The IRS distinguishes between repairs and capital improvements based on whether an expense simply maintains a property or materially improves it, which determines whether the cost is immediately deductible or depreciated over time.

Key Takeaways

- Repairs maintain a property and are generally deductible in the year they occur.

- Capital improvements increase value, extend useful life, or adapt the property and must be depreciated.

- The IRS applies the "BAR Test" - Betterment, Adaptation, or Restoration - to determine classification.

- Understanding the unit-of-property concept is essential when evaluating repairs vs improvements.

- Safe harbor provisions may allow investors to deduct certain improvements immediately.

- Proper classification affects cash flow, depreciation deductions, and eventual capital gains taxes.

Owning rental real estate offers a wide range of tax advantages. From depreciation deductions to deductible operating expenses, the tax code can significantly improve the economics of owning investment property.

But an important, and most frequently misunderstood, concept in real estate taxation is the distinction between repairs and capital improvements.

It’s easy to assume that any money spent fixing or upgrading a property can be deducted immediately. In reality, the IRS draws a clear line between expenses that maintain a property and those that improve or enhance it.

Getting this classification wrong can lead to:

- Missed tax deductions

- Incorrect tax filings

- Increased audit risk

- Overpaying taxes unnecessarily

Understanding how the IRS treats repairs versus capital improvements is essential for managing the tax efficiency of a rental property portfolio.

This article explains how the rules work, how to apply them in real-world scenarios, and how thoughtful planning can help real estate investors optimize their tax outcomes.

The Fundamental Difference Between Repairs and Capital Improvements

The IRS separates rental property expenses into two broad categories:

- Repairs (currently deductible)

- Capital improvements (depreciated over time)

The difference comes down to what the expense actually does for the property.

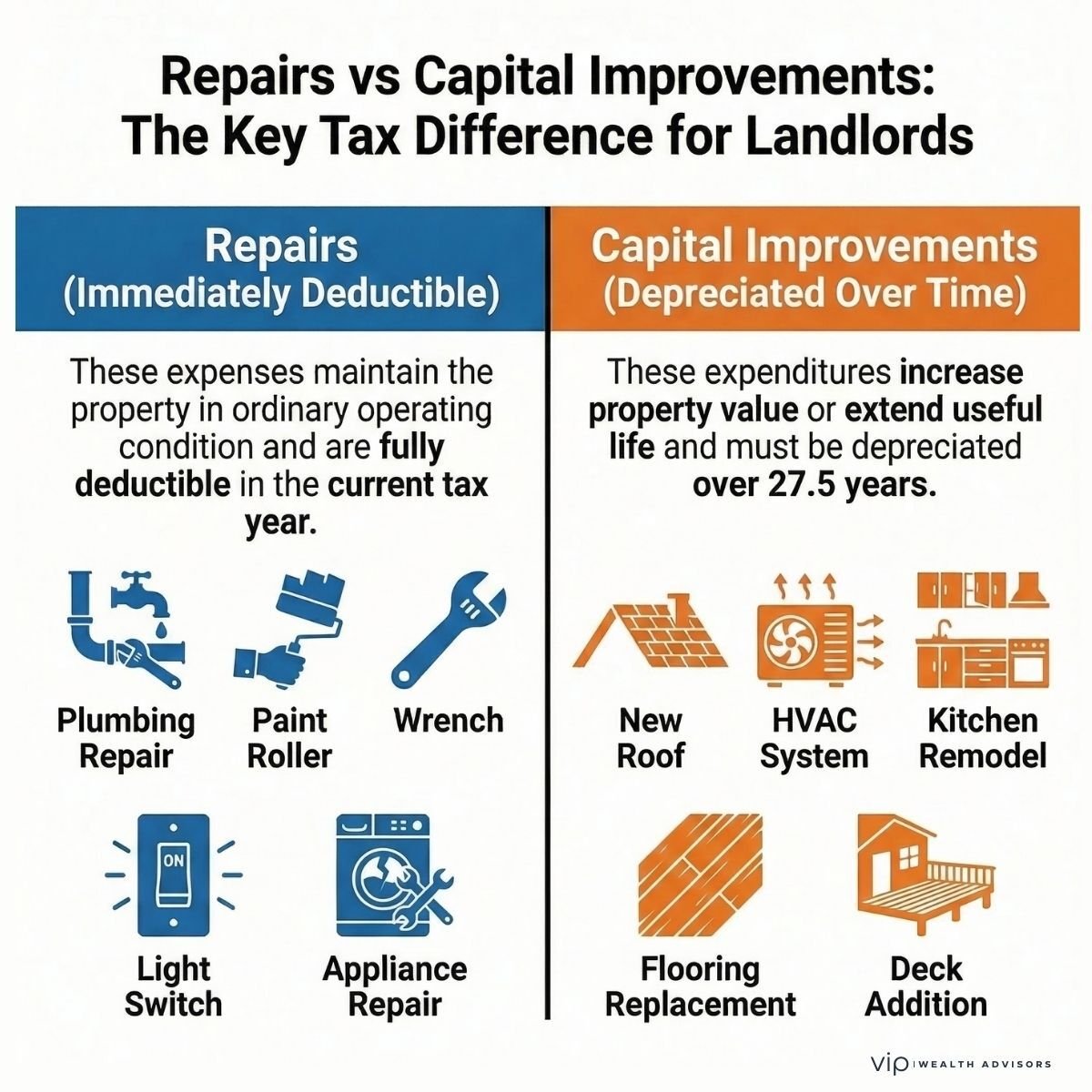

Repairs

Repairs are expenses that maintain the property in ordinary operating condition.

These expenditures fix problems or restore something to working order, but they do not materially add value, extend the property's useful life, or adapt the property to a new use.

Because repairs simply maintain the property, they are typically fully deductible in the year they occur.

These deductions are reported on Schedule E for rental property owners.

Common examples of repairs include:

- Fixing a leaking pipe

- Repairing a broken window

- Patching a small roof leak

- Replacing a light switch

- Repairing damaged drywall

- Painting between tenants

- Fixing an appliance

In short, repairs keep the property running but do not fundamentally improve it.

Capital Improvements

Capital improvements are expenses that improve, restore, or adapt a property.

Rather than maintaining the property, these expenditures increase the asset's value or extend its useful life.

Because these improvements provide long-term benefits, the IRS requires them to be capitalized and depreciated over time.

For residential rental property, improvements are generally depreciated over 27.5 years.

Examples of capital improvements include:

- Installing a new roof

- Replacing an HVAC system

- Remodeling a kitchen or bathroom

- Adding a deck or patio

- Installing new flooring throughout the property

- Replacing all plumbing lines

- Upgrading electrical systems

These expenditures create long-term improvements to the property, which is why they must be spread out over time through depreciation.

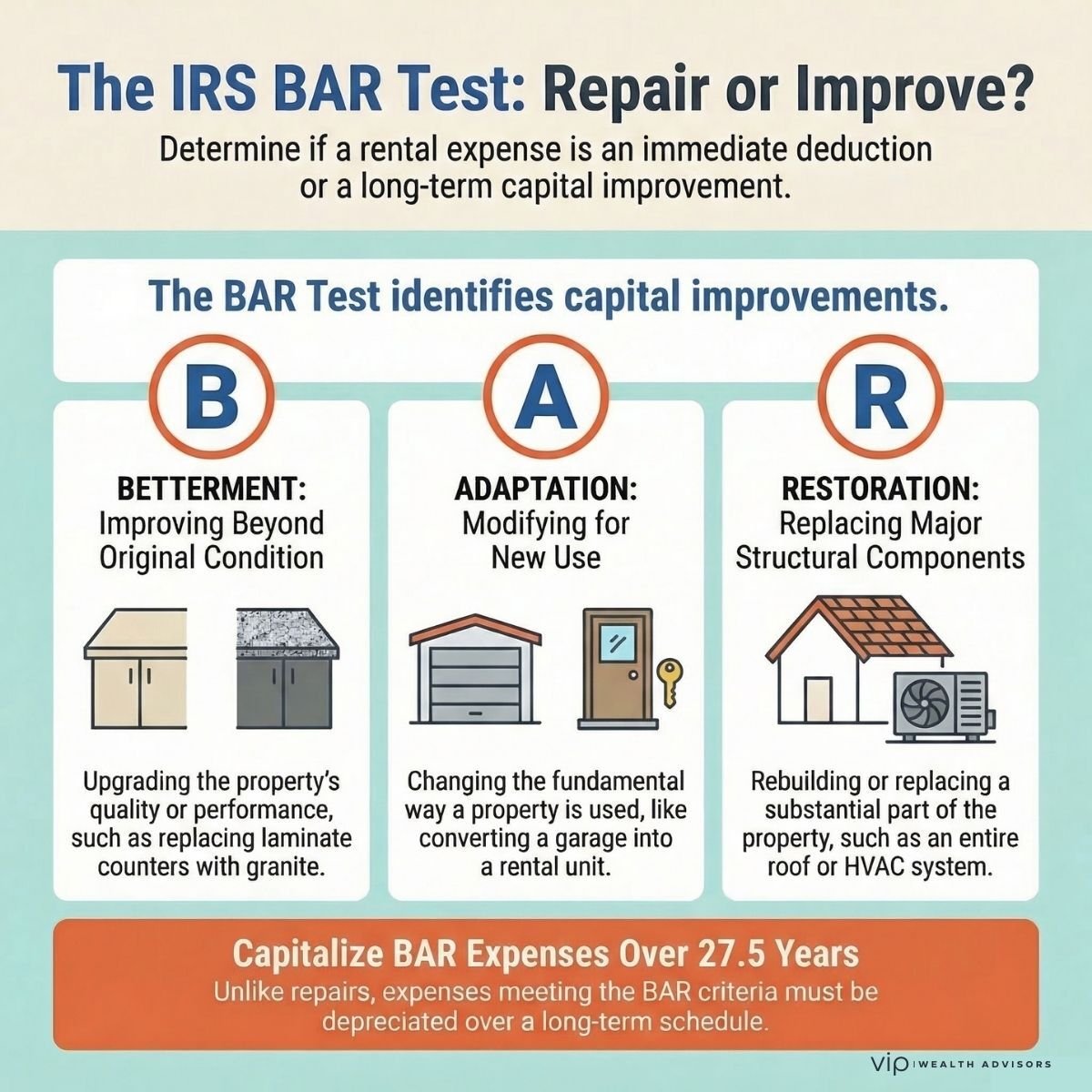

The IRS "BAR" Test: Betterment, Adaptation, or Restoration

The IRS provides guidance through what tax professionals often call the "BAR Test."

This framework helps determine whether an expense qualifies as an improvement that must be capitalized.

An expenditure is considered an improvement if it results in:

- Betterment

- Adaptation

- Restoration

Betterment

A betterment occurs when an expense improves the property beyond its original condition.

Examples include:

- Upgrading laminate countertops to granite

- Installing energy-efficient windows

- Replacing standard flooring with hardwood

- Upgrading outdated appliances

These improvements enhance the property's value or performance beyond its prior state.

Adaptation

Adaptation occurs when a property is modified for a new or different use.

Examples include:

- Converting a garage into a rental unit

- Turning a basement into an apartment

- Converting residential space into office space

These changes fundamentally alter how the property is used and, therefore, must be capitalized.

Restoration

A restoration occurs when an expense replaces a major component or substantial structural part of the property.

Examples include:

- Replacing an entire roof

- Replacing a full HVAC system

- Repiping the entire home

- Replacing major structural components

Because these expenditures effectively rebuild a significant part of the property, they are considered capital improvements.

Real-World Examples of Repairs vs Improvements

| Scenario | Repair | Capital Improvement |

|---|---|---|

| Roof | Fixing a leak or replacing a few shingles | Replacing the entire roof |

| HVAC | Replacing a motor or capacitor | Replacing the entire HVAC system |

| Flooring | Replacing several boards | Replacing flooring throughout the home |

| Plumbing | Fixing a leaking pipe | Repiping the entire home |

| Appliances | Fixing a dishwasher | Replacing all appliances during renovation |

Context always matters. The same expense may be classified differently depending on the scope of the work.

Understanding the "Unit of Property" Concept

One of the most misunderstood aspects of these rules is the concept of the unit of property (UOP).

When evaluating whether something is a repair or an improvement, the IRS does not always consider the entire building. Instead, the IRS evaluates major building systems individually.

For residential rental real estate, the unit of property includes:

- The building structure

- Roof system

- HVAC system

- Plumbing system

- Electrical system

- Fire protection system

- Structural components

This distinction matters.

For example:

Fixing one furnace component may be considered a repair.

But replacing the entire HVAC system is typically a capital improvement.

Understanding the unit-of-property concept helps investors properly classify expenses and avoid costly tax mistakes.

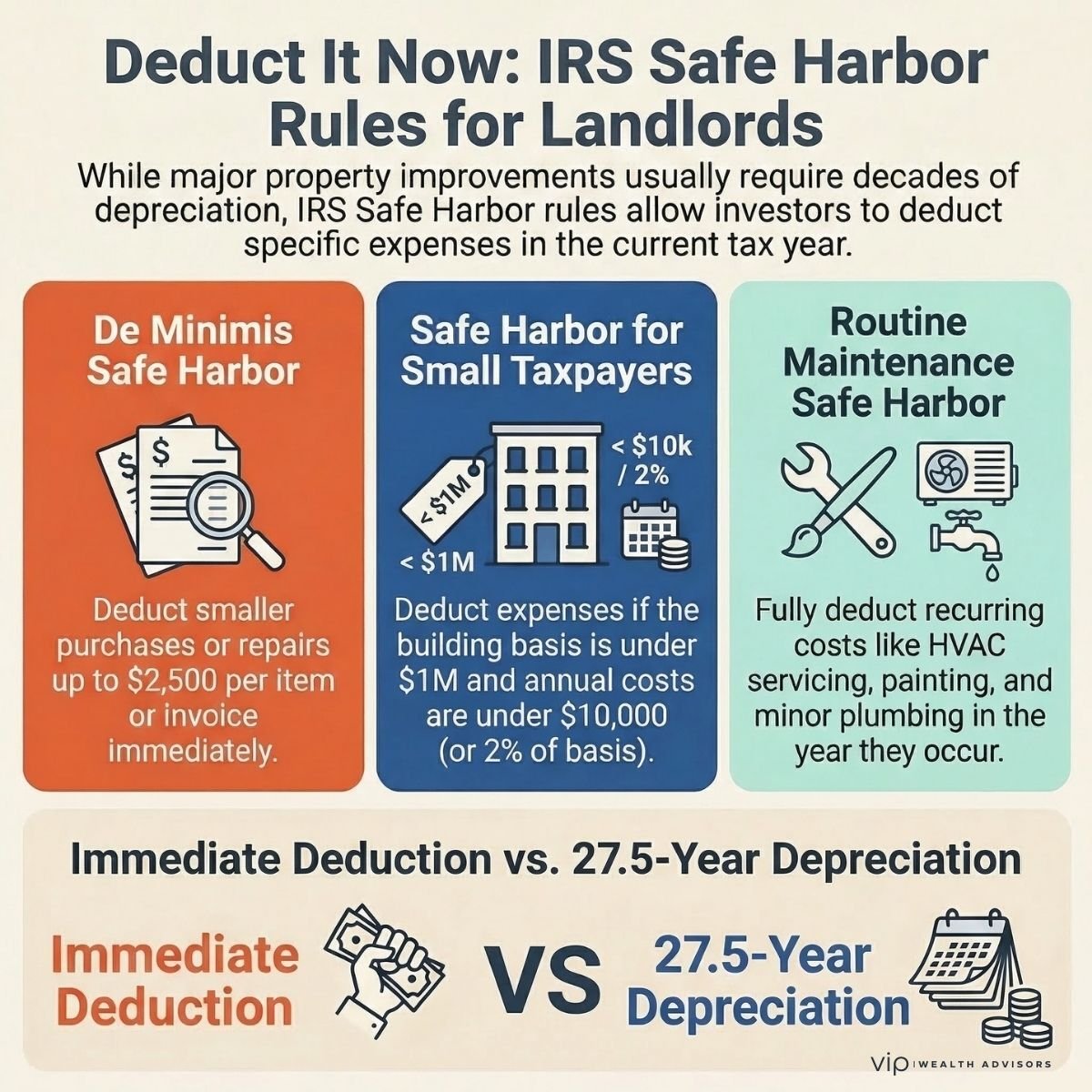

Safe Harbor Rules That Can Help Investors Deduct More

The IRS provides several safe harbor provisions that allow certain expenses to be deducted immediately rather than capitalized.

These rules can significantly benefit real estate investors.

De Minimis Safe Harbor

This rule allows taxpayers to deduct smaller purchases immediately.

For most taxpayers, the threshold is:

$2,500 per invoice or per item

Example:

Replacing a refrigerator for $1,800.

Even though the refrigerator technically improves the property, it may be deducted immediately under the de minimis safe harbor rule.

Safe Harbor for Small Taxpayers

This rule applies if:

- The building’s unadjusted basis is $1 million or less

- Annual repairs, maintenance, and improvements are $10,000 or less, or 2% of the building’s basis

If these conditions are met, many expenditures can be deducted rather than capitalized.

Routine Maintenance Safe Harbor

Certain expenses expected to recur over the life of the property may be deducted as routine maintenance.

Examples include:

- HVAC servicing

- Repainting

- Minor plumbing repairs

- Regular maintenance work

These safe harbor provisions provide flexibility and can reduce the need to capitalize smaller expenditures.

The Tax Impact of Capital Improvements

When an expense is classified as a capital improvement, it becomes part of the property’s tax basis.

The cost must then be depreciated over time.

For residential rental properties, the standard depreciation schedule is:

27.5 years

For example:

If a landlord installs a new roof costing $27,500, the annual depreciation deduction would be approximately:

$1,000 per year

While this spreads the deduction over time, the improvement also increases the property’s tax basis, which may reduce taxable gains when the property is eventually sold.

Cost Segregation: Accelerating Depreciation

Sophisticated real estate investors sometimes accelerate depreciation through a strategy known as cost segregation.

A cost segregation study identifies components of a property that qualify for shorter depreciation periods.

Examples include:

- Appliances

- Carpeting

- Cabinets

- Lighting systems

- Certain electrical components

These components may qualify for depreciation periods of:

- 5 years

- 7 years

- 15 years

Some may also qualify for bonus depreciation, allowing investors to accelerate deductions.

Cost segregation can significantly increase near-term tax deductions for investors who perform major improvements or acquire new properties.

Common Mistakes Rental Property Owners Make

Even experienced real estate investors frequently misclassify expenses.

Some of the most common mistakes include:

Deducting Major Improvements as Repairs

For example, deducting the cost of a new roof as a repair.

This is a clear capital improvement and must be depreciated.

Capitalizing Legitimate Repairs

Some investors mistakenly capitalize routine repairs, which means they lose immediate deductions.

Ignoring Safe Harbor Elections

Many investors fail to use IRS safe-harbor provisions that allow immediate deductions.

Poor Documentation

Lack of detailed invoices, contractor descriptions, or records can make it difficult to justify classifications during an audit.

Proper documentation is critical.

Lack of detailed invoices, contractor descriptions, or records can make it difficult to justify classifications during an audit.

Why This Distinction Matters for Long-Term Wealth

The repair-versus-improvement distinction affects far more than just annual taxes.

It influences:

- Cash flow

- Tax timing

- Property basis

- Depreciation deductions

- Capital gains upon sale

Investors who understand these rules can make more strategic decisions about when to perform renovations, how to structure improvements, and how to optimize tax outcomes.

When integrated with broader financial planning, these decisions can significantly improve the long-term economics of real estate investing.

Tax Clarity Leads to Better Real Estate Investment Decisions

Understanding the difference between repairs and capital improvements is more than a technical tax rule. It is a key component of managing rental property efficiently and maximizing after-tax returns.

Investors who approach these decisions thoughtfully and with proper documentation can avoid costly mistakes while making the most of the tax advantages real estate offers.

Frequently Asked Questions

What is the difference between a repair and a capital improvement for rental property?

A repair maintains a property in ordinary operating condition and is typically deductible in the year it occurs. A capital improvement enhances the property, restores major components, or adapts it to a new use and must be capitalized and depreciated over time.

Are rental property repairs tax-deductible?

Yes. Repairs that maintain the property without materially improving it are generally fully deductible in the year they occur.

Is replacing a roof a repair or a capital improvement?

Replacing an entire roof is typically considered a capital improvement and must be depreciated over the applicable recovery period.

Can painting a rental property be deducted immediately?

Yes. Painting is generally considered a repair or routine maintenance expense and is typically deductible in the year incurred.

Are appliance repairs or improvements for rental property?

Replacing an appliance may be considered an improvement. However, if the cost is below the $2,500 de minimis safe harbor threshold, it may be deducted immediately.

How long are rental property improvements depreciated?

Most residential rental property improvements are depreciated over 27.5 years, although certain components may qualify for shorter depreciation periods through cost segregation.

What happens if you incorrectly classify an improvement as a repair?

If the IRS determines an improvement was improperly deducted as a repair, the expense may need to be capitalized and depreciated, potentially resulting in additional taxes, penalties, or interest.

Do capital improvements reduce taxes when selling a rental property?

Yes. Capital improvements increase the property's tax basis, potentially reducing taxable capital gains when the property is sold.

Planning Rental Property Taxes Strategically

The line between a repair and a capital improvement can dramatically change the tax outcome of a real estate investment.

Strategic tax planning can help investors accelerate deductions, reduce audit risk, and maximize after-tax returns from rental property.