financial gains and the biggest tax savings don't come from the transaction itself. They're created long before the LOI.

A. Tax Optimization: The Most Overlooked and Most Valuable Founder Advantage

Founders consistently underestimate the impact of tax planning on their outcomes. Founders should be evaluating:

✓ Qualified Small Business Stock (QSBS)

The difference between selling at a $20M gain vs. a $20M tax-free gain is life-changing.

- Should you stack shares?

- Can you qualify for the $10M exclusion?

- Should you "pack" QSBS into certain trust vehicles?

- Are you consulting an advisor who knows the rules and risks?

QSBS planning must be done years before the exit.

✓ ISO and NSO Optimization

Founders often create avoidable six-figure AMT bills by exercising options improperly.

You want to bring clarity to:

- The split basis between regular tax and AMT tax

- Why exercising early without analysis is dangerous

- How AMT credit recapture works after the sale

- Why founders accidentally trigger disqualifying dispositions

✓ Pre-Liquidity Estate Strategy

We're talking:

- Spousal Lifetime Access Trusts (SLATs)

- Intentionally Defective Grantor Trusts (IDGTs)

- Charitable Remainder Trusts (CRTs)

- Donor-Advised Funds (DAFs)

- Dynasty trusts

A well-designed pre-exit estate plan can shield millions from future estate taxes before the wealth even exists.

B. Scenario Modeling and Stress Testing

Founders need answers to questions like:

- What does life look like if I sell for $15M vs. $40M vs. $150M?

- What if the deal involves a heavy earn-out?

- What happens if the buyer pays 60% in stock and 40% in cash?

- How much liquidity do I actually need for the next 40 years?

VIP Wealth Advisors models cash flow for:

- Lifestyle

- Taxes

- AMT

- Potential capital losses

- Charitable goals

- Startup investments

- Rollover equity

C. Preparing the Founder's Family

Most founders forget:

Your spouse and family experience the exit, too.

This includes:

- Joint decision-making

- Lifestyle expectations

- Future travel, home, and education plans

- Risk tolerance alignment

- Family governance and wealth values

The household must move forward together.

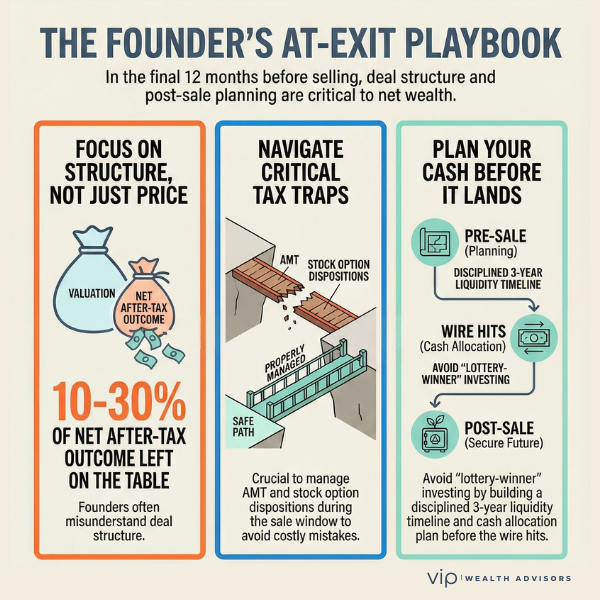

2. At-Exit (12 Months Before the Deal + the Transaction Window)

When the LOI arrives, everything accelerates. And everything suddenly matters.

A. Deal Structure Drives Your Tax Outcome

Founders often obsess over valuation when they should be obsessing over:

- Stock sale vs. asset sale

- Escrow

- Indemnification

- Rollover equity terms

- Earn-out conditions

- Installment payments

- Tax domicile strategy

- State tax exposure

Founders routinely leave 10–30% of their net after-tax outcome on the table by misunderstanding deal structure.

B. AMT and Option Disposition Traps

During the sale, this is when things get messy:

- Disqualifying dispositions

- AMT credit recovery timelines

- Basis allocation for ISOs vs. regular tax

- NSO wage reporting

- The interaction between NII tax, capital gains, and AMT

C. Liquidity Staging and Cash Allocation

So many founders go all-in on:

- A new venture

- Angel investing

- A speculative investment

- Real estate

- Crypto

Before they’ve even run a full liquidity map.

VIP Wealth Advisors builds:

- A 3-year liquidity timeline

- Tax due date mapping

- Cash reserve planning

- A measured, disciplined investment deployment schedule

No lottery-winner behavior. No firehose investing.

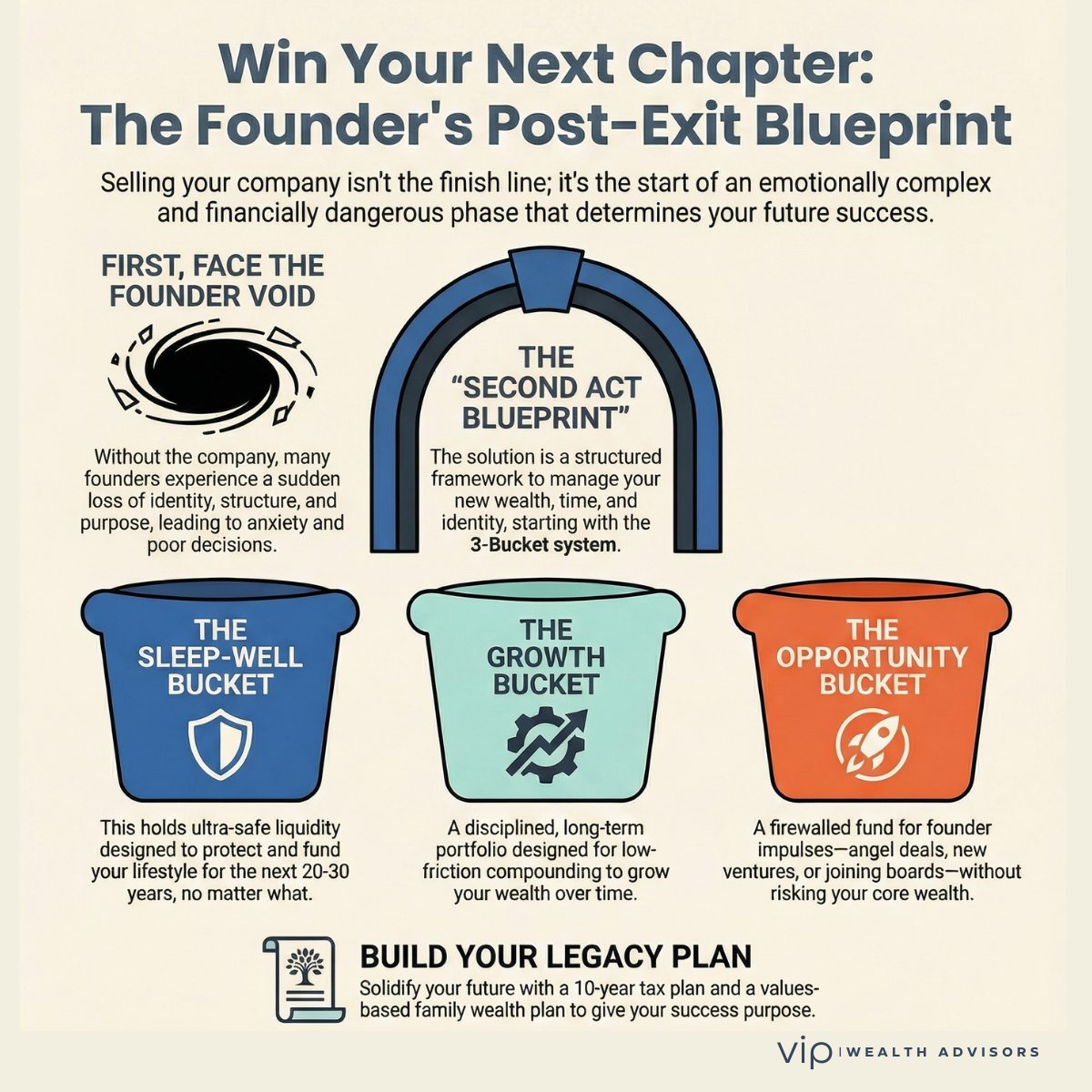

3. Post-Exit (Day 1 to Year 5): Where Founders Win or Lose the Next Chapter

This is the most emotionally complex and financially dangerous phase.

A. The Psychological Reset

Loss of structure. Too much freedom. Too many choices. Family expectations. Sudden wealth visibility.

- "What do I do now?"

- "What does my life look like without the company?"

- "Do I want to start something new or take a break?"

- "Who am I outside of being a founder?"

This isn't fluff. This is where founders crumble without support.

B. The VIP "Second Act Blueprint"

Founders get:

✓ The Sleep-Well Bucket

Ultra-safe liquidity to protect the next 20–30 years of life.

✓ The Growth Bucket

Long-term, low-friction compounding in a disciplined portfolio.

✓ The Opportunity Bucket

For those founder impulses:

→ Angel deals

→ Venture investing

→ Joining boards

→ Building a second company

This bucket has boundaries so founders don't quietly torch 30% of their net worth.

✓ A 10-Year Tax Plan

With:

→ AMT credit timing

→ Tax loss harvesting

→ State tax migration mapping

→ Charitable stacking strategies

→ Exit timing for rollover equity

✓ A Values-Based Family Wealth Plan

This is where wealth becomes purpose-driven:

→ Family mission statement

→ Philanthropic identity

→ Next-gen wealth education

→ Guardrails on lifestyle inflation

Founder Mistakes: The Costly Errors We See Most Often

1. Negotiating valuation instead of after-tax outcome

Founders leave millions behind.

2. Not completing pre-exit estate planning

The IRS gets the windfall instead of your kids.

3. Exercising stock options without an AMT strategy

A rookie mistake with six-figure consequences.

4. Rolling over too much equity

You just sold your company, don’t repurchase it by accident.

5. Starting planning after the LOI

Too late for the most valuable strategies.

6. Underestimating lifestyle creep

A $20M exit can be destroyed by a $1M/year lifestyle.

The Exit Is a Chapter…Not the Story

Selling your company is not the finish line you imagine it to be. It's the gateway into a new life: one with more freedom, more options, more complexity, and more risk than you've ever faced as a founder.

You deserve a next chapter that feels intentional, well-designed, and aligned with who you've become, not a rushed collection of decisions made under pressure.

At VIP Wealth Advisors, we help founders:

- Master the tax strategy

- Design a multi-stage plan

- Protect their lifestyle

- Build generational wealth

- Create purpose after the exit

- And step confidently into their second act

The valuation will matter for a moment.

The life you build afterward will matter forever.

If you want to explore what your next chapter could look like, we’re ready.

Q&A

When should founders start exit planning?

Ideally, 2–5 years before selling, when you can still optimize taxes, equity, estate planning, and valuation strategy.

What is QSBS and why does it matter?

QSBS can exclude up to $10M, and often far more, from federal capital gains tax. But the rules must be met years before an exit.

Should I exercise stock options before a sale?

Maybe. Maybe not. The AMT implications can be substantial. You need a full AMT vs. regular tax analysis before acting.

How do I minimize taxes when selling my company?

Start early, structure the deal properly, leverage trusts, maximize QSBS, and plan for AMT. Timing and structure matter more than valuation.

Is rollover equity good or bad for founders?

It can be incredibly valuable or incredibly risky. It depends on deal terms, liquidity needs, and diversification.

How much cash should founders keep after an exit?

We typically recommend a 2–3 year liquidity runway, especially if interest rates are elevated and markets are volatile.

What’s the biggest mistake founders make during an exit?

Negotiating the deal structure last. Structure determines the after-tax outcome.

Should founders set up trusts before or after a sale?

Nearly always before. After the sale, the value is “locked in,” and trust strategies lose their tax advantage.

How should I invest after a liquidity event?

Slowly, deliberately, and with a structured plan. A disciplined deployment schedule prevents regret.

How do I avoid lifestyle inflation?

Use a cashflow map, establish spending guardrails, and tie lifestyle decisions to long-term planning, not emotion.

Design Your Second Act With Intention

If you are thinking about an exit - or already reviewing a term sheet - the most valuable planning decisions happen before the deal closes.