Private credit can offer income and diversification, but its illiquidity, risk structure, and tax treatment make planning fit more important than headline yield.

Key Takeaways

- Private credit offers income-driven returns but comes with meaningful illiquidity and complexity.

- Reported stability can mask real economic risk during market stress.

- Tax treatment often reduces after-tax returns for high-income investors.

- Proper sizing and liquidity planning matter more than yield.

- Private credit works best as part of a broader, planning-first portfolio.

Private credit has become one of the most talked-about asset classes of the past decade. What was once a niche corner of institutional portfolios is now marketed to high-net-worth investors as a source of income, diversification, and stability in an uncertain market environment.

That attention naturally raises an important question:

Should you be investing in private credit?

For some investors, the answer may be yes. For others, the risks, complexity, and illiquidity make it a poor fit. The difference has far less to do with market forecasts and far more to do with how private credit actually works and how it fits into a real financial life.

This article explains what private credit is, why it has grown so rapidly, how it behaves across market cycles, the risks and tax implications investors often overlook, and how to determine whether it belongs in your portfolio.

What Is Private Credit?

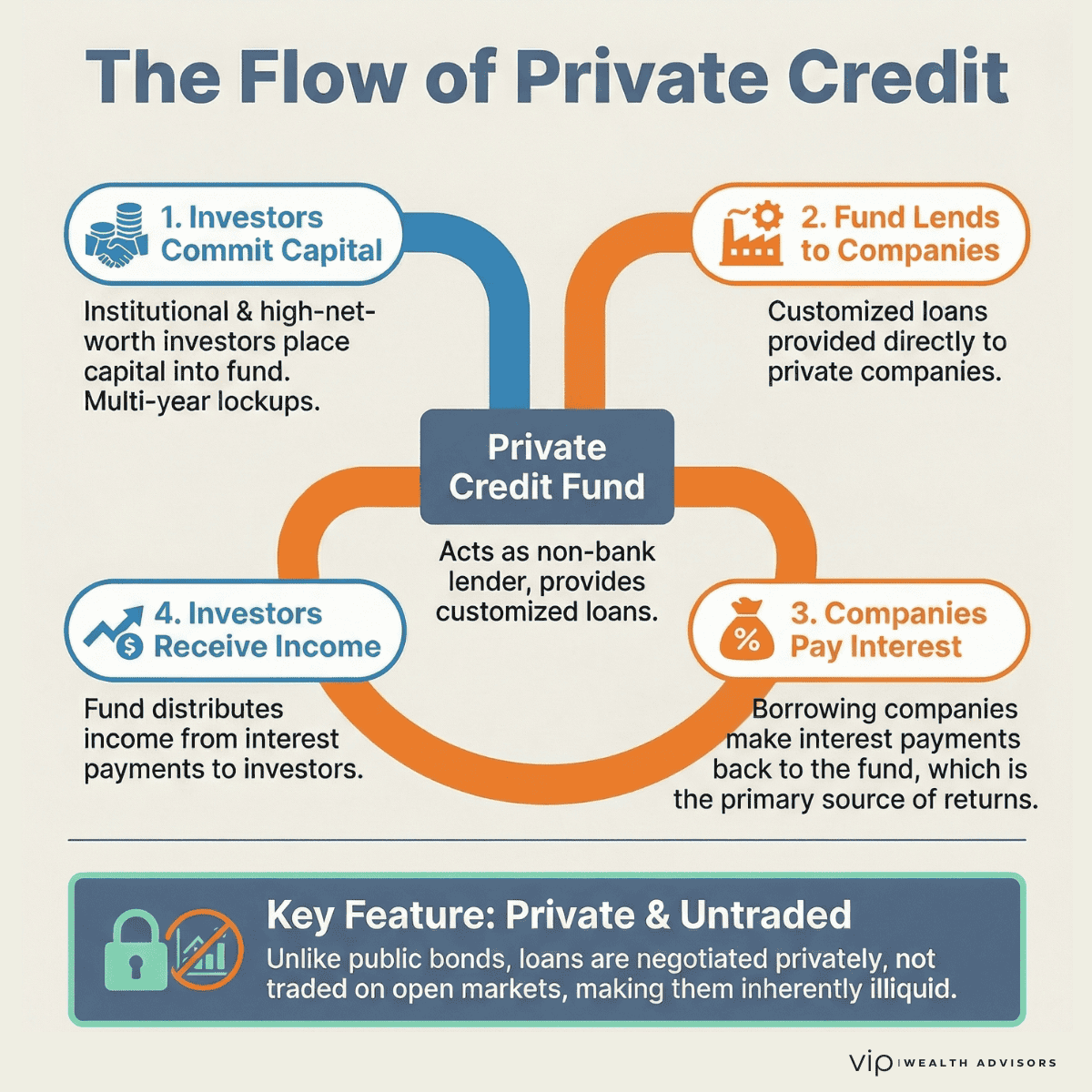

Private credit refers to loans made by non-bank lenders, typically private funds, directly to companies outside of the public bond markets. Instead of issuing publicly traded bonds, borrowers work directly with private lenders to structure customized financing.

Common forms of private credit include:

- Direct lending to middle-market companies

- Private debt used in private equity transactions

- Asset-backed lending

- Infrastructure and specialty finance loans

Investors access private credit through pooled investment vehicles, often structured as limited partnerships with multi-year lockups.

Why Has Private Credit Grown So Quickly?

The growth of private credit is not a temporary trend. It is the result of structural changes in the financial system.

Following the Global Financial Crisis, banks faced higher capital requirements, stricter lending standards, and increased regulatory scrutiny. Holding leveraged or bespoke corporate loans became more expensive and less attractive for traditional lenders.

Private credit funds stepped into that gap.

At the same time, investors endured years of ultra-low interest rates, followed by sharp volatility in public bond markets. Private credit offered an appealing alternative:

- Higher income potential

- Floating-rate structures

- Reduced interest-rate sensitivity

- Perceived downside protection through covenants

As a result, private credit has evolved from a niche strategy into a core allocation for pensions, endowments, insurers, family offices, and increasingly, high-net-worth investors.

How Private Credit Actually Generates Returns

Private credit returns primarily come from interest income, not price appreciation.

Most loans are floating-rate, meaning income rises as interest rates increase. In addition to base interest, lenders may receive:

- Origination fees

- Prepayment penalties

- Payment-in-kind (PIK) interest

- Equity kickers in certain structures

This income-heavy profile is what attracts investors seeking yield. But it also shapes the risk profile in important ways.

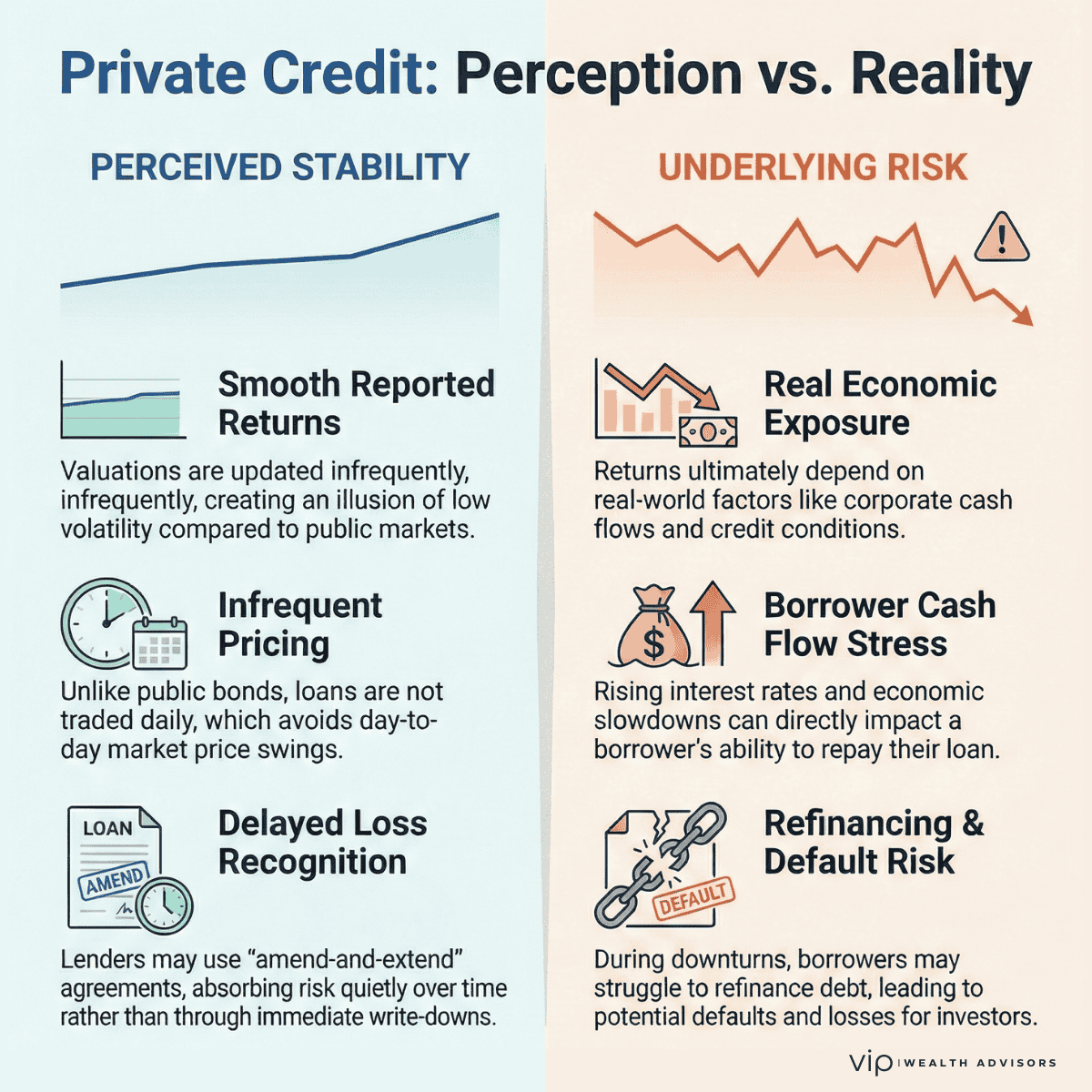

Understanding Risk: Why Private Credit Looks Safer Than It Is

One of the most common misconceptions about private credit is that it is inherently safer than other credit investments.

Private credit often looks stable because:

- Loans are not traded daily

- Valuations are updated infrequently

- Losses are recognized slowly

This creates smoother reported returns, but it does not eliminate economic risk.

Private credit borrowers are still exposed to:

- Economic slowdowns

- Rising financing costs

- Refinancing risk

- Operational challenges

Private credit diversifies pricing frequency, not underlying economic exposure.

Correlation to Stocks and Bonds

Historically, private credit has shown low reported correlation to public equities and traditional bonds. This makes it appear attractive as a portfolio diversifier.

However, the reported correlation understates the true economic linkage.

Private credit performance ultimately depends on corporate cash flows, leverage, and credit conditions. During prolonged market stress or recessions, correlations to equities and high-yield credit tend to rise, often with a lag.

This delayed response can be helpful for portfolio stability, but it should not be mistaken for insulation from downturns.

Liquidity: The Trade-Off Investors Must Accept

Private credit is illiquid by design.

Most funds require capital to be locked up for several years, with limited or no early-exit options. Distributions depend on loan repayments, refinancings, or fund wind-downs, not investor demand.

Illiquidity is not inherently bad. It is the source of the return premium. But it becomes dangerous when investors:

- Overallocate

- Ignore upcoming cash needs

- Treat private credit as a bond substitute

Liquidity risk is one of the most important planning considerations.

Tax Implications of Private Credit

Private credit is often tax-inefficient for high-income investors if not planned properly.

Most income is taxed as ordinary income, not qualified dividends or long-term capital gains. In addition:

- Investors may owe taxes on accrued or PIK interest before receiving cash

- Income may be sourced across multiple states

- Certain strategies may generate UBTI when held in retirement accounts

After-tax returns can differ dramatically from headline yields. Account placement and tax planning matter.

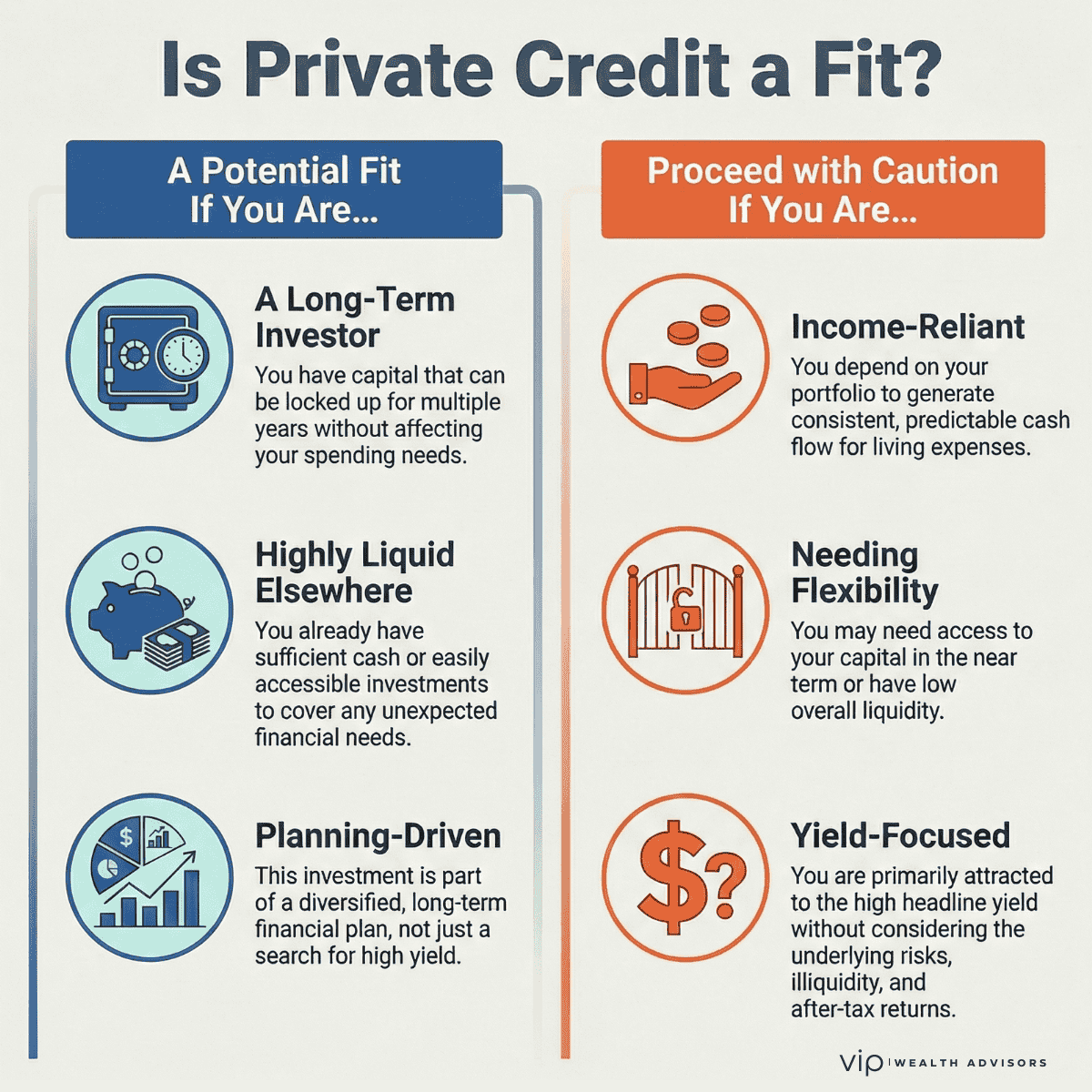

Who Should Consider Investing in Private Credit?

Private credit may be appropriate for investors who:

- Have long-term capital that they do not need for near-term spending

- Already have sufficient liquidity elsewhere

- Understand and accept illiquidity

- Are comfortable with complexity and manager risk

- Are investing as part of a diversified, planning-driven portfolio

Who Should Be Cautious or Avoid It?

Private credit is often a poor fit for investors who:

- Rely on portfolio income for living expenses

- Need flexibility or near-term access to capital

- Are highly concentrated in private investments

- Focus primarily on headline yield rather than after-tax outcomes

How Private Credit Fits Into a Wealth Plan

Private credit should not be viewed in isolation.

The right allocation depends on:

- Cash-flow needs

- Tax profile

- Time horizon

- Risk tolerance

- Total exposure to private assets

For the right investor, private credit can complement traditional fixed income and equities. For the wrong investor, it can quietly introduce fragility.

The Real Question Isn’t Yield. It’s Fit.

Private credit is neither a guaranteed income solution nor a ticking time bomb. It is a complex, illiquid asset class that rewards patient, well-planned capital and punishes mismatched expectations.

The most important question is not whether private credit is attractive in today’s market. It is whether it fits your life, goals, and financial structure.

Frequently Asked Questions About Private Credit

What is private credit?

Private credit investing involves providing loans to companies through private funds rather than public bond markets, with returns driven primarily by interest income.

Is private credit safe?

Private credit is not risk-free. It carries credit, illiquidity, and valuation opacity risks and should not be treated as a bond replacement.

How does private credit compare to bonds?

Private credit offers higher income potential but less liquidity, less transparency, and greater reliance on manager skill than traditional bonds.

Does private credit perform well in rising interest rates?

Floating-rate loans can increase income, but higher rates also raise borrower stress and default risk.

What are the main risks of private credit?

Key risks include borrower default, refinancing risk, illiquidity, delayed loss recognition, and unfavorable tax treatment.

Is private credit good for retirees?

Private credit may be inappropriate for retirees who rely on portfolio liquidity or consistent cash flow.

How much of a portfolio should be allocated to private credit?

Allocation depends on liquidity needs, risk tolerance, and total private exposure. It should be sized conservatively within a broader plan.

Is private credit tax-efficient?

Generally no. Most income is taxed as ordinary income, making tax planning and account placement critical.

Should private credit be held in retirement accounts?

Some strategies may generate UBTI, making careful review essential before holding private credit in tax-advantaged accounts.

Not Sure Where Private Credit Fits for You?

Private credit can be powerful in the right context and problematic in the wrong one. The decision should be driven by liquidity needs, taxes, and total portfolio structure, not marketing yield.