Most non-spousal beneficiaries must empty inherited IRAs within 10 years, but whether annual RMDs are required depends on the owner's RBD and the beneficiary's classification.

Key Takeaways

- The 10-year rule applies to most non-spousal beneficiaries.

- Annual RMDs are required only if the owner died on or after their RBD.

- Eligible Designated Beneficiaries may use life expectancy payouts, sometimes temporarily.

- Roth IRAs follow the 10-year rule but generally avoid annual RMDs.

- Missteps can trigger penalties, higher taxes, and lost planning flexibility.

Inherited IRAs are no longer open-ended assets for non-spousal beneficiaries. From the moment an IRA owner dies, federal law imposes a defined distribution timeline that governs how long the account may remain open and how withdrawals must be made. That timeline was rewritten by the SECURE Act, refined by SECURE 2.0, and finalized by the IRS's July 2024 regulations.

For beneficiaries, these changes determine whether annual required minimum distributions apply, whether withdrawals can be delayed, and when the account must be fully drained. Missing the distinction can carry real tax consequences.

This article lays out the current rules in plain terms. It explains when RMDs are required, when they are not, and how the outcome changes based on the owner's date of death, the beneficiary's classification, and the type of IRA inherited. The goal is precision, compliance, and tax-aware decision-making, not guesswork.

Why Inherited IRA Rules Changed So Dramatically

Before 2019, non-spousal beneficiaries could stretch distributions from an inherited IRA over their own life expectancy. A 40-year-old child inheriting an IRA from a parent could spread taxable income over four decades. Congress decided that the level of deferral was too generous.

The SECURE Act of 2019 eliminated the stretch IRA for most non-spousal beneficiaries and replaced it with the 10-year rule. Unfortunately, the statute left open a critical question that confused taxpayers and advisors alike: Does the 10-year rule require annual RMDs, or does it simply require the account to be emptied by the end of year 10?

That ambiguity triggered years of conflicting interpretations until the IRS issued final regulations in July 2024. As of 2025, the rules are settled, but only if you know exactly which category you fall into.

Key Terms You Must Understand

The IRS uses exact definitions. One misclassification can change the entire distribution outcome.

Non-Spousal Beneficiary refers to any individual or entity that inherits an IRA but is not the decedent's spouse. This includes adult children, minor children, siblings, friends, trusts, estates, and charities.

Designated Beneficiary means an individual human being named on the beneficiary form. Estates, charities, and certain trusts do not qualify.

Eligible Designated Beneficiary (EDB) is a special subset of designated beneficiaries that Congress carved out for favorable treatment. EDBs include the surviving spouse, the decedent's minor child, disabled individuals, chronically ill individuals, and anyone not more than 10 years younger than the decedent.

Required Beginning Date (RBD) is the date by which an IRA owner must begin taking RMDs during life. Under current law, the RBD is April 1 of the year following the year the owner reaches age 73 if born between 1951 and 1958, or age 75 if born in 1959 or later.

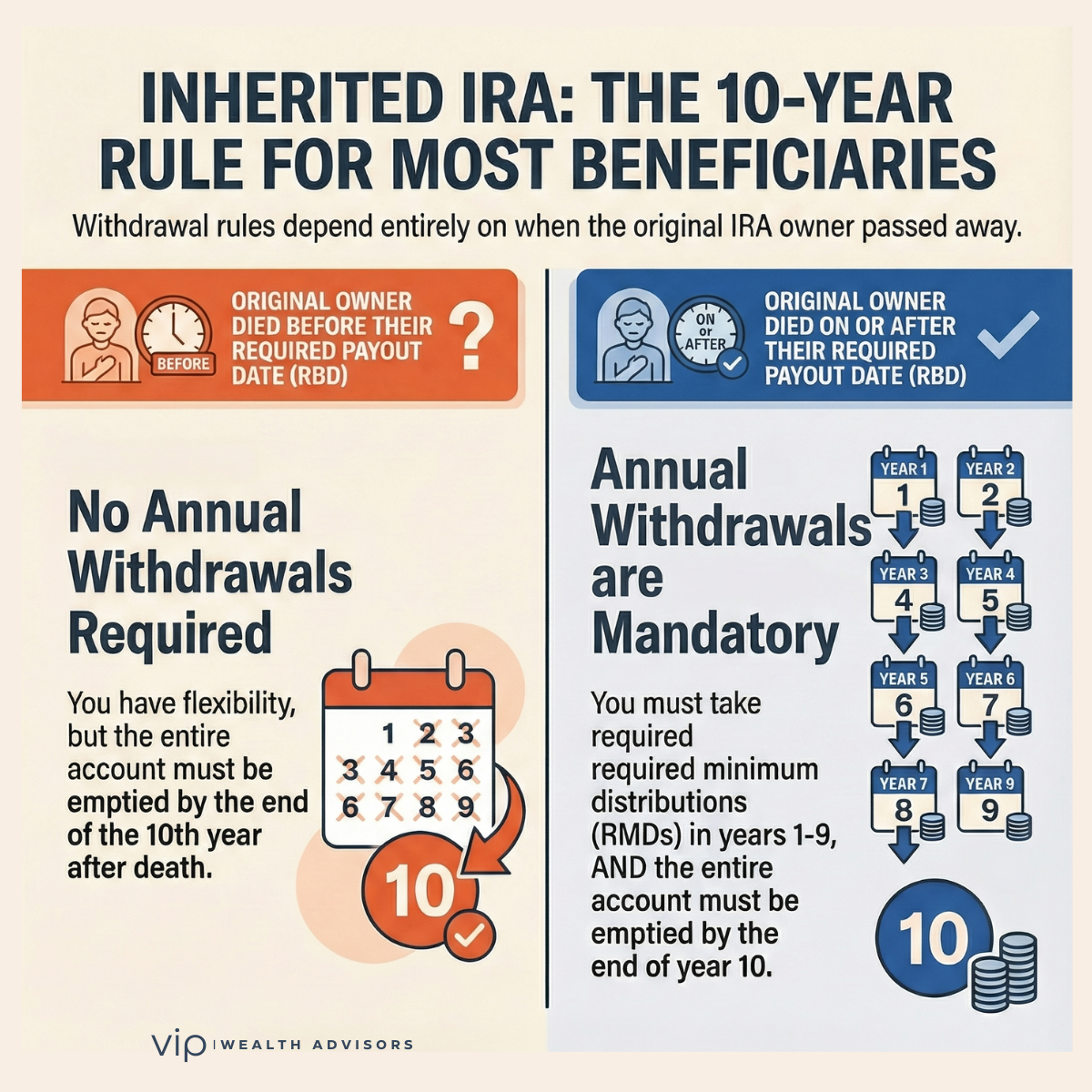

The Single Most Important Question: Did the Owner Die Before or After Their RBD?

For non-spousal beneficiaries, everything hinges on one fact: whether the original IRA owner died before or after their required beginning date.

This single detail determines whether annual Required Minimum Distributions are required during the 10-year window, or whether distributions can be delayed entirely until the final year.

Non-Spouse Beneficiaries Who Are Not Eligible Designated Beneficiaries

Most inherited IRAs today fall into this category. Adult children, grandchildren, and other beneficiaries who do not qualify as EDBs are subject to the SECURE Act's 10-year rule.

Owner Died Before Their RBD

If the IRA owner died before their required beginning date, the beneficiary is not required to take annual RMDs during years one through nine. However, the account must be fully distributed by December 31 of the tenth year following the year of death.

This allows for tax planning flexibility. Beneficiaries may spread withdrawals unevenly or wait until later years, but failure to empty the account by the end of year ten results in penalties.

Owner Died On or After Their RBD

If the owner died on or after their required beginning date, the rules are far less forgiving. The beneficiary must take annual RMDs in years one through nine using the Single Life Table. In addition, the entire account must still be emptied by the end of year ten.

The IRS confirmed in the July 2024 final regulations that these annual RMDs are mandatory, not optional. This clarification resolved years of confusion but caught many beneficiaries off guard.

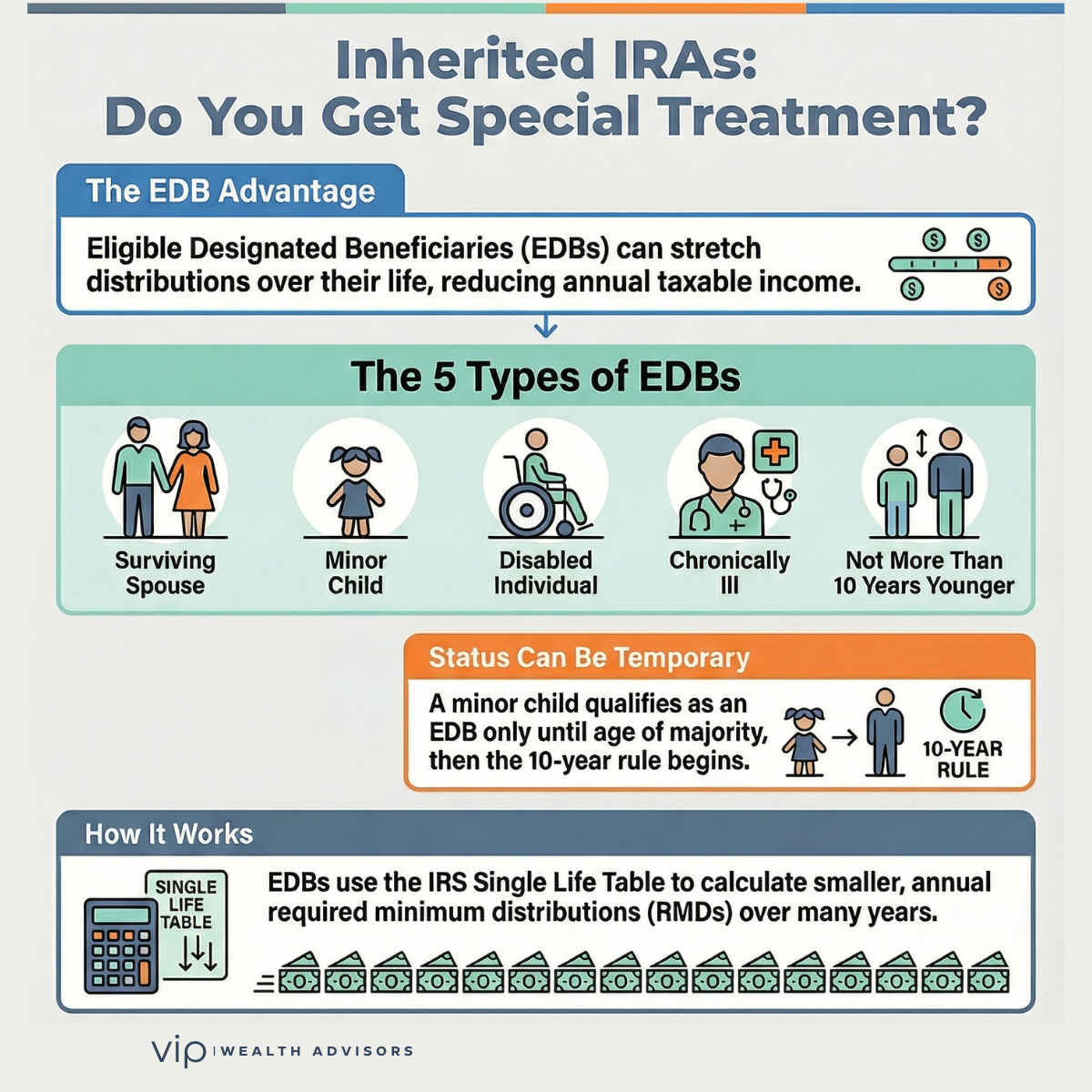

Who Gets Special Treatment: Eligible Designated Beneficiaries (EDBs)

While the SECURE Act eliminated lifetime stretch payouts for most non-spousal beneficiaries, it preserved them for a narrow but essential group: Eligible Designated Beneficiaries.

An Eligible Designated Beneficiary includes:

- The decedent's surviving spouse

- The decedent's minor child (until reaching the age of majority)

- A disabled individual as defined under IRC §72(m)(7)

- A chronically ill individual

- Any individual not more than 10 years younger than the decedent

EDBs may take distributions over their own life expectancy using the IRS Single Life Table. This can dramatically reduce annual taxable income compared to the 10-year rule. However, this favorable treatment is not permanent in all cases.

Example: Disabled Child as an Eligible Designated Beneficiary

Consider the following scenario.

An IRA owner dies in 2025 at age 68, before reaching their required beginning date. The sole beneficiary is the owner's 30-year-old child, who qualifies as disabled under section 72(m)(7). Proper medical documentation must be provided to the plan administrator by October 31 of the year following the death.

Because the beneficiary meets the IRS definition of a disabled individual, they qualify as an Eligible Designated Beneficiary. As a result, the child may take annual RMDs over their own life expectancy rather than being forced into the 10-year rule.

If the child is age 31 in the year following the owner's death, the applicable life expectancy factor from the Single Life Table is 54.4. If the inherited IRA balance is $100,000, the first required minimum distribution is approximately $1,838.

Each subsequent year, the life expectancy factor is reduced by one. This method allows the bulk of the IRA to remain tax-deferred for decades.

If the disabled child dies before the account is fully distributed, the remaining balance must be withdrawn by the successor beneficiary within ten years of the child's death.

Example: Beneficiary Not More Than Ten Years Younger Than the Decedent

Now consider a different scenario.

An IRA owner dies in 2025 at age 75. The sole beneficiary is the owner's sibling, age 70. Because the sibling is not more than ten years younger than the decedent, they qualify as an Eligible Designated Beneficiary.

The sibling may take RMDs over their own life expectancy using the Single Life Table. If the sibling is age 71 in the year following the owner's death, the applicable life expectancy factor is 18.0. On an inherited IRA valued at $180,000, the first RMD would be $10,000.

As with other EDBs, if the sibling dies before the account is fully distributed, the successor beneficiary must drain the account within ten years.

What Happens When an EDB Loses Their Status

Some EDB categories are temporary. Minor children are the most common example. A minor child of the decedent may use the life expectancy method until reaching the age of majority. At that point, the 10-year rule begins, and the account must be fully distributed within ten years after adulthood.

This transition often catches families by surprise and requires proactive planning.

Non-Designated Beneficiaries: Estates, Charities, and Certain Trusts

If the beneficiary is not an individual, different rules apply. If the owner died before their required beginning date, the account must be fully distributed by the end of the fifth year following death.

If the owner died on or after their required beginning date, distributions are taken over the decedent's remaining life expectancy, reduced by one each year.

Trusts require special attention. Only trusts that qualify as see-through trusts can access designated beneficiary treatment.

Roth IRAs Inherited by Non-Spousal Beneficiaries

Roth IRAs follow a simpler framework. Roth IRA owners are treated as having died before their RBD. As a result, most non-spousal beneficiaries are subject to the 10-year rule, but no annual RMDs are required in years one through nine.

The account must still be fully distributed by the end of year ten.

IRS Transition Relief for Missed RMDs

Due to widespread confusion, the IRS waived excise taxes for missed RMDs for beneficiaries subject to the 10-year rule for calendar years 2021 through 2024. This relief does not extend the 10-year distribution deadline.

Beginning in 2025, enforcement is expected to resume in full.

Why Inherited IRA Planning Still Matters

Inherited IRAs are no longer passive assets. The distribution schedule affects tax brackets, Medicare premiums, Net Investment Income Tax exposure, and long-term wealth preservation.

For high-income families, a poorly managed inherited IRA can trigger unnecessary taxes year after year. A properly structured plan can turn a compliance headache into a controlled, intentional tax strategy.

At VIP Wealth Advisors, inherited IRA planning is integrated with tax planning, investment strategy, and estate planning, so beneficiaries are not making decisions in isolation.

Putting the Inherited IRA Rules Into Practice

The rules for non-spousal beneficiaries of inherited IRAs are now settled, but they are anything but simple. The correct answer depends on the date of death, the beneficiary's classification, the type of IRA, and whether the owner had reached their required beginning date.

For most beneficiaries, the 10-year rule applies. For Eligible Designated Beneficiaries, life expectancy payouts remain available, at least temporarily. Missing even one detail can lead to penalties or lost planning opportunities.

This is an area where professional guidance is not a luxury. It is a necessity

Q&A: Inherited IRA RMD Rules

Do non-spousal beneficiaries have to take required minimum distributions from an inherited IRA?

It depends on when the original IRA owner died and the beneficiary's classification under IRS rules. Most non-spousal beneficiaries are subject to the 10-year rule. If the owner died before their required beginning date, no annual RMDs are required, but the account must be fully distributed by the end of the tenth year. If the owner died on or after their required beginning date, annual RMDs are required in years one through nine, and the account must still be emptied by the end of year ten.

What is the 10-year rule for inherited IRAs?

The 10-year rule requires most non-spousal beneficiaries to fully distribute an inherited IRA by December 31 of the tenth year following the year of the original owner's death. In some cases, annual RMDs are required during the 10-year period. In other cases, distributions can be delayed until later years. The determining factor is whether the owner died before or after their required beginning date.

Are annual RMDs required during the 10-year rule?

Annual RMDs are required during the 10-year period only if the IRA owner died on or after their required beginning date. If the owner died before their required beginning date, no annual RMDs are required, but the account must still be fully distributed by the end of year ten.

Who qualifies as an Eligible Designated Beneficiary (EDB)?

An Eligible Designated Beneficiary includes the decedent's surviving spouse, the decedent's minor child, a disabled individual, a chronically ill individual, or any individual who is not more than 10 years younger than the decedent. EDBs are allowed to take distributions over their own life expectancy instead of being subject to the standard 10-year rule.

Can an Eligible Designated Beneficiary still use the life expectancy method?

Yes. Eligible Designated Beneficiaries may calculate RMDs using their own life expectancy under the IRS Single Life Table. This allows distributions to be spread over many years. However, in some cases, this treatment is temporary, such as when a minor child reaches the age of majority.

What happens when an Eligible Designated Beneficiary dies?

When an Eligible Designated Beneficiary dies before the inherited IRA is fully distributed, the successor beneficiary is generally subject to the 10-year rule. The remaining account balance must be fully withdrawn by December 31 of the tenth year following the EDB's death.

Are inherited Roth IRAs subject to required minimum distributions?

Inherited Roth IRAs are subject to the 10-year rule for most non-spousal beneficiaries, but annual RMDs are not required during years one through nine. The account must still be fully distributed by the end of the tenth year, regardless of the original owner's age at death.

What happens if the beneficiary is an estate, charity, or non-qualifying trust?

If the beneficiary is not an individual, the account is treated as having a non-designated beneficiary. If the IRA owner died before their required beginning date, the account must be fully distributed by the end of the fifth year following death. If the owner died on or after their required beginning date, distributions are taken over the decedent's remaining life expectancy.

What is the required beginning date (RBD) for IRA owners?

The required beginning date is April 1 of the year following the year the IRA owner reaches the applicable age. For individuals born between 1951 and 1958, the RBD is tied to age 73. For those born in 1959 or later, the RBD is tied to age 75.

Did the IRS provide relief for missed inherited IRA RMDs?

Yes. The IRS waived excise taxes for missed RMDs for certain beneficiaries subject to the 10-year rule for calendar years 2021 through 2024 due to widespread confusion following the SECURE Act. This relief does not extend the 10-year distribution deadline. Beginning in 2025, enforcement is expected to resume under the finalized rules.

What is the penalty for missing an inherited IRA RMD?

The excise tax for failing to take a required minimum distribution is generally 25 percent of the amount not withdrawn. The penalty may be reduced to 10 percent if the error is corrected in a timely manner and properly reported, but reliance on penalty relief should not be part of a planning strategy.

Why does inherited IRA planning still matter under the 10-year rule?

Even under the 10-year rule, the timing of distributions can significantly affect tax brackets, Medicare premiums, Net Investment Income Tax exposure, and overall wealth outcomes. Strategic coordination with income, deductions, and investment planning can materially reduce lifetime taxes for beneficiaries.

Inherited an IRA and Not Sure Which Rules Apply?

Inherited IRA decisions affect taxes, Medicare premiums, and long-term wealth outcomes. A single misstep can be costly.